Highlights

This research note summarizes a study by Nareit primarily using data from CoStar that estimates the total dollar value of commercial real estate was $20.7 trillion as of 2021:Q2. This study updates and builds upon the methodology for Nareit’s previous estimates of the commercial real estate market.

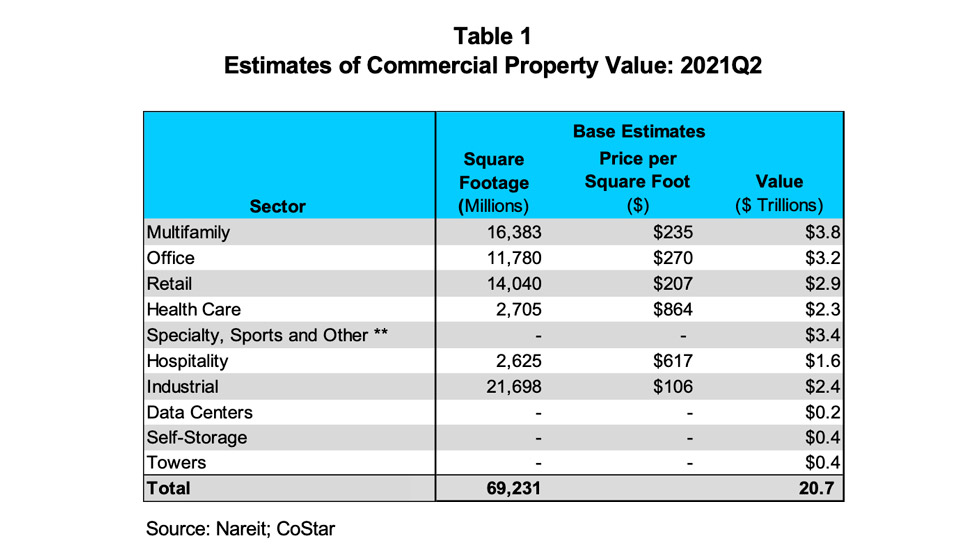

Table 1 summarizes the estimates by property sector. The total estimate is $20.7 trillion. Measurement issues with the underlying data suggest that the actual value of total CRE may differ from this point estimate. An examination of these sources of uncertainty suggests that the actual value is highly likely to fall within a range of $18 - $22 trillion. These estimates are based on a bottom-up approach using the best available data for each property sector.

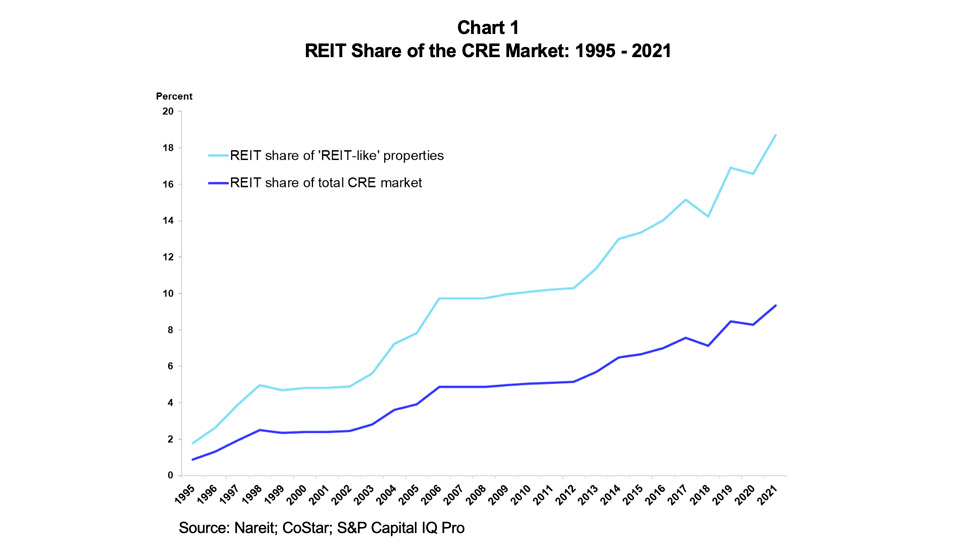

We also estimate total REIT holdings of commercial real estate using data from Capital IQ Pro. For the second quarter of 2021, REITs make up an estimated 9.4% of the total CRE market. REITs tend to focus on institutional-quality properties that are newer and of higher quality than many other commercial properties that are owned by private investors. We estimate the total value of these “REIT-like” properties to be roughly 50% of the total CRE market and that the REIT share of “REIT-like” properties is 18.7% for the second quarter of 2021.

Chart 1 shows a time series of the REIT share of the total CRE market and the REIT share of the REIT-like CRE market.

Methodology

To estimate the size of the commercial real estate market, we use a multi-step approach based on the best available data for each property sector.

- We begin by identifying and estimating the number of units (for multifamily) and total square footage (for other property sectors) by property sector and property quality type for the largest 200 markets in the U.S. This process used CoStar’s data export function covering the Office, Retail, Multifamily, and Industrial property sectors that provided total square footage and units as well as the average price per square foot (for office, retail, and industrial) or per unit (for multifamily).

- The details on square footage and average price by property type (for retail: General Retail, Mall, Neighborhood Center, and Strip Center; for industrial: Flex, Logistics, and Specialized), CoStar quality rating (1-2 Star, 3 Star, 4-5 Star), and groups of metro areas (gateway cities, next largest 48 metro areas, and all other metro areas) allow for further analysis of the geographic distribution of commercial real estate across the country and estimates of institutional-grade commercial real estate versus all other. These estimates in turn are useful for calculating the REIT share of commercial real estate by property sector.

- To estimate values for the Health Care and Hospitality sectors where we do not have disaggregated totals available from CoStar, we use the values from an aggregate analysis of commercial real estate market size conducted by CoStar, updated using aggregate growth rate assumptions.

- To estimate the value of Data Centers and Towers, we estimate the total value of REITs in these property sectors and gross up to cover the entire market using assumptions on the REIT percentage of these sectors (50% for Data Centers and 75% for Towers). Recent Nareit-sponsored research on cell tower REITs highlights their importance in the CRE market. The calculated value for Data Centers is subtracted from the Industrial total, as it is included in the CoStar estimate of total square footage of Industrial properties.

- We estimate the REIT share of the commercial real estate market by using data from S&P Capital IQ Pro on the Real Estate Value of REITs. We add up the total Real Estate Value for the most recent quarter and divide by the total value of the CRE market.

- To establish a time series for REIT share, we use observed data on the total size of the CRE market since 2012. For years before 2012, we assume an 8% growth in total value for each year going back to 1995.. For the years 2007 – 2011, we follow different conventions to account for the effects of the Great Financial Crisis. In 2007, we estimate that the total CRE value declined the same percent as REITs. This percent decline is the same for both components in 2008. In 2009 – 2011, both the total market and the REIT values increase to ¼, ½, and ¾ of the way to the 2012 value, respectively.

- In addition to estimating the REIT share of the total market, we also estimate the REIT share of ‘REIT-like properties.’ REITs do not own many older, lower quality, or smaller properties that are owned by private investors. Therefore, we estimate that half of the total market is “REIT-like” properties and we divided the REIT value by that number to estimate the REIT share of “REIT-like” properties.