Rosemarie Thurston, a partner with Alston & Bird and leader of the firm’s REITs and real estate funds team, recently sat down with REIT magazine to share her perspective on changes in the public non-listed REITs (PNLR) market.

How would you describe the mood in the PNLR segment today, compared with just a few years ago?

I think it depends on where you sit. There are two different moods going on. One is quite enthusiastic, and one is not. The oceans have really parted, and those that are enthusiastic are the large institutional managers who are excited about a new source of capital being made available to them—the retail investor.

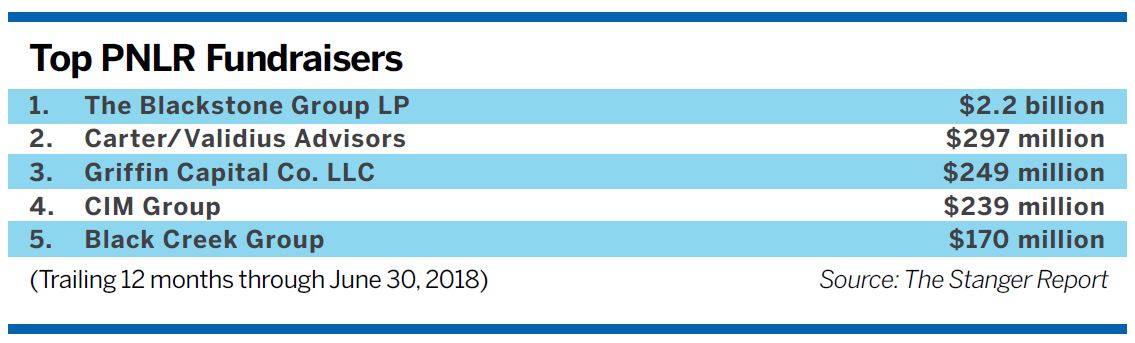

That is largely led by Blackstone coming into the space. Institutional managers who are looking to diversify their sources of capital beyond the institutional investor are very enthusiastic.

And what about the other side?

The legacy sponsors who founded this industry—and have historically been the leading capital raisers through the products in the past—would fall into the other category. Right now, they are having difficulty competing with the institutional managers.

Legacy sponsors are either pulling out of the sector, as evidenced by firms like Behringer Harvard, Wells Real Estate Funds, Inc., and W.P. Carey Inc., or they’re going into a different direction with private placements on a smaller scale.

Looking ahead, what are you anticipating?

It may be possible for some of the smaller sponsors to compete with niche products, but I think for the foreseeable future it’s going to be dominated by those large-scale managers that have the brand recognition and relationships with the wirehouses to get distribution.

What has been the overall impact of these changes on fundraising in the sector?

It’s really been quite a game changer. We are seeing more firms get wirehouse distribution. JLL announced that its non-listed daily NAV REIT, JLL Income Property Trust, is now launched on Morgan Stanley’s global wealth management platform. So, they’re joining Black Creek and Blackstone.

As new products are sponsored, such as by Nuveen, Starwood, and Oaktree, and existing products get these distribution agreements, the fundraising will continue to grow.

Blackstone’s entry into the PNLR market has received a lot of attention. What’s the biggest impact it’s had?

Blackstone’s arrival really removed any of the remaining negative stigma that the product type had. The products have really changed and become much more investor-friendly. For many years, they were perceived as an investment you could get into, but you couldn’t get out of.

Blackstone came in with a better mousetrap, namely the NAV REIT that a couple of firms had already tried to sponsor. Because of Blackstone’s reputation and relationships with the wirehouses, they’ve been able to really get traction and get that product moving forward in a more robust manner. Blackstone coming in in such a successful way has really demonstrated the huge potential for institutional managers to access this capital.

What benefits are retail investors seeing from all of this?

Number one, they’re getting access to managers that historically only institutional investors and pension funds had access to. So, “mom and pop” investors can now invest with the same investment acumen as the largest institutions, which is really exciting.

And the products themselves have improved dramatically in terms of transparency, liquidity, and fees. The problems that the regulators were concerned about largely have been solved by this next generation of product. In fact, the pendulum may start to swing in the opposite direction, where regulations may actually ease up to make it easier to sell these products.

One of the difficulties for sponsors in this channel is that investors must use an old-fashioned approach to actually get into the investment, with signatures on subscription documents and a five-day waiting period after receiving the prospectus before they can actually purchase shares. In most states there is also a concentration limit where an investor’s purchase of the non-listed REIT shares, together with all similar products, cannot exceed 10 percent of the investor’s liquid net worth. Today’s regulatory environment is largely now out of step with the lower risk profile of this next generation of products and some of the regulatory protections may not be necessary for investor protection.

Is there anything else you’re watching at this point?

This is a fairly new product structure, and to date, we’ve been in a robust real estate cycle. Almost 100 percent of investors’ redemption requests have been processed, and redemption plans have largely been kept open. Because redemption plans are the only meaningful source of liquidity for investors in these non-listed vehicles, it will be interesting to see how the boards of directors of these products react in a real estate downturn. Do they close the gates? And how will the distribution partners that are currently marketing the products respond? The products are built for the long term, so if the market fully understands the real estate cycle, then arguably NAV’s will go down, the pricing will go down, and investors will see it as a buying opportunity. But, when the redemption plan is closed, human nature may get in the way of good investment judgment. That will be an interesting chapter yet to come.