|

|

August 3, 2011

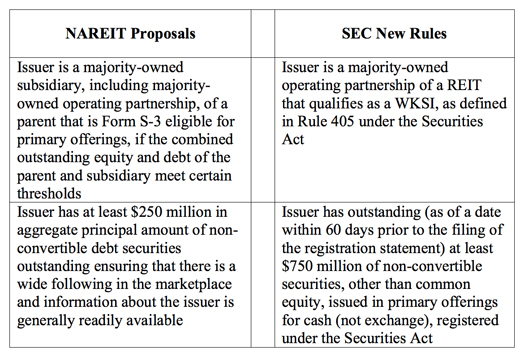

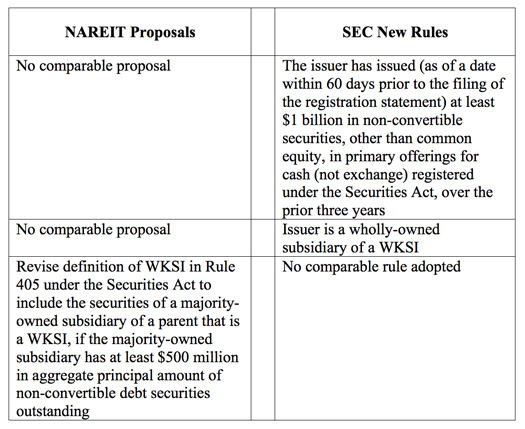

SEC Adopts New Short-Form Criteria to Replace Credit RatingsAs required by Section 939A of the Dodd-Frank Wall Street Reform and Consumer Protection Act, the Securities and Exchange Commission (SEC) voted unanimously on July 26, 2011 to adopt new rules (New Rules) to remove credit ratings as eligibility criteria for companies seeking to use “short form” registration to register the offering of securities.1 Rather than relying on certain credit ratings criteria, the New Rules now permit a majority-owned operating partnership of a real estate investment trust (REIT) that qualifies as a well-known seasoned issuer (WKSI) to use Form S-3 for offerings of non-convertible debt securities under the Securities Act of 1933 (the Securities Act), among other changes.   The REIT-specific eligibility criteria represents a significant broadening of the eligibility criteria contained in the SEC’s initial proposal, which threatened to create substantial roadblocks to continued access by REITs to the public debt capital markets. In explaining why it singled out REIT operating partnerships for Form S-3 eligibility, the SEC specifically cited the NAREIT Letter in noting that investors and other market participants that follow Umbrella Partnership Real Estate Investment Trusts (UPREITs) analyze the operations of their operating partnerships in conjunction with following the UPREITs. The New Rules will take effect 30 days after they are published, but will include a temporary grandfather provision that allows an issuer to use Form S-3 for a period of three years from the effective date of the New Rules if the issuer would have been eligible to register the securities offerings under the old criteria. However, since the final rule is favorable to UPREITs, the use of the grandfather provision will probably not be necessary. 1See SEC Release Nos. 33-9245; 34-64975 (July 27, 2011)

ContactFor further information, please contact Tony Edwards at tedwards@nareit.com. |