REITs are an investment grade sector, as companies with investment grade ratings by Moody’s and Standard & Poors comprise 70% of the total market capitalization of the industry.

The financing choices a company makes can have a big impact on their profitability and also their resilience to future shocks. Leverage, the ratio of debt to assets, gets most of the attention, but the composition of debt matters as well. REITs have made important changes over the past decade in their overall leverage ratios, as well as the composition and structure of their debt. These financing choices have helped reduce REITs’ financing costs, and have also strengthened their balance sheet positions and improved their flexibility for the future.

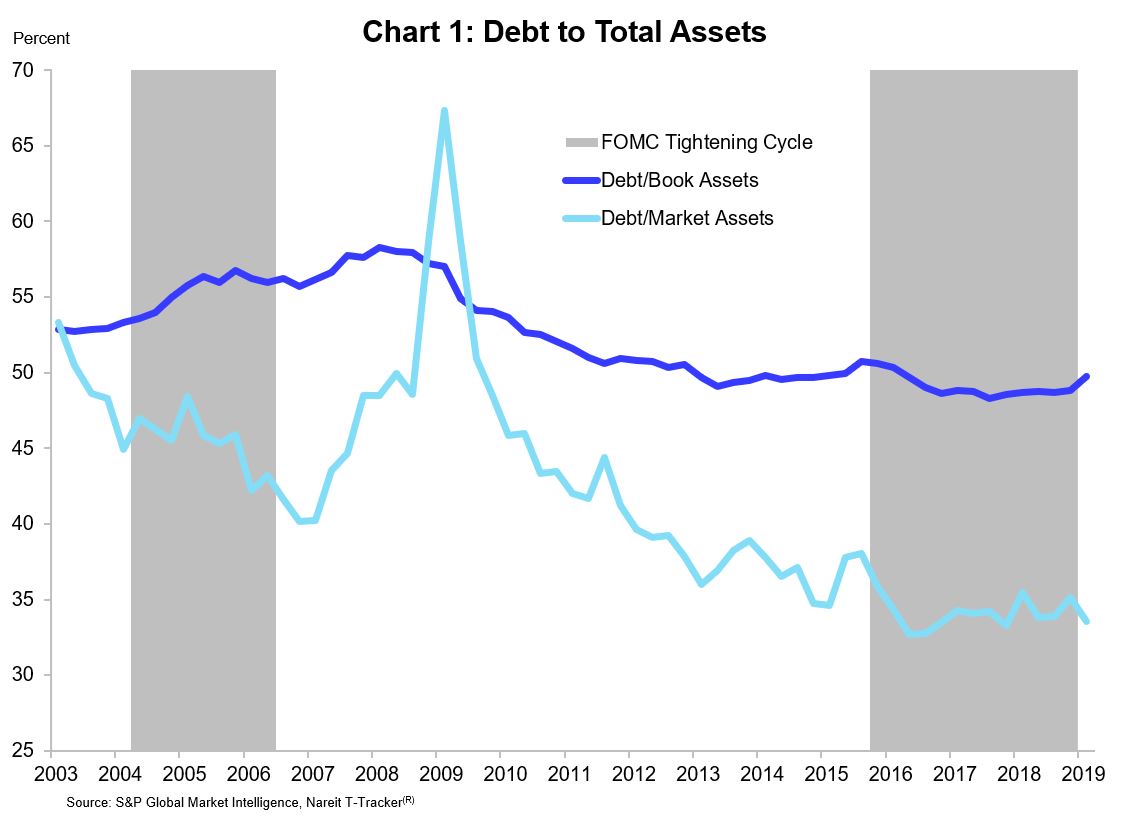

Lower leverage. REITs have reduced their overall leverage ratios to the lowest in at least two decades (chart 1, for more see Nareit’s T-Tracker). The ratio of debt-to-book assets was 50.6% in 2019:Q1, compared to a peak of 58.3% prior to the financial crisis. REITs reduced leverage by raising significant amounts of equity capital while making sparing use of debt to fund their portfolios. Lower debt ratios, and the correspondingly higher capital cushion, provides a strong base to withstand future market events, as well as dry powder for acquisitions should the opportunity arise.

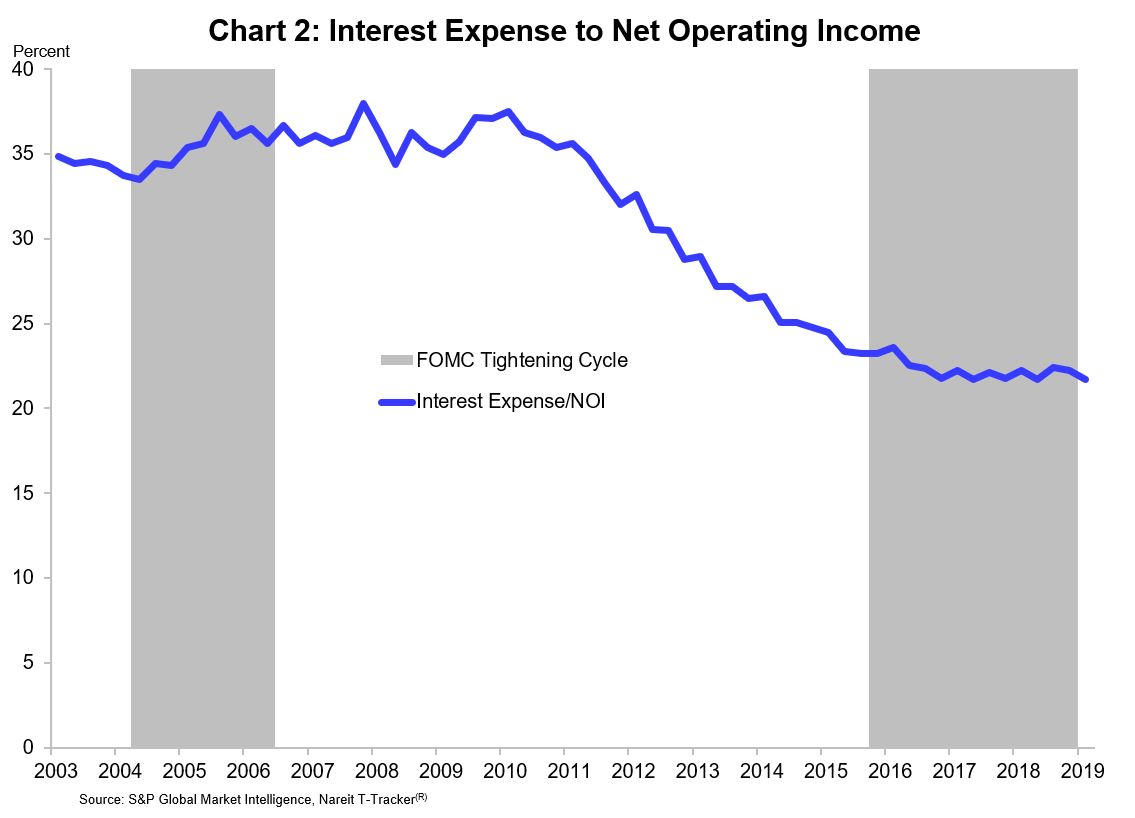

The decline in REIT leverage, combined with the low level of interest rates, has reduced interest costs (as a share of NOI) to a record low (chart 2). The weighted average interest rate paid on REITs’ long-term debt declined 200 basis points, from 6.0% in 2009 to 4.0% in 2019:Q1, according to the Nareit T-Tracker. Lower interest costs benefit investors in REITs as a larger share of revenues is available for earnings and dividend payments.

Lengthened debt maturities. REITs have lengthened the average maturity of debt outstanding to 75 months, up from 60 months a decade ago. REITs have thus locked in low interest rates well into the next decade (chart 3).

.JPG)

Reduced reliance on secured debt. REITs have shifted their capital structure away from mortgages (secured debt) toward bond issuance (unsecured debt). Before the financial crisis, total debt was evenly split between secured and unsecured. In 2019Q1, however, unsecured debt encompassed two-thirds of total debt for REITs. Unsecured debt provides more flexibility and is usually lower cost compared to mortgages. In contrast to mortgage financing, which is tied to a specific property, bond financing leaves more properties unencumbered over time.

The greater use of unsecured financing in part reflects the stronger financial position of the REIT industry overall, including the reduced leverage discussed above. Access to unsecured debt is greatest for those REITs with an investment grade bond rating. In 2006, 44 REITs had an investment grade rating, but by 2019 the number of investment grade REITs had increased to 68. The investment grade stamp offers REITs more financing opportunities and lower interest rates and reflects a stronger financial position.

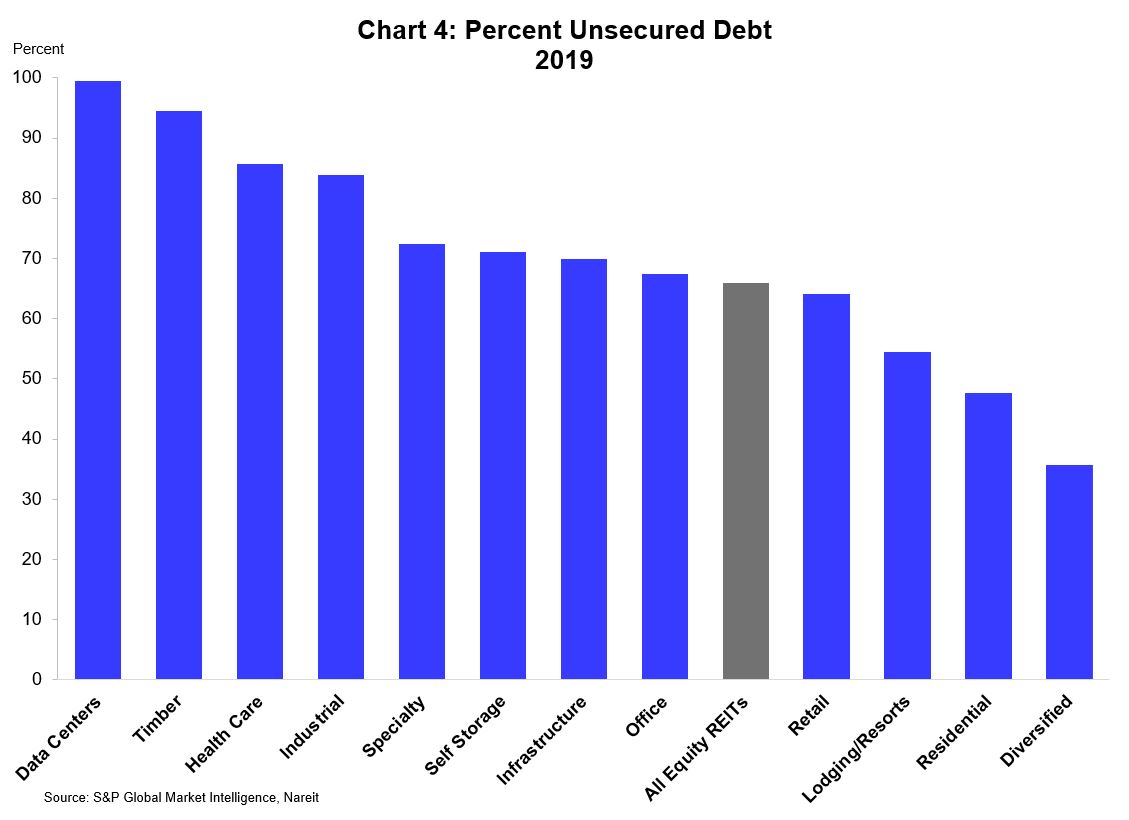

Like the properties they own, the amount of unsecured debt used varies widely by sector (see chart 4). Data centers use the most unsecured debt, 99.4%, while diversified REITs use the least, 35.6%. Residential REITs rely heavily on secured debt, in part because Fannie Mae and Freddie Mac provide support and funding to the multifamily mortgage market.

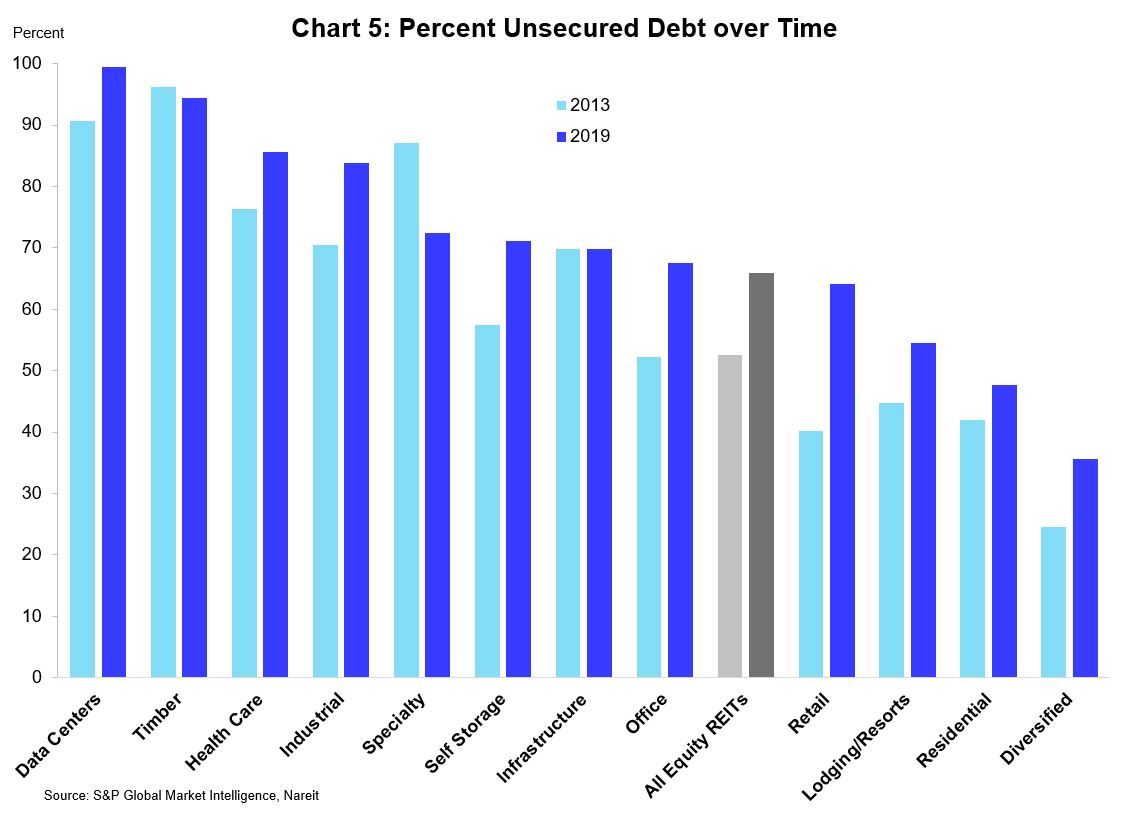

The use of unsecured debt has increased for all but two of the REIT property sectors (see chart 5). The largest shift away from secured financing was the Retail REIT sector, which reduced the secured share of total debt by 24 percentage points, from 64% to 40%.

Since the financial crisis, REITs have strengthened their balance sheets, reducing interest costs and making them better prepared to withstand potential shocks. Lower leverage reduces the company’s reliance on debt and interest payments, while the greater use of unsecured financing provides more flexibility to REITs and their properties.