The commercial real estate (CRE) mortgage market has changed dramatically since the end of 2021. For many real estate investors, gone are the days of low-cost, readily available property financing. Today, borrowers face significantly higher interest rates and stricter underwriting standards. The public-private market divergence in real estate valuations has further complicated the mortgage underwriting process, as private property valuations have been slow to adjust to market realities. As a result, many private market real estate investors seeking to refinance their properties are finding themselves in a pickle. Some are facing the prospects of negative leverage; others are finding their current loans cannot be refinanced at par.

REITs Have Well-Structured Balance Sheets

While U.S. public equity REITs may not have been immune from the current mortgage market turmoil, data from the Nareit Total REIT Industry Tracker Series (T-Tracker®) for the first quarter of 2023, the latest data available, show that they have been reasonably well-insulated from it. Specifically, on average, equity REITs have maintained long-term, well-structured balance sheets with low leverage ratios, predominantly utilizing unsecured debt and fixed interest rates. Capital markets have been open for REITs and they have been successfully issuing unsecured debt and equities. REITs have also continued to deliver meaningful year-over-year funds from operations (FFO) and net operating income (NOI) gains. With their strong balance sheets and solid operational performance, equity REITs are well-prepared to navigate this period of economic and capital market uncertainty.

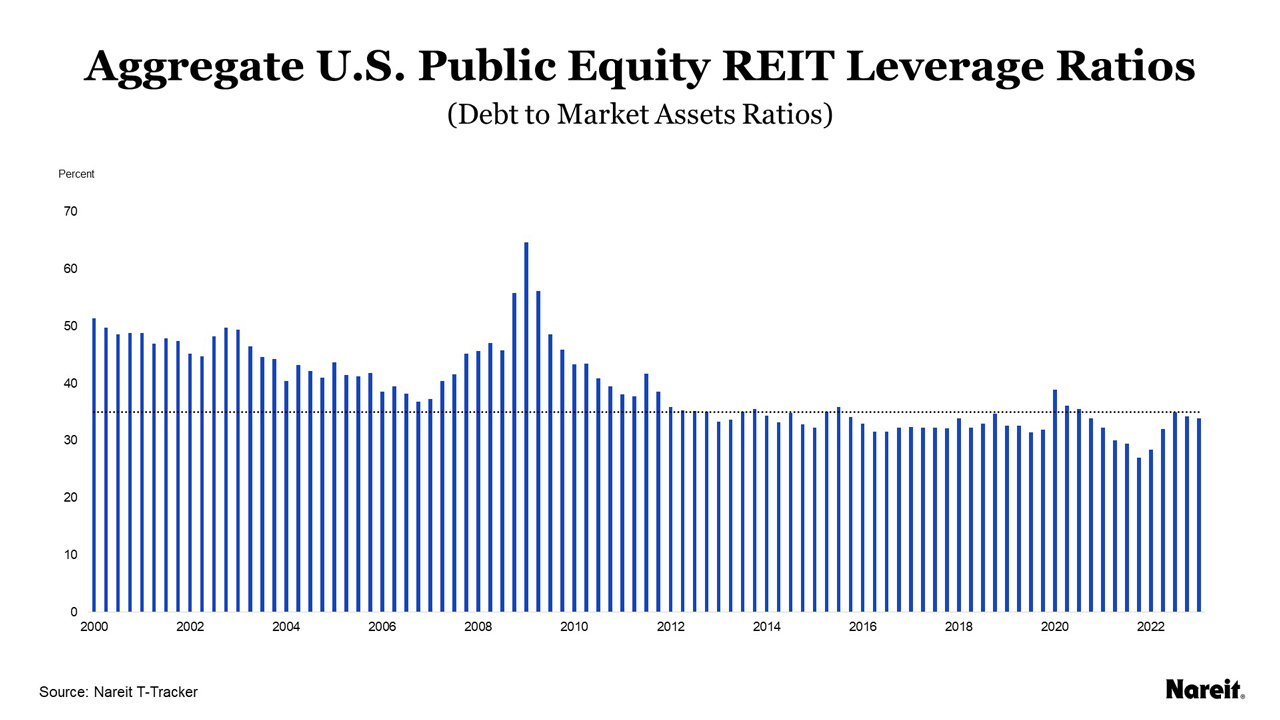

The chart above presents quarterly aggregate U.S. public equity REIT leverage (debt to market assets) ratios from the first quarter of 2000 to the first quarter of 2023. It also indicates a leverage ratio threshold of 35%. This threshold is one of the inclusion criteria for a fund to be part of the NCREIF Fund Index—Open End Diversified Core Equity; these private real estate funds follow core investment strategies. The equity REIT leverage ratio peaked during the Great Financial Crisis; it was 64.7% in the first quarter of 2009. Since 2013, the REIT debt to market assets ratio has generally remained below 35%. In the first quarter of 2023, the leverage ratio was 33.9%.

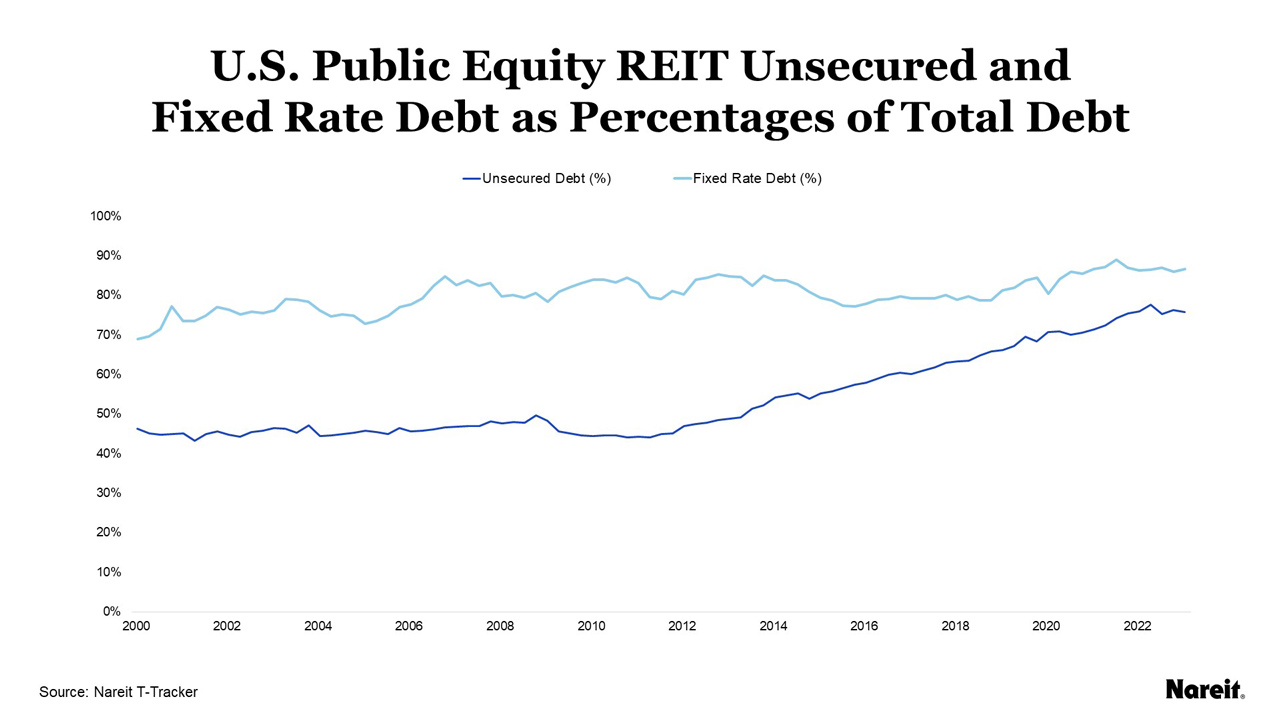

The chart above displays quarterly unsecured and fixed rate debt as percentages of total debt for U.S. public equity REITs from the first quarter of 2000 to the first quarter of 2023. Equity REIT use of unsecured debt typically ranged between 45% and 50% of total debt prior to 2013. After that time, unsecured debt utilization grew consistently, reaching 76.0% of total debt in the first quarter of 2023. REITs have also favored using fixed rate debt. At the beginning of 2000, fixed rate debt accounted for almost 70% of equity REIT total debt. By the first quarter of 2023, it comprised 87.0% of total debt; the weighted average term to maturity for all REIT debt was nearly 7 years. By focusing on unsecured, fixed rate, and longer-term debt, public equity REITs have limited their exposure to the challenges of the current mortgage market.

While U.S. public equity REITs have not been immune from rising interest rates, their debt costs only increased marginally compared to the recent surge in the 10-year Treasury yield. From the fourth quarter of 2021 to the first quarter of 2023, the U.S. 10-year Treasury yield increased by 212 basis points to 3.7%. Over the same time frame, the public equity REIT weighted average interest rate on total debt rose by 55 basis points to 3.9%. Although the average in-place REIT debt cost has steadily increased over the past year, it is now just slightly higher than the 10-year U.S. Treasury yield.

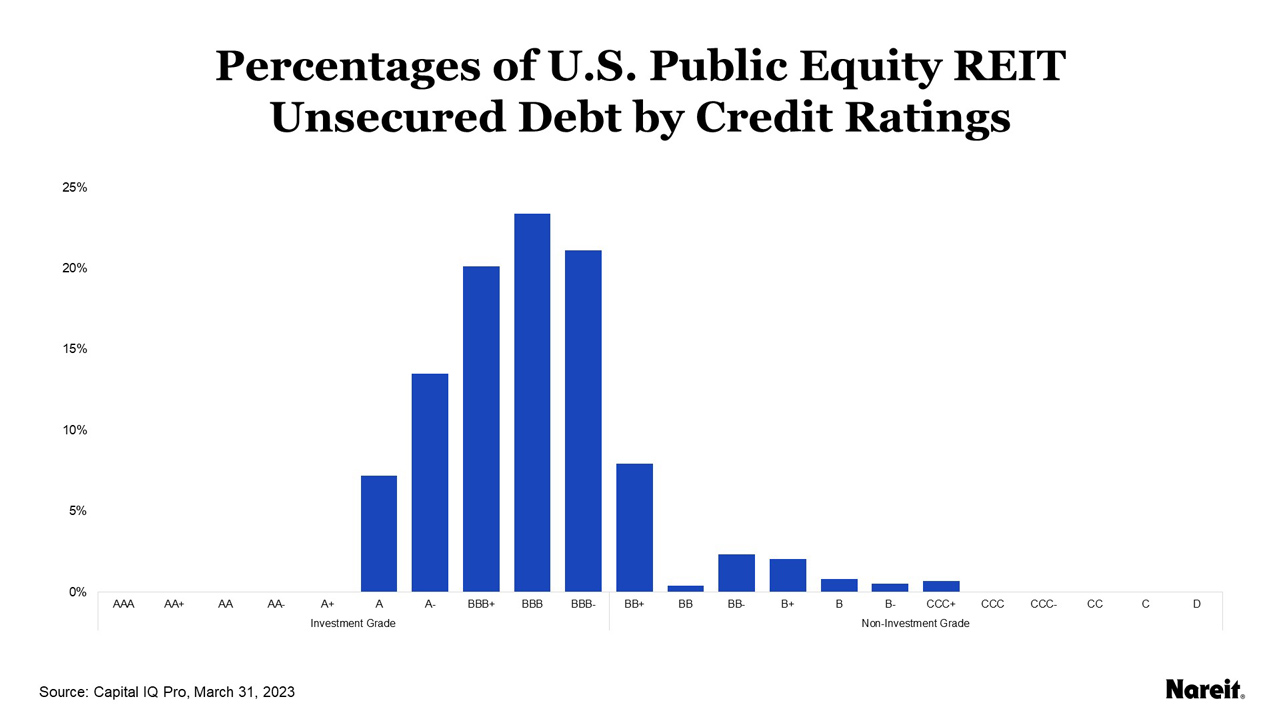

The chart above shows the percentages of U.S. public equity REIT unsecured debt by credit ratings from S&P Global Ratings. Investment-grade ratings include all those that are BBB- or better. Today, over 85% of public equity REITs have an investment-grade bond rating. These REITs accounted for $1.4 trillion in capital as of the first quarter of 2023. While the majority of that capital was sourced from common equity, nearly one-fourth of it was in unsecured debt; approximately 5% was in the form of secured debt like mortgages.

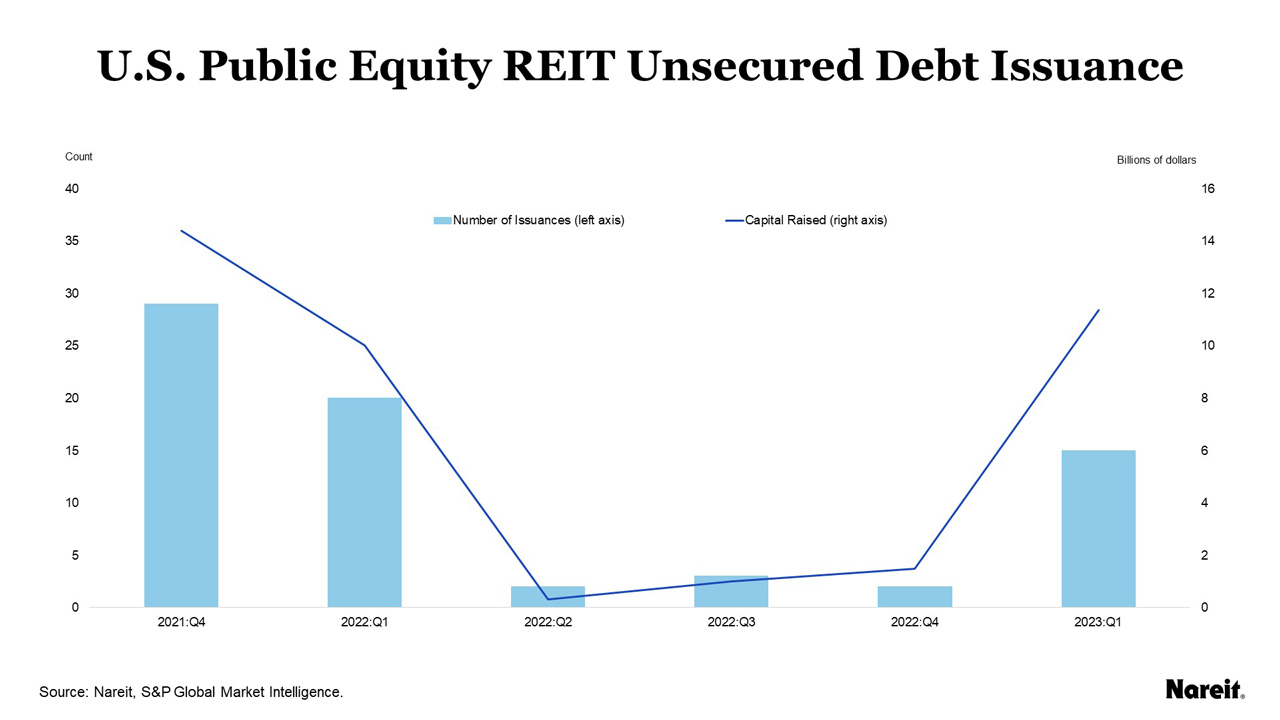

The chart above exhibits unsecured debt issuance by U.S. public equity REITs from the fourth quarter of 2021 through the first quarter of 2023, highlighting both the number of issuances and total capital raised. With the rise in interest rates and debt costs in 2022, REITs acted rationally; their unsecured debt issuance fell off precipitously. Importantly, the unsecured debt market remained open and available to REITs during that time. In the first quarter of 2023, there has been a material uptick in unsecured debt issuance. Fifteen senior debt deals with an aggregate value of $11.4 billion were closed during that time. The gross amount offered including over-allotment and yield to maturity median values for these issuances were $650 million and 5.3%, respectively. The unsecured debt market clearly provides U.S. public equity REITs access to significant capital at attractive interest rates.

REITs Well-Prepared to Navigate Economic, Capital Market Uncertainty

With higher interest rates, stricter underwriting standards, and changing property valuations, many private real estate investors are ill-equipped to face the current financing environment. This has fueled concerns about real estate debt holdings and the potential for escalating CRE defaults. It has also increased the perceived risk of the overall industry. While U.S. public equity REITs are not immune from the current mortgage market turmoil, on average, REITs have limited their exposure to these challenges by maintaining leverage ratios consistent with core investment strategies and focusing on unsecured, fixed rate, and longer-term debt. Access to the unsecured debt market provides U.S. public equity REITs with a competitive advantage over many of their private real estate market counterparts. Today, REITs continue to be well-prepared to navigate this period of economic and capital market uncertainty.