In the second quarter of 2022, continued solid fundamentals reflect an ongoing healthy demand for commercial real estate across most sectors, even as concerns about a slowing economy dominate the outlook.

- Despite uncertain economic conditions, the apartment and industrial sectors saw near-record and record levels of construction, respectively. The office and retail experiences were considerably more subdued. Read more.

- Net absorption continued to outstrip net deliveries for both industrial and retail, while apartment and office demand fell short of their respective supply counterparts. Although recovering, office has maintained a chronic struggle with demand since the pandemic. Read more.

- Market fundamentals have driven office and apartment vacancy rates higher, and industrial and retail vacancy rates lower. Despite the uptick, apartment availability remained tight. The industrial vacancy rate reached its all-time low. Read more.

- Commercial real estate rental growth rates maintained positive four-quarter gains across all sectors. The apartment and industrial sectors maintained four-quarter growth near or above double-digits. Retail and office rents continued their recoveries. Read more.

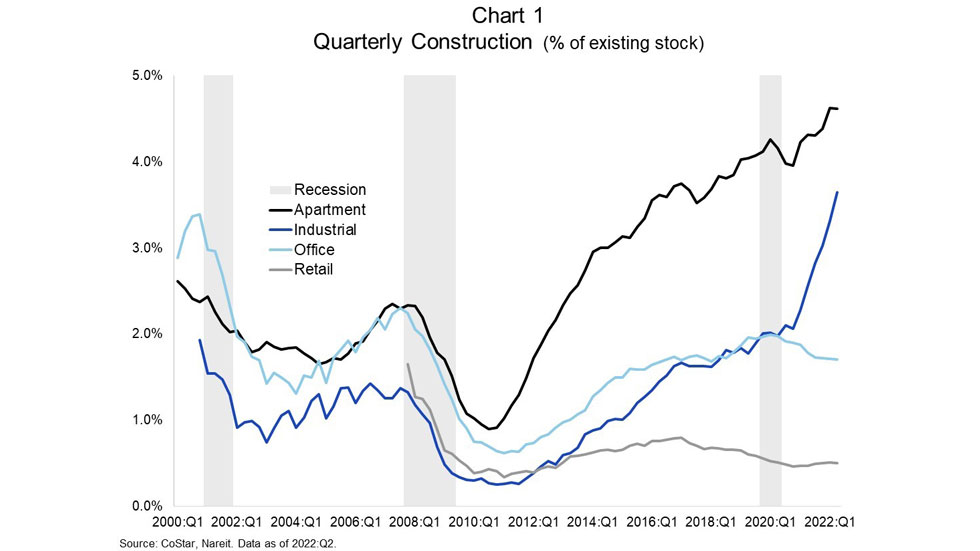

As shown in Chart 1:

- In the second quarter of 2022, apartment construction as a percent of existing stock remained near its peak level at 4.6%. This pace of construction activity approximately doubled the sector’s average in the year prior to the Global Financial Crisis (GFC).

- Industrial construction has surged during the pandemic. As of second quarter of 2022, nearly 650 million square feet of new facilities were under construction. This level of building equaled 3.6% of existing stock, marking an all-time high.

- With the uncertainties over how work from home may impact the sector, office construction has waned. In the second quarter of 2022, construction was 1.7% of existing stock; it has remained below its post-GFC and pre-pandemic high.

- Retail construction has been relatively flat throughout the pandemic. It has maintained a level around 0.5% of existing stock since the middle of 2019. In the second quarter of 2022, there were 59.4 million square feet of retail properties under construction.

Supply & Demand: Net Absorption & Net Deliveries

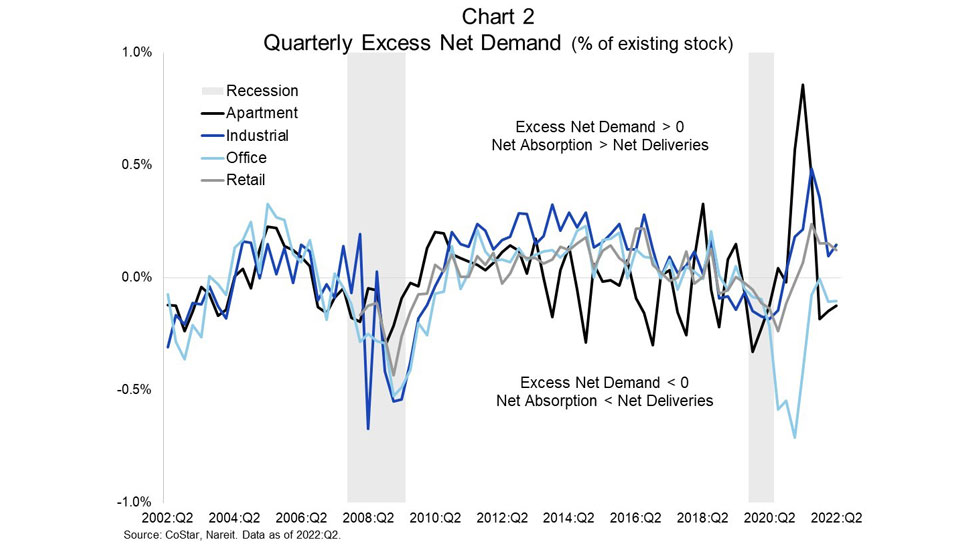

As illustrated in Chart 2:

- The seasonality of apartment demand is highlighted in the data. Net deliveries continued to outpace net absorption for the third quarter in a row. This followed three quarters of excess net demand being at its highest levels ever.

- Industrial has high levels of demand and supply. In second quarter of 2022, net absorption and net deliveries equaled 98 million and 94 million square feet, respectively. Excess net demand has been positive for seven straight quarters.

- Office markets have struggled with demand. Net absorption was 4.5 million square feet; the sector’s fourth consecutive quarter of positive demand following five quarters of negative values. Even at low levels, supply continued to exceed demand.

- The retail sector has continued to experience very little new construction. In the second quarter of 2022, it saw its fifth consecutive quarter of robust demand that has resulted in positive excess net demand, i.e., net absorption exceeded net deliveries.

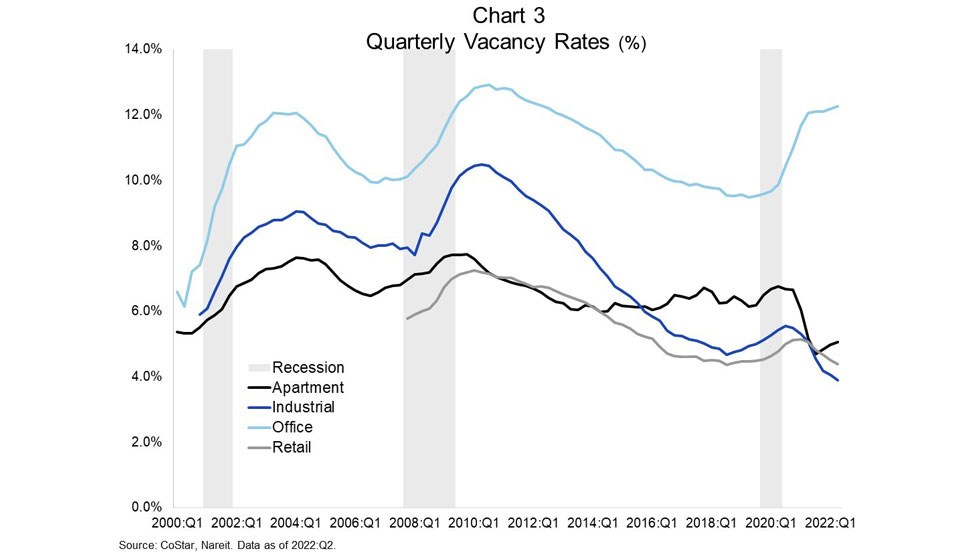

As displayed in Chart 3:

- While apartment vacancy rates ticked up slightly higher to 5.1% in the second quarter of 2022, they remained well below their historical average. Vacancy rates have been below 6% for the past four consecutive quarters; they have not been below 6% since 2001.

- In the second quarter of 2022, industrial vacancy rates declined by 16 bps to 3.9%, reaching an all-time low. While there was a modest increase in vacancy rates at the beginning of the pandemic, the sector is now performing better than ever.

- Office vacancy stayed relatively flat, increasing 9 bps to 12.3% in the second quarter of 2022. The sector has been the hardest hit by the pandemic in terms of vacancy rates. A meaningful improvement in the vacancy rate is unlikely without increased demand.

- Recent elevated demand combined with limited supply has benefited the retail sector. The retail vacancy rate declined by 13 bps to 4.4% in the second quarter of 2022. This is the lowest vacancy rate for the sector since the third quarter of 2018.

Fundamentals: Rental Growth Rates

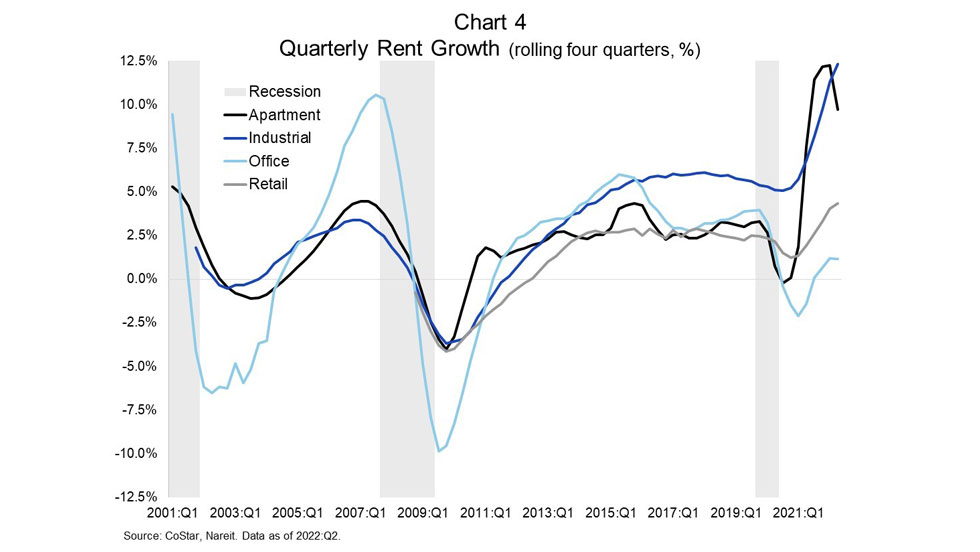

As highlighted in Chart 4:

After three consecutive quarters of double-digit growth, the rolling four-quarter apartment rental growth rate moderated to 9.7% in the second quarter of 2022.

In the second quarter of 2022, industrial rent growth continued to accelerate. Rents increased 12.3% over the last four quarters and 3.1% over the last quarter. The sector has experienced the highest rents and rent growth rates on record.

Office rents experienced a major slowdown during the early stages of the pandemic with four-quarter growth falling to a low of -2.1%. Growth has been recovering, but it remained modest at 1.2% in the second quarter of 2022; far below pre-pandemic levels.

In the second quarter of 2022, retail rent growth accelerated slightly increasing 4.4% over the past four quarters and 1.2% over the last quarter. Rents have been steadily increasing and are at their highest levels of growth on record.