Blackstone’s recent acquisition of Apartment Income REIT Corp. (NYSE: AIRC) is being seen by many as a solid endorsement of future prospects for the multifamily sector, underscoring expectations that pressures from new supply and high interest rates will start to recede later this year and into 2025.

Blackstone is making a big bet on the multifamily sector with its $10 billion take-private of Apartment Income REIT, known as AIR Communities. The acquiring entity, Blackstone Real Estate Partners X, said that it plans to invest more than $400 million to maintain and improve the 76-property portfolio and may invest additional capital to fund further growth.

“Blackstone has a great record of acting prior to the movement in cycles. And given the amount of capital they have to deploy, I think they wanted to get in early and also take down a large portfolio, which is not that easy to assemble,” says Jeffrey Adler, vice president at Matrix Yardi Systems Inc.

The acquisition could be a sign that values have bottomed and will go up from here. The question is the speed at which that recovery moves, he says. “But they've got a little more patience and a longer-term perspective that as long as it's not going down, they want to enter the market,” he adds.

The AIR acquisition follows an announcement in January that Blackstone Real Estate Partners X and Blackstone Real Estate Income Trust Inc. (BREIT) were acquiring Tricon Residential Inc. in a deal valued at $3.5 billion. Tricon owns a single-family rental (SFR) portfolio and development platform focused on high growth U.S. markets, as well as a multifamily development platform in Canada. Under Blackstone’s ownership, the company plans to complete its $1 billion development pipeline of new SFR homes in the U.S. and $2.5 billion of new apartments in Canada.

The two acquisitions are a statement about Blackstone’s view on residential real estate in the U.S. “Their take is that the housing shortage is unlikely to get significantly better, which would give incumbent landlords pricing power over time,” says Rob Goldstein, portfolio manager, real estate securities at CenterSquare Investment Management. “I think they’re also looking at a REIT market that's a little bit dislocated from the private market, and they saw an opportunity to get into a very large, high-quality portfolio at a relatively attractive basis,” he says.

Mixed Signals

Multifamily has seen near record high levels of new construction and the Sunbelt markets are taking the brunt of that supply punch. COVID accelerated population growth and demand for housing across the Sunbelt, with asking rents that skyrocketed by as much as 30% to 40% in some cases during 2021.

Not surprisingly, rent growth coupled with low interest rates sparked a huge building boom in markets such as Austin, Atlanta, Phoenix, Nashville, and Raleigh. Those high-growth markets are now the ones struggling the most due to high levels of new supply.

“If you strip away the dozen or so cities that have a lot of supply now delivering, we actually have very good demand, very good absorption, and growing rents in the Midwest, Northeast, and some of the smaller mountain states and cities,” Adler says.

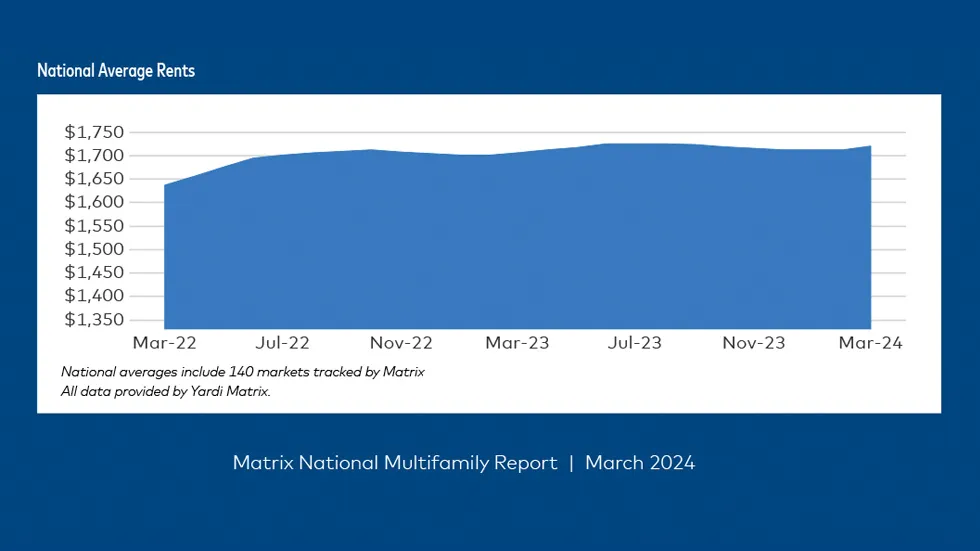

The national average asking rent grew by 0.9% year-over-year in March, according to Yardi Matrix data, whereas a number of Midwest and Northeast markets posted annual rent growth between 3% and 4%. So, there are mixed signals due to the nuances in different markets with the high growth submarkets struggling while others are still performing quite well, he adds.

“It’s a bifurcated market right now. Coastlines are outperforming due to low supply, ironically due to housing policy that has disincentivized development and landlord unfriendly policy,” says John Panichi, head of U.S. equity sales trading at Mizuho. The Sunbelt is now the sole focus of concern due to elevated supply, higher incentives, and falling rents, he says. However, while Sunbelt properties are expected to underperform in the short to medium term, cap rates are now around 6.5%. “Even if you discount the numbers and argue its high fives to low sixes, that is starting to look very attractive for a space that is need-based,” he adds.

According to CBRE data, average monthly rents in the first quarter edged up 0.4% compared with 2023. Meanwhile, 73,700 new units came online, contributing to a record four-quarter total of 429,500 units.

Despite a slight increase in the multifamily vacancy rate in the first quarter, strong demand led to net absorption of 52,500 units, marking the third-strongest first quarter in more than 20 years and surpassing the pre-pandemic first quarter average, CBRE said. “Absorption has remained surprisingly resilient despite the record deliveries over the last few quarters,” said Kelli Carhart, leader of multifamily capital markets for CBRE. “Investors continue to display a strong conviction towards multifamily. We expect multifamily capital allocation and deployment to increase as the year progresses.”

Goldstein adds that absorption of the new space is moving faster than some had expected. “I think a lot of that relates to the strength of the economy and job growth and wage growth that we're continuing to see,” Goldstein says. “That has really helped Sunbelt markets but it's still not too pretty of a picture out there.” Many of the Sunbelt markets are seeing negative rent growth and elevated concessions, he adds.

Pain Points Likely Temporary

Camden Property Trust (NYSE: CPT) is one REIT with a strong presence in Sunbelt markets. Although market challenges are squeezing gross revenues, occupancies across its portfolio are holding up well at 95.4%, according to the REIT’s first quarter results.

“Folks are looking at the supply numbers and expecting the results to be worse than they are because they are overemphasizing supply and underemphasizing demand,” says Alex Jessett, Camden president and CFO.

“The demand is incredibly strong and because of that we are able to absorb the supply,” he says. In particular, there is still a steady flow of people moving into Sunbelt cities from other regions. For example, 18% of all Camden move-ins during the first quarter were from renters who were relocating from places outside of the Sunbelt.

Broadly speaking, it also is important to note that there is still a housing shortage and bigger affordability hurdles in the for-sale housing market that are contributing to robust renter demand. Developers also are pulling back from new projects due to higher costs. According to RealPage, multifamily construction permits for March were down 22% on a year-over-year basis, while construction starts were down nearly 44%.

“As we look forward, we're very encouraged by the permitting and starts data that we're seeing on a national level. We think that when we're through the run of deliveries later this year, we should have a very good setup into next year and the following year in terms of competitive supply in the market,” says Goldstein at CenterSquare. Even for the more supply challenged Sunbelt markets, supply and demand will be more in balance 12 months from now as that new space continues to be absorbed, he adds.

Will REITs Play Offense or Defense?

Views are somewhat mixed on whether, like Blackstone, REITs are ready to make some bold moves to acquire assets and grow portfolios, or whether they are more apt to move cautiously considering near-term pressure on revenues.

After stellar performance through the COVID period, multifamily REITs are now experiencing a bit of underperformance and are trading at discounts to NAV. Those REITs with more exposure in the Sunbelt are trading at slightly bigger discounts relative to their coastal peers, which are still performing relatively well.

“We think that the valuation setup is very compelling. They're trading close to a 7% cap rate, and we're still seeing trades in the private market in those markets that are closer to 5%. So, there's quite a big disconnect between the public and private market cap rates,” Goldstein says.

Discounted NAVs may make it difficult for multifamily REITs to be aggressive on the acquisition front. That being said, there could be more take private deals ahead, especially if the disconnect between the public and private sector valuations doesn’t narrow. “I suspect that as we begin to see the light at the end of the tunnel as it relates to supply deliveries, that's when the public markets will start to value these companies a little bit more appropriately,” Goldstein notes.

There is a lot of capital on the sidelines, including the public REITs, and that capital will start to move off the sidelines and start looking for buying opportunities once there is more clarity on cap rates. One portfolio deal that institutions are watching closely is the Lennar portfolio sale. The company’s multifamily development group, Quarterra, is marketing its roughly 11,000 luxury apartment units for sale in a deal that is reportedly worth $4.5 billion.

“Obviously, AIR is helpful. But adding the Lennar transaction, assuming that closes, is going to set a mark for what cap rates really are,” Jessett says. “I think that that will likely loosen up some sellers and buyers and help them become a little bit closer in terms of the bid ask spread.”

In its first quarter earnings call, Camen said that it is still assuming $250 million in acquisitions for 2024 along with $250 million of dispositions. Although Camden is well positioned for acquisitions due to a strong balance sheet, the REIT is waiting for more data points before engaging.

Potential New Development

Markets with higher levels of new supply will continue to absorb that space in 2024 and 2025. However, by 2026 and 2027, Adler expects that the industry could be moving towards another upcycle as vacancies tighten.

REITs have a cost of capital advantage that could position them as first movers in stepping back on the gas with regard to new development. Most apartment developers are looking at higher cost construction loans that are now between 9% and 10%, which is making it difficult for new projects to make sense. In comparison, REITs have the option of doing an unsecured bond, which for investment grade rated REITs, could be 100 to 150 basis points over the 10-year, or 5.5% to 6.5%.

“The question that a lot of us are trying to understand is, if construction costs start to roll back, plus you have very low starts and continued demand, that would be a great opportunity to start some development. So that's what we're all watching,” Jessett says.