With mixed economic growth results, waning job gains, increasing interest rates, and rising recession risk, the U.S. economy is facing numerous headwinds. Recent data from CoStar highlight the current state of commercial real estate fundamentals—excess net demand, occupancy rates, and rental growth rates—across property types. In the third quarter of 2022, property fundamentals across most sectors generally remained solid, but the office sector continued to face challenges.

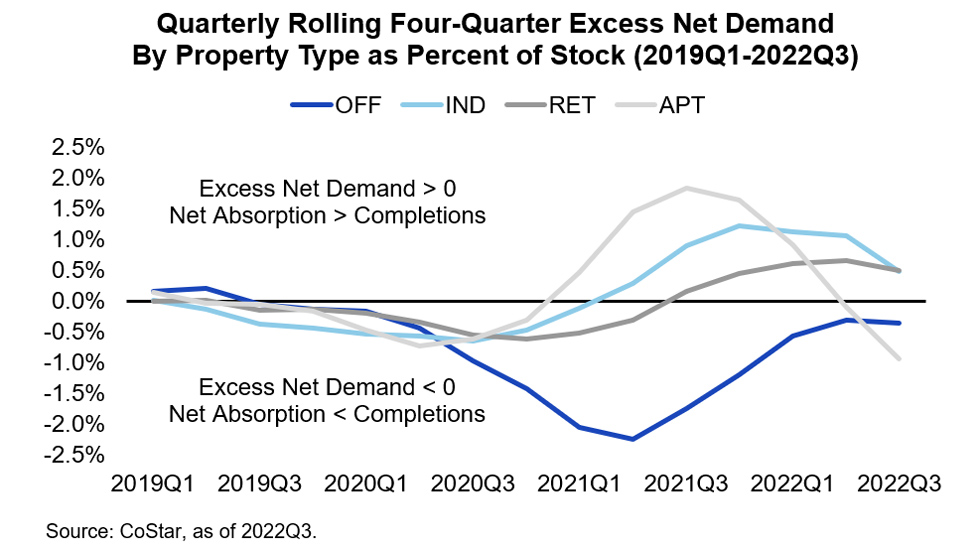

The above chart displays quarterly rolling four-quarter excess net demand (or net absorption less completions) as a percentage of existing stock by property type. Excess net demand weakened across each of the four major property types in the third quarter of 2022. Net absorption exceeded completions for the industrial (0.5%) and retail (0.5%) sectors. Demand fell short of supply for the apartment (-0.9%) and office (-0.4%) property types. While the precipitous fall-off in apartment excess net demand rate may cause a sense of foreboding for some investors, the decline likely reflects the sector’s movement toward equilibrium. Three years of negative excess net demand capture the plight of office, but the sector has been making progress in its effort to achieve demand and supply balance.

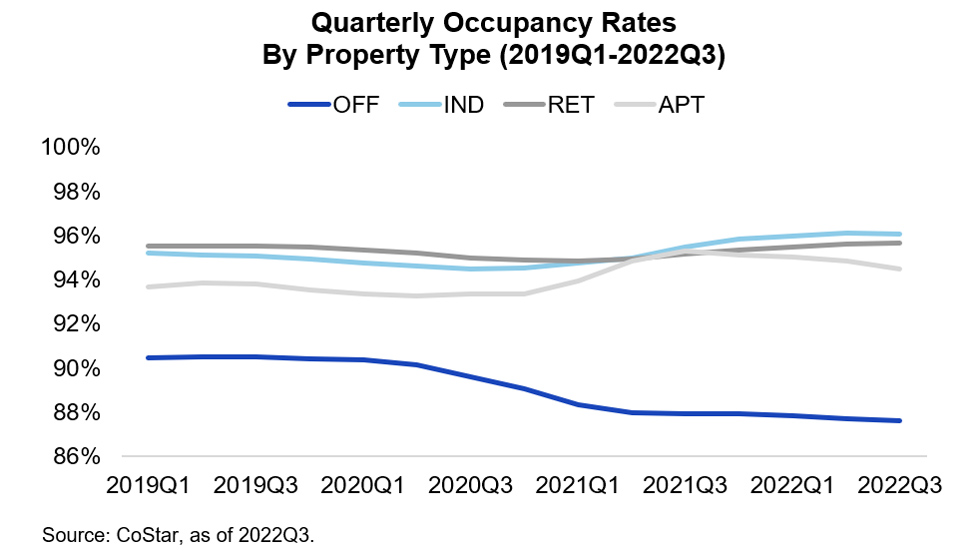

The above chart shows quarterly occupancy rates by property type. As of the third quarter of 2022, occupancy rates for the industrial, retail, apartment, and office sectors were 96.0%, 95.7%, 94.5%, and 87.6%, respectively. The industrial, retail, and apartment property types maintained elevated occupancy rates that were higher than their respective pre-pandemic (2019Q1 to 2019Q4) levels. Office occupancy continued its downward trajectory, dropping nearly 3% from its 2019 average. The decline reflects a persistent demand and supply imbalance. Despite demand struggling since 2020, office completions have not yet slowed; they have sustained a consistent pace since 2015.

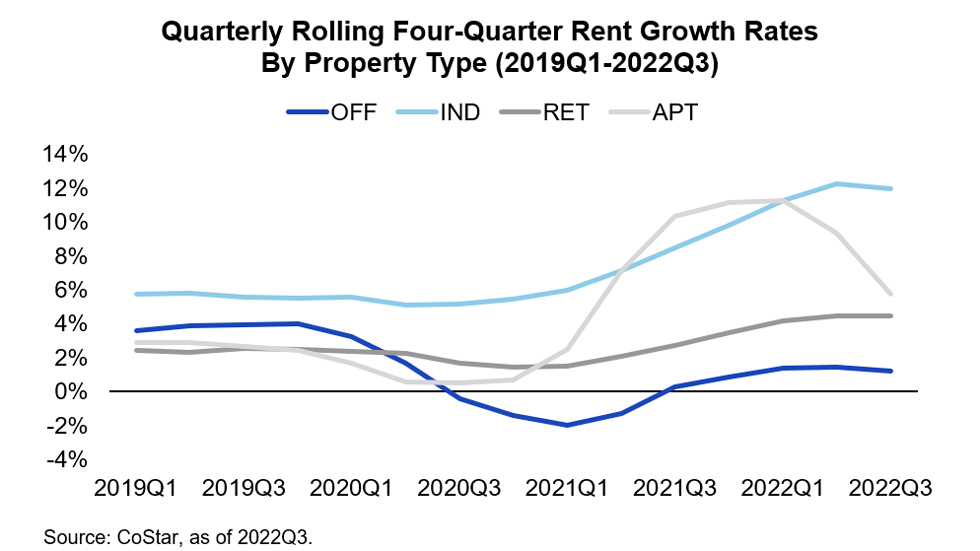

The above chart displays quarterly rolling four-quarter rent growth rates by property type. Similar to the trends observed with occupancy rates, the office sector has been the laggard. Nonetheless, it continued working toward achieving positive rent gains. As of the third quarter 2022, one-year rental growth rates for the industrial, apartment, retail, and office sectors were 12.0%, 5.7%, 4.5%, and 1.2%, respectively. The drop in the apartment rent growth rate is striking. Prior to raising a cautionary flag, it is important to note that apartment occupancy and rental growth rates are approaching 95% and near 6%, respectively. Given these metrics, apartment fundamentals remain solid.