Investment real estate values declined by -0.32 percent during April 2016 according to the FTSE NAREIT PureProperty® Index Series, which provides the earliest measurement of changes in the market values of properties held for investment purposes. The Midwest and East regions saw slight improvements in property values by +0.67 percent and +0.63 percent respectively, while property values dipped in the South and West regions by -1.46 percent and -1.12 percent respectively.

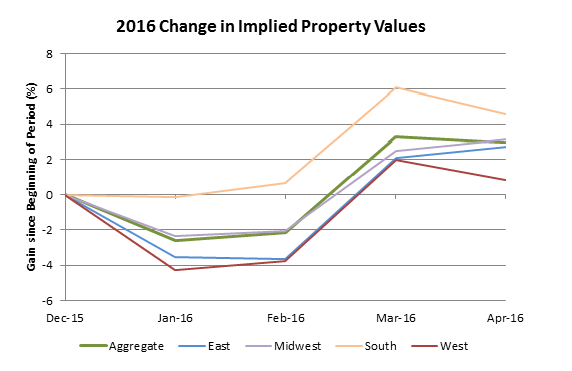

Notwithstanding the relatively flat results for April, property values nationwide as measured by the PureProperty Index have increased strongly at +2.96% since the beginning of the year. The South region has seen the strongest year-to-date gains at +4.57%, while property values increased by +3.17% in the Midwest region and +2.72% in the East region. The West region has lagged slightly behind the rest of the country with property values having increased by just +0.82% since the beginning of the year.

With income from property investments averaging +0.24% nationwide, total returns were only barely negative during April at -0.08%; since the beginning of the year, however, income of +1.27% has combined with strong property appreciation to provide total returns averaging +4.24%. Year-to-date total returns have been strongest in the South region at +5.94%, with the Midwest and East regions also strong at +4.75% and +3.95% respectively; the West region has lagged slightly with total returns averaging +1.80%.

The PureProperty Index Series, launched last year, provides a daily measure of U.S. real estate price and total returns at the level of both property (unlevered) and equity investments. The index series infers changes in the market values of apartment, health care, hotel, industrial, office, and retail properties owned by stock exchange-listed U.S. equity real estate investment trusts (REITs) by relating observed changes in stock prices to the property holdings of each REIT and correcting for the effect of each REIT’s capital structure.

Because it evaluates returns by geographic region as well as by property type, the PureProperty index series can help investors take advantage of performance differences among targeted segments of the U.S. property market through diversified exposure to properties in each segment. During April, for example, office properties in the Midwest region significantly outperformed those in the South region, with implied property values increasing by an average of +6.18% for the Midwest region Office segment compared to +0.91% for the South region Office segment, and total returns averaging +6.35% compared to +1.13%. Similarly, over the first four months of the year retail properties in the South region have outperformed those in the East region with implied appreciation averaging +8.25% and +2.45% respectively.

Property-level (unlevered) returns averaging -0.08% nationwide outpaced equity returns (averaging -1.17% according to the PureProperty Index Series), which can happen when unlevered returns are not strong enough to outweigh the cost of borrowings. Equity returns measured by the PureProperty Index Series (-1.17%) outpaced equity returns measured by the FTSE NAREIT Equity REIT Index (-2.39%), reflecting underperformance during April among several equity REITs that are not constituents of the PureProperty Index Series including those holding self storage properties and manufactured home communities.