U.S. real estate likely will continue to benefit from strong fundamentals, but the high valuations of properties across all sectors will make it harder this year to see any big gains in prices, according to Nareit’s recent conversations with a group of five leading economists.

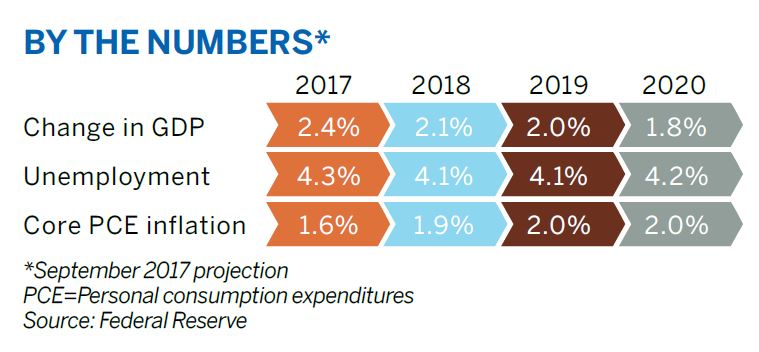

The key reason: an expected rise in interest rates, in part from the belief that the Federal Reserve will continue to raise the federal funds rate this year. That said, economic fundamentals remain decent: Annual growth in gross domestic product is expected to be in the 2 percent range, and unemployment could push down toward 4 percent, meaning more job growth. Real estate sectors such as industrial, suburban office and the condo market look especially promising in 2018.

Our panel also expounded on trends, structural shifts, sectors and cap rates in the coming year.

What’s your general economic outlook for 2018?

Mark Zandi: The economy is performing well. Near-term prospects next year are good. Job creation is double the rate of growth in the labor force. Unemployment and underemployment, which are already low, continue to decline, which means wage growth will accelerate further. That is the fodder for consumer spending, and American consumers make the economic engine move.

Eva Steiner: There are good reasons to remain confident about the U.S. economy: real wage growth, falling unemployment and cheap credit represent an encouraging environment for consumption. Having said that, economic growth of around 2 percent may be the new normal for the U.S. We’re more than eight years into the recovery from the crisis, without a significant boost to productivity or a huge improvement in the global economy.

Mike Fratantoni: We’re looking for GDP growth to average 2 percent for 2018, roughly where we have been in the post-crisis environment. We’re expecting the unemployment rate to drop a little further to just a little over 4 percent this year. We’re running out of workers to hire.

What are some trends either getting affirmed or undercut?

Jim Costello: Retail, in particular, might be a bit oversold. There are clear winners and losers. You are dealing with a structural downturn in the Midwest, with all of the old manufacturing jobs gone away, so the infrastructure there just doesn’t have the value it used to have. Yet, there are fantastic assets sold at very high prices in other regions.

Kim Betancourt: It’s a popular story line that baby boomers are moving into multifamily rentals, but it’s not this huge movement. In 2015, 12 percent of people 55 or older were renting multifamily apartments, up from 11 percent 10 years earlier.

Going forward it might increase another percentage point, but that’s not what is driving the multifamily market.

Steiner: Investors continue to be enthused by the story of industrial investment as a way to buy into the success of internet commerce. The industrial sector has delivered record results, with deal volume even higher than the previous peak levels seen in the third quarter of 2007.

Zandi: There are a lot of technologies on the horizon. But if history is any guide, it will take a long time to for them to diffuse through businesses and really affect productivity growth. These technologies create wealth, incomes and profits. People will spend that wealth, and that creates demand for other things and more jobs.

Fratantoni: Job growth is certainly being affirmed. We really are seeing ongoing strength in business demand for workers. Wage growth hasn’t picked up to the pace that we’ve expected, given all the survey evidence that employers are having difficulty hiring. Our forecast is that will happen in 2018.

What types of structural changes are affecting real estate and why?

Steiner: The growing preference for shared space is huge. We see the impact of technological progress in the office sector, where space per worker has been declining for some time. Telecommuting and working remotely have become real alternatives to going into the office.

Second, there is the trend toward the sharing economy, which includes shared space in office and rental living.

Costello: There’s a lot of buzz around this move toward urbanization. So far, we don’t provide the same incentives for millennials to suburbanize as have been given to past generations. We are saddling these folks with student debt and we are not giving them short commutes, or shiny new suburban infrastructure that our parents had. So, millennials are choosing urban locales.

Zandi: The technological changes are substantive and relentless, and have huge implications for real estate. Online retailers are really doing a number on brick and mortar. Airbnb is beginning to affect the hotel industry. People are not working in offices in the way they used to in the past—that has taken a long time to come to reality, but we are there.

Then you have other technologies seemingly on the horizon that can have real impacts: driverless cars could affect the transportation sector enormously, and the demand for warehouse and industrial space.

Given your overall outlook, what particular real estate sectors might perform well in 2018?

Fratantoni: Besides the single-family market, we do expect a lot of pickup in the condo market this year, with a lot of turnover of existing properties. Given this rise of millennials getting to prime first-time home-buying ages, condos are a natural first place, given the affordability.

Steiner: I see a positive trend for the industrial space, as it continues to serve logistics and delivery centers, especially the last-mile to customer delivery. They may be able to see further rent increases because there is little sign of over-building, in part due to the labor shortages from the reconstruction efforts after last year’s hurricanes.

Costello: Folks are hungry for yield, and in suburban office we are seeing growing deal volumes. There are some good locales in the suburbs, nice walkable business parks, with relatively higher yields compared with national average office cap rates.

Which areas face the most challenges?

Fratantoni: Many multifamily units under construction are going to come online in 2018. There are going to be certain markets that are going to see a big pickup in new units to be leased, especially with higher-end luxury rentals in cities such as New York and Washington. It might take a little bit of time for those to be absorbed.

Costello: The hotel sector continues to be a bit of an issue, and some pockets of the apartment sector as well. They are dealing with some of the same forces in terms of new construction coming into the market and competing with existing assets.

Steiner: I think malls and strip centers continue to be hit the hardest due to the Amazon factor. While the largest proportion of retail sales are still in physical stores, this is likely to change over time. Excess retail space will continue to disappear.

What are your thoughts on interest rates in 2018?

Betancourt: Everyone has been predicting a rise in rates for years. I expect a slowly increasing Fed funds rate, but nevertheless interest rates will remain fairly low over the next two years, with the 10-year reaching 2.5 percent to 2.6 percent by the end of 2018.

Betancourt: Everyone has been predicting a rise in rates for years. I expect a slowly increasing Fed funds rate, but nevertheless interest rates will remain fairly low over the next two years, with the 10-year reaching 2.5 percent to 2.6 percent by the end of 2018.

Zandi: I do expect rates to rise. A lot depends on tax policy. Regardless, there are many catalysts: a tight labor market, wage growth picking up, a stock market at or near record highs, housing values rising quickly, high commercial real estate prices, low cap rates and narrow credit spreads. The Fed needs to normalize rates.

Fratantoni: I don’t see us going into a long-term bear market for bonds. We keep hitting potholes such as sovereign debt crises or geopolitical events that lead to a flight to safety—meaning lower rates—but I do expect the trend is going to be upward, given the removal of central bank accommodation and growing U.S. deficits.

What do you see in the real estate market that seems out of whack?

Zandi: The only place where things seem to be getting frothy is the high-end multifamily sector. Regulators issued guidance to banks in 2016, and things seem to have cooled off. So, I see less worry about that.

Betancourt: There is a lack of affordable rental housing, especially at the lower income levels. As we add more and more of these class-A units, there are fewer units available to lower income residents. For example, in 2011, almost 38 percent of all rental multifamily housing units were affordable to people earning 50 percent or less of the area medium income. Today that supply is down to 30 percent.

Costello: One thing that seems odd is that you have a bunch of folks trying to start up debt funds. Just because you have borrowed money before doesn’t mean you know how to lend money. As a result, the proliferation of players there has me a bit concerned.

What are your thoughts on prices, cap rates and cap rate spreads?

Costello: For the most part, we have squeezed as much as possible out of current cap rates. There’s not going to be too much more compression. Really for about two years, there has been a disconnect of falling volume and rising prices. Buyers and sellers are just further apart. It just makes for a slower market than it was a couple of years ago.

Steiner: Prices have been on the rise all throughout the recovery from the financial crisis, and they now substantially exceed the pre-crisis peak. To the extent that price increases are driven by stronger income growth, that is good news.

Going forward, cap rates may rise, if and when the Federal Reserve raises its target for short-term interest rates.

Betancourt: Property sales are down for multifamily assets. But it’s not a slowdown in investor demand, but available supply for sale. We are at a standoff here. If I am going to sell my multifamily property, I want to get the highest possible price I can get. And if I want to buy a property, I don’t want to pay what I think is a peak price.

Fratantoni: Rates have been so low around the globe, you have foreign investors just looking for yield. Many of them have parked their funds in U.S. commercial real estate, which has pushed up property values. As rates begin to normalize globally, some of that property value increase could be reversed if you get capital outflows, but fundamentals in the sector remain strong.