REITs Underutilized Despite Outperformance Compared to Private Real Estate

WASHINGTON, DC, (Oct. 14, 2021) — REITs have continued to outperform unlisted real estate investments over a more than two-decade period, delivering higher returns for pension funds. However, despite their strong performance, a newly released study found that many pension funds may still be missing out on REIT benefits by under-allocating to them in their real estate strategy.

The study, conducted annually by research firm CEM Benchmarking, provides a comprehensive look at investment allocations and realized investment performance across aggregate asset classes using a unique dataset covering over 200 public and private sector pensions over a 22-year period, with nearly $3.6 trillion in combined assets under management at the end of 2019. The analysis was commissioned by Nareit.

“As millions of Americans rely on pensions for their retirement security, the investment allocation decisions of pension fund managers are of the utmost importance,” said Nareit Executive Vice President of Research and Investor Outreach John Worth. “The strong returns of REITs shown in this 22-year study reaffirm that pension fund managers and institutional investors should look to REITs as a key component of their real estate investment strategy.”

Key takeaways from the study, entitled “Asset Allocation and Fund Performance of Defined Benefit Pension Funds in the United States,” include:

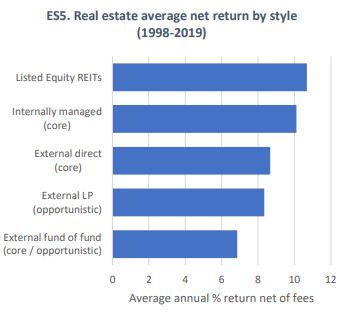

- REITs continued to outperform all styles of unlisted real estate.

CEM compared returns, correlations, and volatilities of four key private real estate ownership styles with varying risk profiles and costs. All styles of unlisted real estate underperform listed equity REITs by between 50 basis points and 3% depending on style.

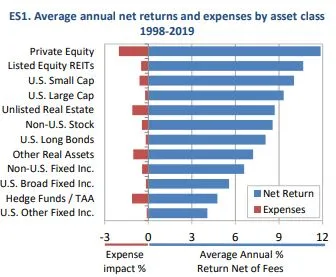

- REITs had the second highest average annual return of the 12 asset classes covered.

Over the 22-year period covered by the study, listed equity REITs had the second highest average net return of 10.7%, falling only shortly behind private equity’s average gross return of 13.9% and average net return of 11.9%.

- Despite their strong performance, REITs were the least used asset class covered in the study.

Over the 22-year period, while REITs had the second highest returns, allocations to listed equity REITs averaged just 0.6% of total assets compared to a 3.8% allocation to unlisted real estate.

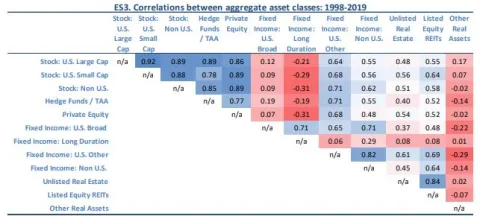

- Listed equity REITs and unlisted real estate were highly correlated.

The study compared correlations of annual returns among the 12 asset classes. Listed equity REITs and unlisted real estate have a high correlation at 0.84. Both listed equity REITs and unlisted real estate were not highly correlated to any other asset classes. REITs had a 0.55 correlation with stocks and 0.48 correlation with fixed income.

- Listed equity REITs and unlisted real estate had comparable volatilities.

The study found that listed equity REITs and unlisted real estate had comparable volatilities. Listed equity REITs and unlisted real estate had the fourth and sixth most volatile net returns with volatilities of 18.9% and 17.9% respectively. Private equity was the most volatile aggregate asset class reflecting high market and idiosyncratic risk.

“Our analysis finds that, historically, REITs have outperformed all styles of unlisted real estate. While factors such as leverage, cost, or geographic differences might play a role, at the end of the day this study made clear that U.S. defined benefit pension funds would have achieved a better net return if they had more REITs and less unlisted real estate, whatever the style, all with a similar level of risk and more liquidity,” said Alex Beath, Senior Research Analyst at CEM Benchmarking.

Learn more about the CEM Benchmarking study at www.reit.com/cemstudy .