The Sears bankruptcy marks the end of an era, and the famed retailer plans to shutter 142 stores by year-end. There will be many ramifications of these closings, but not all of them are negative. When discussing the outlook for retail, it’s important to keep in mind the distinction between the impact on retail stores and what it means for the owners of retail properties, including REITs.

There’s no question that retailers have been forced to adapt to E-commerce and the changing patterns of consumer spending, and Sears is far from the first casualty. The implications for retail properties, including regional malls, however, are more mixed, with some locations faring much better than others. A key factor that affects how well a property can absorb a loss of tenants due to bankruptcy or other store closings is whether it is a high-productivity mall, with high sales per square foot and busy customer foot traffic. The economic vibrancy of the communities around the mall is also critical in how well the property can rebound from store closings.

Let’s take a look at REITs’ exposures to the Sears store closings, and the economic forces that may help them adapt. Sixty-one of these Sears and Kmart stores (43 percent of the total expected store closings) are in properties owned by REITs, indicating that REITs have a significant exposure to the retailer. It may be costly to remodel the ‘big box’ spaces for new tenants, and there will be a loss of income for the period until new tenants move in.

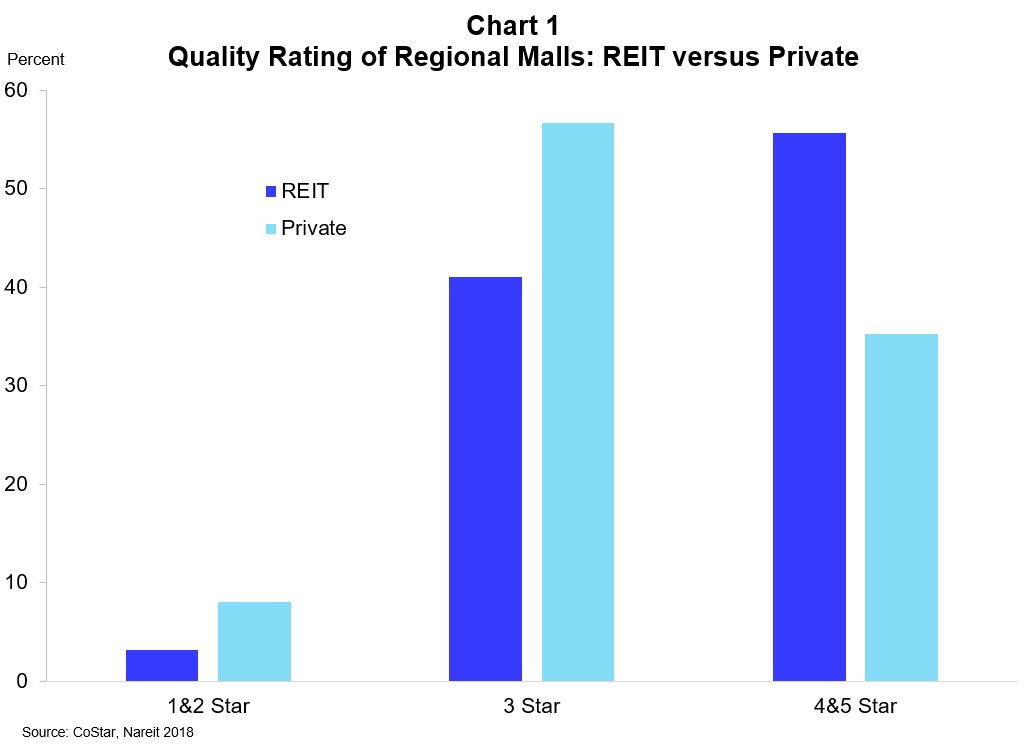

REITs are well-positioned to handle the Sears news, however, and over the longer term could even benefit from bringing in new tenants with fresh product lines. REITs own higher quality properties compared to their private counterparts. Over 55 percent of REIT-owned malls are 4&5 Star quality, the highest quality ratings, according to CoStar, compared to only 35 percent of privately owned malls with such ratings (see Chart 1).

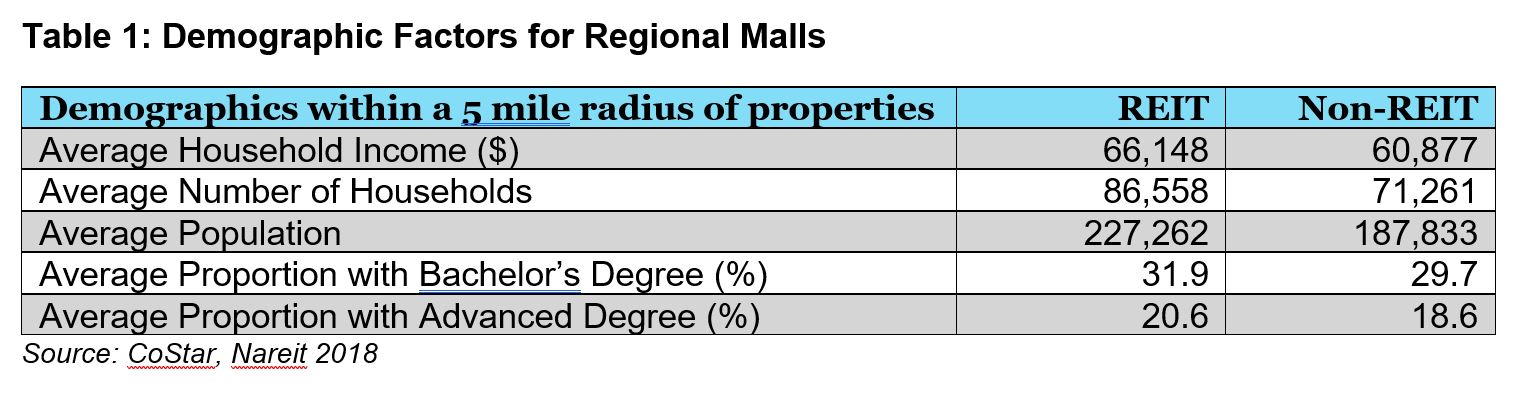

REITs also tend to own properties in locations with higher household incomes, greater population density, and in higher educated areas (see Table 1). Experience shows that properties located in higher-income, more dense communities are better able to attract quality tenants and high customer traffic volumes. These underlying fundamentals provide long-term demand for REITs and their retailers, better positioning them to bounce back from the Sears bankruptcy.

There is another potential upside to REITs, as new tenants with a fresh product line often sign leases at higher rental rates than the old lease. This should not be surprising, as these new retail tenants typically have higher sales volumes and attract greater foot traffic. While there may be some near-term loss of revenues, replacing older tenants like Sears with new stores will ultimately provide a boost to net operating income.

The longer-term future of retail properties depends on bringing in new, higher-productivity tenants as older retailers leave. The malls owned by REITs have a relatively large exposure to Sears but are also high quality properties located in communities with higher incomes and solid economic fundamentals, factors that typically favor retail properties.