07/16/2015

| by

The recovery in commercial real estate markets continues to gain momentum. The following charts track the progress in transactions volumes, commercial property prices, financing, new construction, and macro fundamentals.

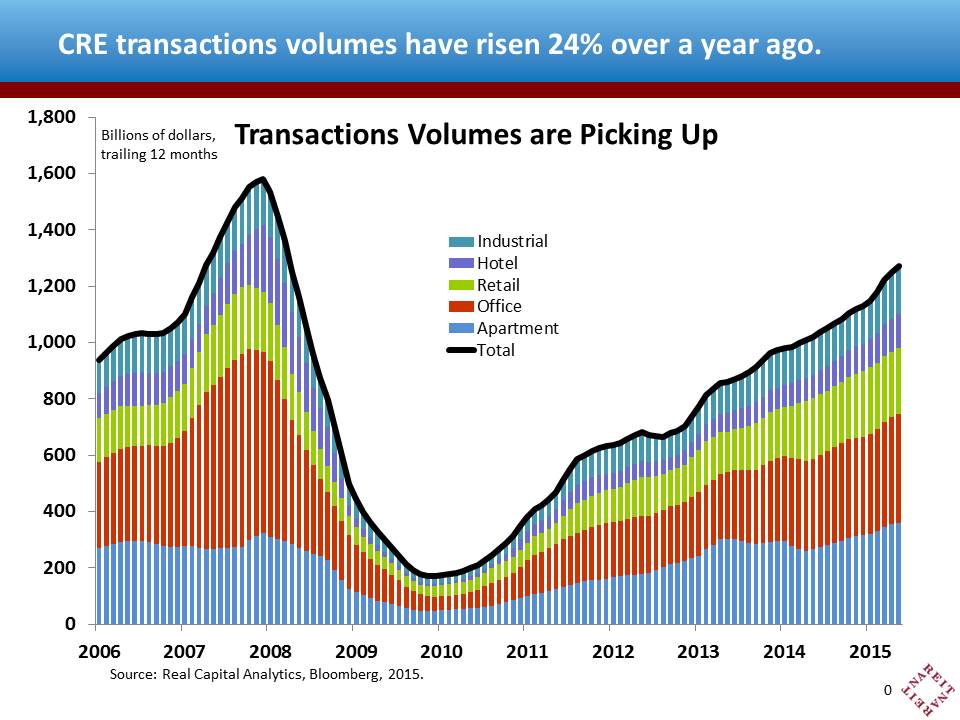

- Transactions volumes of all property types are up 24% over a year ago. The apartment market remains hot, with transactions up 35%, and sales of hotel properties have risen more than 40%. Increases of industrial and office properties have also been robust, at up 25% and up 21%, respectively. Only the retail sector is in the single-digits, with a 9% rise.

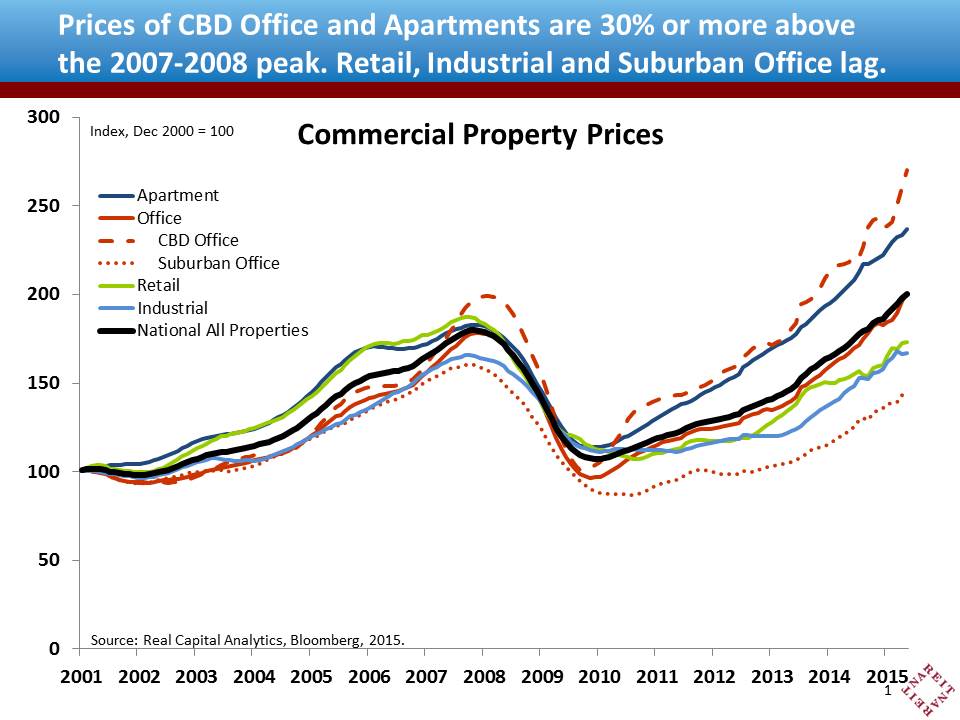

- Commercial property prices are rising across all sectors, but the progress of the recovery has not been evenly distributed. Prices of CBD Office and Apartments are 30% or more above their pre-crisis peak. Prices of retail, industrial and suburban office properties, however, remain below levels reached in 2007 and 2008. After a slow start in the recovery, though, the retail, industrial and suburban office sectors have posted double-digit price increases over the past 12 months—an encouraging sign that the recovery is spreading more broadly.

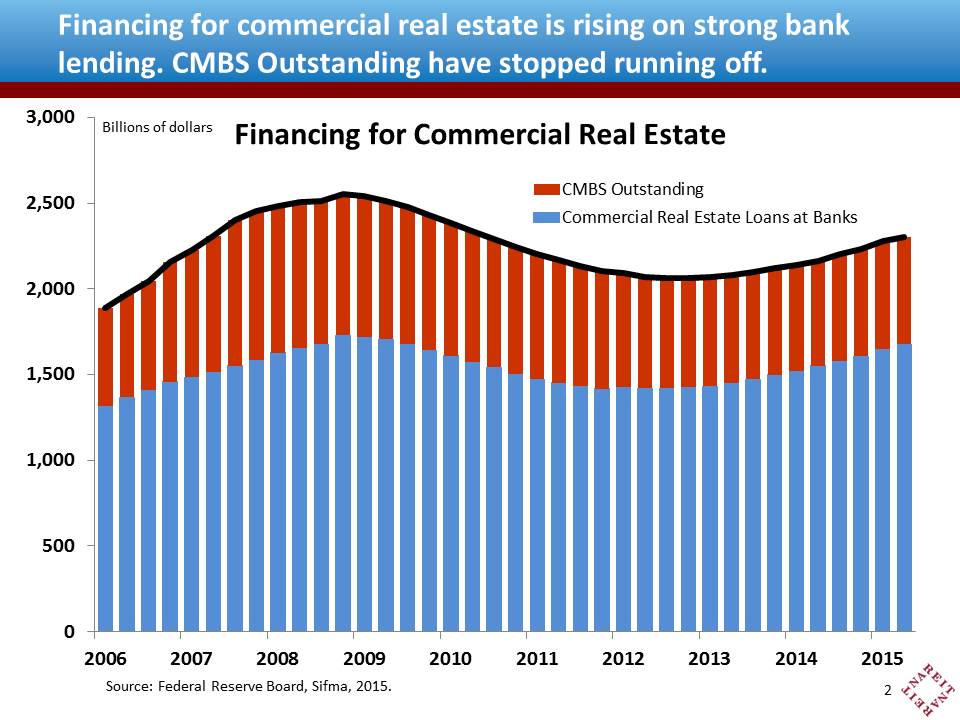

- Financing is available for CRE. Banks have increased their lending to commercial real estate. Commercial mortgage lending at U.S. banks rose more than 8% over the past twelve months, a significant acceleration from the period through 2013, when they increased little or not at all. Gross issuance of CMBS is also up. This has not resulted in a net source of funds for the sector, however, due to the need to refinance the 7-year CMBS that had been issued prior to the crisis.

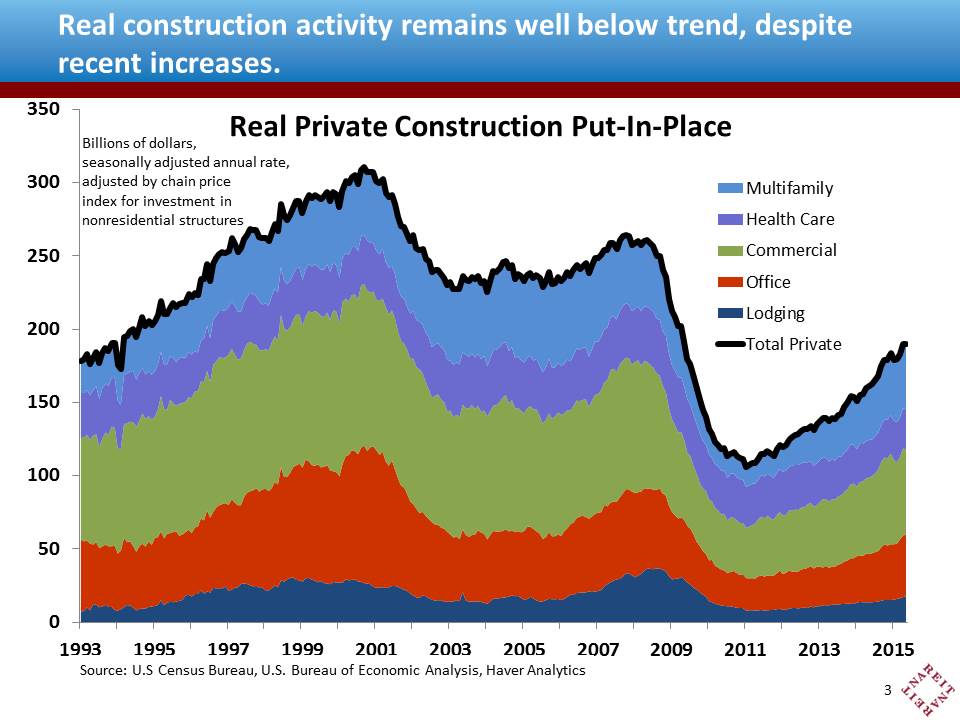

- Construction is ramping up. Investment in commercial buildings (in inflation-adjusted dollars) rose nearly 20% over the past 12 months, with activity in hotels, office and multifamily rising more than 20%. The increase in construction activity reflects not only the stronger outlook for the sector, but also the depths to which construction fell during the Great Recession and early in the recovery. Despite the recent increases, real construction activity is still below levels from 20 years ago, and will have to rise significantly further before new supply threatens to flood the market.

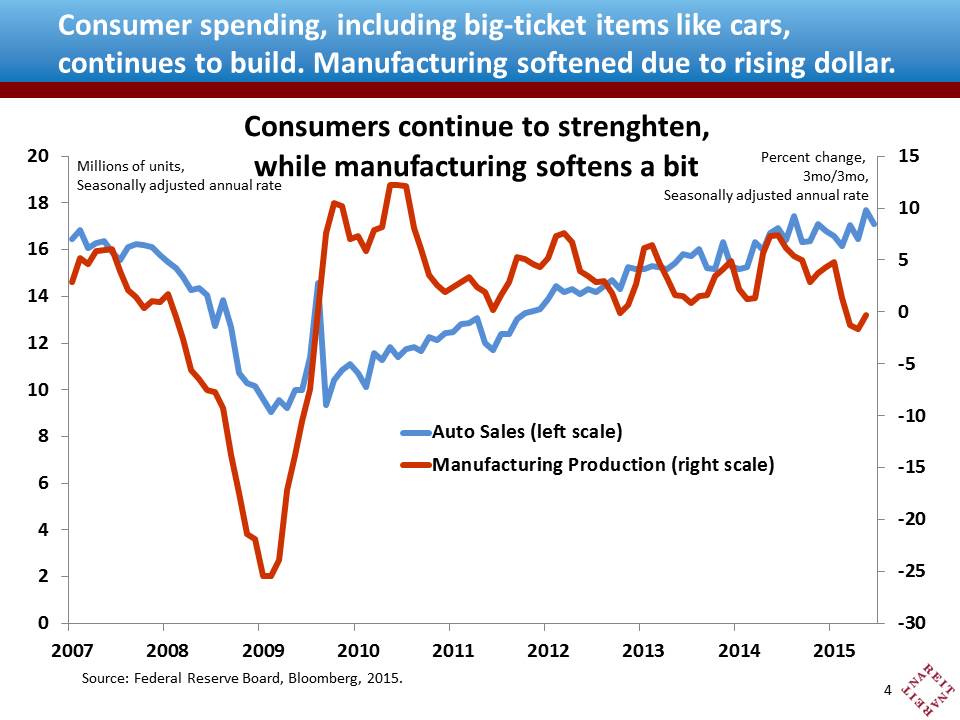

- Macro fundamentals have maintained momentum. After an apparent pause in the winter, most macro indicators have resumed trend growth. The monthly payroll numbers show robust increases, with job growth averaging 254,000 a month in Q2. Consumers are increasingly willing to spend on big-ticket items like automobiles, which so far this year have been averaging nearly a 17 million unit sales pace, the highest since 2005. A stronger dollar, however, has crimped export demand, which has contributed to a decline in manufacturing output so far this year.