Our roundtable of real estate fund managers assess market fundamentals and growth opportunities around the world.

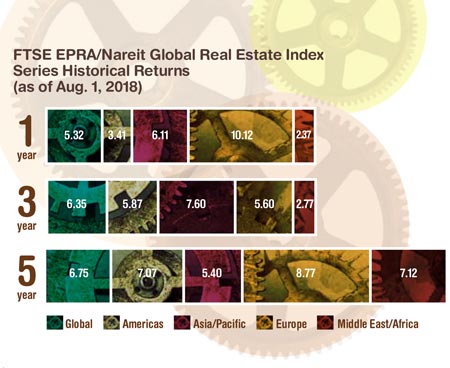

Overall, global real estate market returns in 2018 have been lackluster to date, particularly compared to strong returns seen in 2017. While investors are sounding a note of caution in response to geopolitical risks and other factors, fundamentals appear sound overall, with opportunities present in a slew of different geographic regions and property sectors.

How would you describe global real estate market performance this year? What’s your view on operating fundamentals going forward?

Scott Crowe: Year-to-date we’re basically flat globally. A lot of that reflects the fact that we had a pretty dramatic downdraught in the first quarter of this year, which we’ve recovered from nicely.

If you look at the last year through to June, the trend that pops out is that the U.S. continues to lag global markets, while Europe has been very strong. That’s off the back of the fact that European growth is catching up with the rest of the world. You also have tightening monetary conditions in the U.S. whereas in Europe, for the moment at least, the European Central Bank is still somewhat in easing mode. [The Bank of England raised the interest rate in August for only the second time in a decade.]

Jay Leupp: We’re treading water. We’re at the confluence of some macro forces that are affecting investor sentiment. The U.S. and U.K. are in the process of renegotiating global trade agreements and that alone, across sectors, has its own ramifications. That’s been a big driver of the lack of returns so far this year.

Steve Buller: Fundamentals generally are good. Demand for most forms of global real estate investment seems to be good, and supply, with some exceptions, is still relatively constrained.

However, we don’t have that inflection point or second derivative that things are accelerating at all. Global listed real estate stocks are doing well but they just don’t offer a similar type of growth as investors can find elsewhere in the broader market.

However, we don’t have that inflection point or second derivative that things are accelerating at all. Global listed real estate stocks are doing well but they just don’t offer a similar type of growth as investors can find elsewhere in the broader market.

What are some of the top themes or trends you’re watching right now impacting global real estate markets?

Sherry Rexroad: Trade war tensions are definitely weighing on Asia-Pacific markets. Brexit continues to weigh on the U.K. Trade war, central bank policy, and political tension are the three main themes that we’ve been dealing with and will continue to deal with.

Gillian Tiltman: Improved global growth in assets under management on the direct property side is continuing to put pressure on investors to deploy capital. The problem though is that the prospect of higher long-term interest rates could pose a challenge for pricing.

Crowe: A number of trends are ubiquitous. They include the fact that supply is catching up in many asset classes; obsolescence risk, which is probably more acute this cycle than it’s ever been; and logistics—the need to reconfigure the supply chain—is evident in every country. The rise of alternative investment types is another trend we’re seeing globally.

Leupp: Investors are cautious right now with respect to global real estate. There’s a real hunt for consistent rent and earnings growers both across countries and property sectors.

At this point, I believe that global pricing does not properly reflect the positive fundamentals in institutional real estate that we’re seeing globally. I see opportunities to purchase real estate assets at a significant discount to their underlying private market value really around the globe.

Within Europe, where are you seeing the biggest opportunities right now?

Rexroad: There are political issues within Germany, but from a real estate perspective the fundamentals are very strong. We continue to like the German residential sector and the German and French office market. The Spanish and Irish residential markets are also interesting.

In Europe, storage and student housing are much newer sectors and are still experiencing positive momentum that will be interesting to watch. Logistics, life science, and data centers are all strong sectors in Europe—as well as globally. There are lots of arguments for the scale and globalization of data center companies.

Crowe: U.K. property stocks are going to continue to struggle because the outcomes surrounding Brexit are pretty unclear.

We really like the Nordics, especially the Swedish office market. Stockholm has become this creative economic hub within Europe and that’s creating some good opportunities.

Germany continues to remain attractive in terms of the residential market. Spain has had the most catching up to do after the financial crisis, creating some very interesting opportunities as it relates to rent growth.

Buller: Ireland is a very small listed property market, but the Dublin office market continues to do well, despite new supply. We see tremendous demand not only from the Brexit story and financial services firms moving some of their operations to Dublin, but also multinational technology firms—given the advantageous tax environment and local talent—are viewing it as an English-speaking headquarters for their European operations.

Tiltman: Retailers are increasingly focused on getting their city strategy correct in Europe, which should support rental growth at the prime end of the market, particularly in cities like London and Stockholm.

We still think we can see further rental and capital growth from the German residential sector, given the scope for a potential loosening of government rent controls. We still like Spain, particularly office and industrial, where cyclical rental recovery is accelerating still. We believe that recovery on the peripheral Paris office market continues.

Leupp: Despite Brexit, we see opportunities in London-centric office, residential, and retail, as well as German residential. Public company ownership of German residential is well below 10 percent of the total stock, so I believe there is potential for strong growth and better-than-average rent growth compared with other European real estate sectors. Across Europe, well-located malls and well-located industrial.

Shifting to the Asia-Pacific region, what markets are you watching?

Crowe: In Australia, the office market is undersupplied. The [Sydney development known as] Barangaroo basically put a cloud over the Australian office market for many years coming out of the financial crisis, as it stopped all new supply. Due to a strong residential market you’ve also had a lot of office space converted to residential, so supply is actually shrinking. Now that Barangaroo is finished, the office outlook for the next few years is for very little delivery, which will boost rent growth.

Leupp: Japan will continue to be a very stable institutional real estate market. I also like emerging Asian countries like the Philippines and Indonesia because of their more rapid growth prospects. I like India’s long-term prospects, but in the short term I’m cautious that the public equitization of Indian real estate will potentially have regulatory bumps along the way.

Tiltman: Japan really stands out as an attractive opportunity this year given the convincing signs of deflation finally ending, robust tenant demand, and wide valuation discounts to net asset value.

Corporate management in Asia-Pacific countries is now placing heavier emphasis on corporate governance and shareholder returns—something that we didn’t really see before. Those are factors conducive to improved stock valuation.

Corporate management in Asia-Pacific countries is now placing heavier emphasis on corporate governance and shareholder returns—something that we didn’t really see before. Those are factors conducive to improved stock valuation.

Buller: We like Tokyo office, but more specifically the mid-price point segment. Most of the supply is at the high end, and we’ve actually seen some contraction in the middle of the market.

Are there other regions you’re looking at?

Leupp: In Latin America, I’m favoring Mexico, as it’s the best-positioned economy for future growth. They’ve just had elections, so I’m quite certain that the new president and congress are going to have policies that drive stable economic growth and trade agreements that work for Mexico, as well as their trading partners.

How has the growth of the REIT approach to real estate investment impacted overall investment in real estate markets globally?

Crowe: The growth of global REITs and global REIT investing has certainly made the real estate world more global. I think it has led to great information and analysis in both public and private markets. It has also helped spread best practices globally, especially in the area of management alignment with shareholders, efficient capital allocation, and governance.

Tiltman: The growth in the securitization of real estate around the world has provided investors the opportunity to access the best real estate around the world in a liquid fashion. The public real estate format provides an opportunity for investors to participate in the growing real estate market in a tax efficient way, with access to companies run by top quality management teams that understand how to pass through the income and capital growth provided by their assets to investors.

Leupp: The REIT structure holds a country’s real estate players accountable for enhanced transparency, disclosure, and corporate governance. Once a REIT regime has been established in a country—it paves the way for increased liquidity by introducing the regional REITs there to the $2 trillion global REIT marketplace. A recent great example of this is Mexico where the first REIT was launched less than 5 years ago— liquidity in the country’s commercial real estate market has increased manifold during this period.

Buller: Over time, the growth of REIT investing has impacted real estate markets globally as seen by the introduction of many more “niche” sectors in REITs such as self-storage, data centers, student housing and health care. These “niche” sectors” have tremendously increased their weighting versus the traditional sectors of office, retail and apartments.

Rexroad: The growth of the public equity and debt real estate markets have resulted in a greater transparency for the real estate market overall. I believe this increase in information flow has helped to reduce the amount of overbuilding that occurs in a cycle, thereby muting the recovery period required after a downswing.

With the continued growth of REITs across the world, is there more room for growth in terms of the securitization of global real estate?

Tiltman: We think there’s a lot more securitization of global real estate to come. By investing globally, you have a plethora of sectors and regions and the ability to find value in different places when certain sectors are doing poorly.

In India and China the real estate markets have yet to be securitized, so we believe there is plenty of room for the global market size to grow and be even more interesting going forward. It could be a real game changer for the size of the global REIT market.

Crowe: Definitely. We’ve seen it go the other way in the U.S. with various privatizations, but the trend over time is to see more and more securitization. You’re seeing it especially in the non-traditional asset classes in other countries.

Leupp: I’m extremely bullish on further securitization of real estate. Investors worldwide have become very comfortable with investing in real estate globally, particularly public market investors targeting REITs that want to have immediate exposure in different countries.

Buller: There’s always this accordion of expansion and contraction. Right now, we’re in a period where the number of companies and market cap will be relatively constant but you could see contraction in the U.S. and expansion of some continental European companies.

Rexroad: There’s no question to me that there’s definitely room for growth among the countries currently outside of the developed index, and many of those countries are in the process of implementing a REIT regime.

For the countries within the developed index, what we’ve had recently is a contraction. Part of that is because there’s a lot of private equity chasing a decreased amount of global transactions. That’s an ebb and flow that’s not permanent.

How does your view of the U.S. real estate market impact your allocations in other markets?

Rexroad: We maintain a relatively neutral regional allocation and focus our risk budget on stock selection. That said, our view of U.S. real estate and U.S. economic conditions does affect our outlook for real estate in other countries. The size of the U.S. economy means other countries are impacted by our changes, and countries such as Singapore and Hong Kong are directly impacted by our monetary policy.

Crowe: Our view on the U.S. REIT market is something that feeds into our capital allocation globally. Currently, we think the U.S. is close to fair value, but earlier in the year, following the sell-off, our analysis suggested the U.S. offered relative value when compared to other international markets. As a consequence, we allocated more capital domestically and less abroad.

Leupp: When evaluating international REIT markets, we take into account the macro risk premiums and local bond rates for that region. Subsequently, we compare the price/NAV relationships and cap rate spreads for that particular market, to conclude the relative attractiveness of investing in it versus the U.S. REIT market. For instance, using the same framework today, I would consider U.K. REITs to be more attractively valued and Australian REITs to be less attractively valued relative to U.S. REITs.