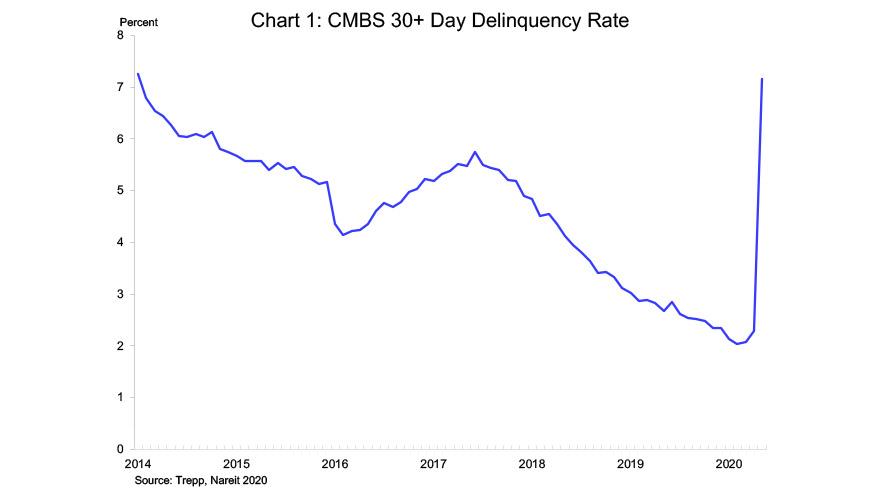

The percentage of mortgages held in commercial mortgage-backed securities (CMBS) that were 30+ days delinquent jumped from 2.29% in April to 7.15% in May due to tenants who have lost business during the COVID-19 crisis.

Trepp reported that an additional 7.6% of loans by loan balance missed their May payments but are less than 30 days delinquent. If many of these loans remain delinquent, Trepp warns we may see another large increase in the 30+ day delinquency rate in June.

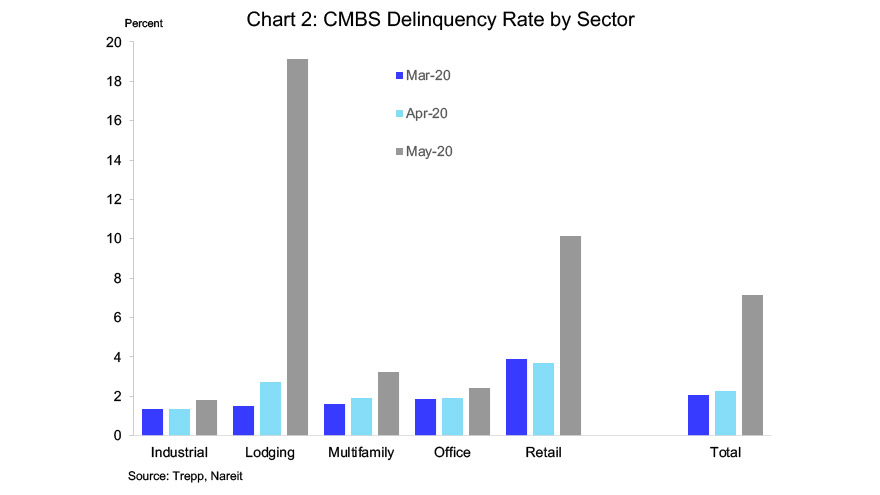

Credit issues are not spread evenly across property sectors, however, but are concentrated in loans secured by lodging and retail properties. The 30+ day delinquency rate on lodging loans rose more than 16 percentage points, to 19.13%, while the delinquency rate on retail mortgages rose 650 basis points, to 10.14%. Credit troubles in these two sectors are likely to continue to deteriorate in the months ahead.

Outside of these two sectors, however, delinquencies are little changed from pre-COVID-19 levels. The delinquency rate on loans to multifamily properties rose 133 bps, to 3.25%, while the delinquency rate on loans secured by office or industrial properties rose less than 50 bps.

There are three takeaway messages from the latest CMBS delinquency data. First, the sharp rise in delinquencies underscores the impact of the COVID-19 crisis on commercial real estate markets, and that conditions are likely to continue to deteriorate further in the near term. Second, the most severe impact remains concentrated in a few front-line sectors. This could prove beneficial during the recovery phase once the health issues are better controlled, as underlying business conditions remain sound for many parts of the economy.

The third point draws a contrast between the pool of borrowers that are represented in the CMBS markets compared to REITs. CMBS include loans secured by a wide range of property types, including both high-quality and also older, lower-rated properties, and are owned by companies with both stronger and weaker financial condition. REIT-owned properties, in contrast, tend to be higher-grade institutional quality. The REIT industry also has a solid financial base, with most REITs having reduced their leverage compared to during the Global Financial Crisis (GFC) of 2008-2009.