As noted in previous market commentaries, efforts to stem the spread of the coronavirus are disrupting economies across the globe. This disruption is affecting and will continue to affect real estate. A recent market commentary discussed why the Lodging and Resorts, Retail and Health Care sectors have been the hardest hit in terms of total return during the month of March.

News reports and the limited data that are available data that hotel stays and occupancy rates have already dropped precipitously, and restaurant traffic is greatly diminished. A number of retailers have closed operations and at least two REIT mall operators have announced they are temporarily closing their facilities in the interest of public safety. Health Care REITs face elevated costs and tenant departures paired with a drop off in new tenants. It is likely that we will see more retail, restaurant and hotel closures as local, state and federal authorities provide increasingly restrictive social distancing guidance and restrictions.

While the timing and full implications of the restrictions and closures are unclear, it is a near certainty that many real estate owners, including REITs, will see delinquencies in rents due and declines in other revenue in April.

REITs enter into this period of economic uncertainty with strong operation performance, however, the lowest leverage ratios in more than 20 years, long debt maturities and high interest coverage ratios.

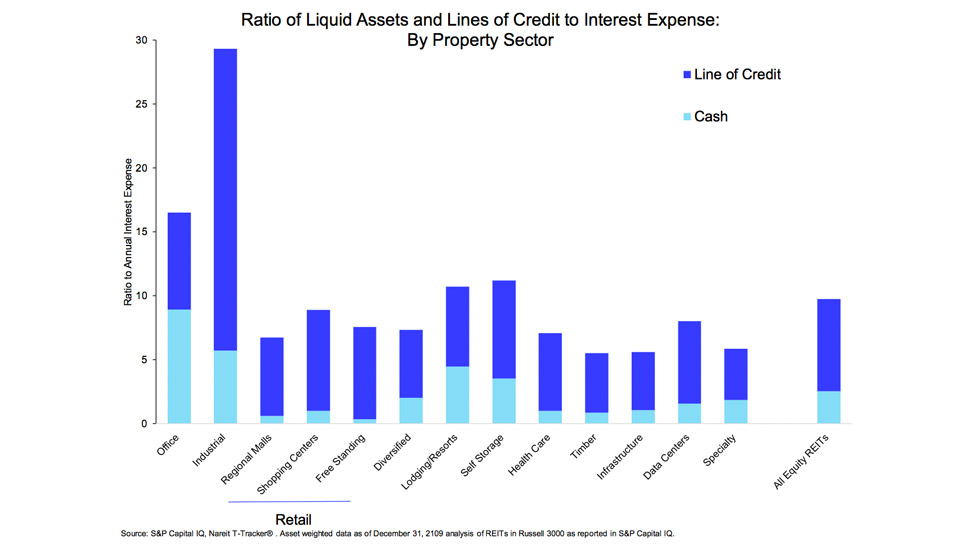

REITs have also prepared themselves for economic uncertainty by building up their stock of cash and cash-like assets and maintaining substantial unused lines of credit. REITs have over $28 billion in cash and nearly $120 billion in untapped lines of credit. Chart 1 below shows the ratio of cash and untapped lines of credit to interest expense by sector as of the end of the fourth quarter of 2019.

As the chart shows, the asset weighted average ratio of cash and lines of credit to interest expense is near 10 for equity REITs, this means that REITs have access to 10 times the cash and credit they would need to make required annual interest payments. REITs hold rough 2.5 times their interest expense in cash and the balance in untapped lines of credit.

Looking across the universe of REITs we find most REITs have a healthy liquidity position, with nearly 90% of REITs (by assets) with a cash and untapped line of credit ratio greater than 3.

In the past few days, we have seen a number mall and hotels REITs announce that they are drawing down part or all of their lines of credit to ensure they have ample liquidity on their balance sheets. This action underscores the value of these lines of credit.