Highlights

- The inclusion of REITs in a retirement portfolio boosts returns and reduces risks.

- REITs play a critical role in improving investment returns and reducing risk in target date funds.

- A portfolio including REITS can significantly boost retirement savings.

Key Results

Wilshire Funds Management was commissioned by Nareit to study the role of REITs in Target Date Funds (TDFs). Wilshire found that REITs play a critical role in improving investment returns and reducing risk in these popular investment products.

TDFs are designed to simplify portfolio planning for individuals. It is expected that the majority of new 401(k) and IRA assets will be invested in TDFs over the coming decades and the retirement security of millions of Americans will depend upon their investment performance.

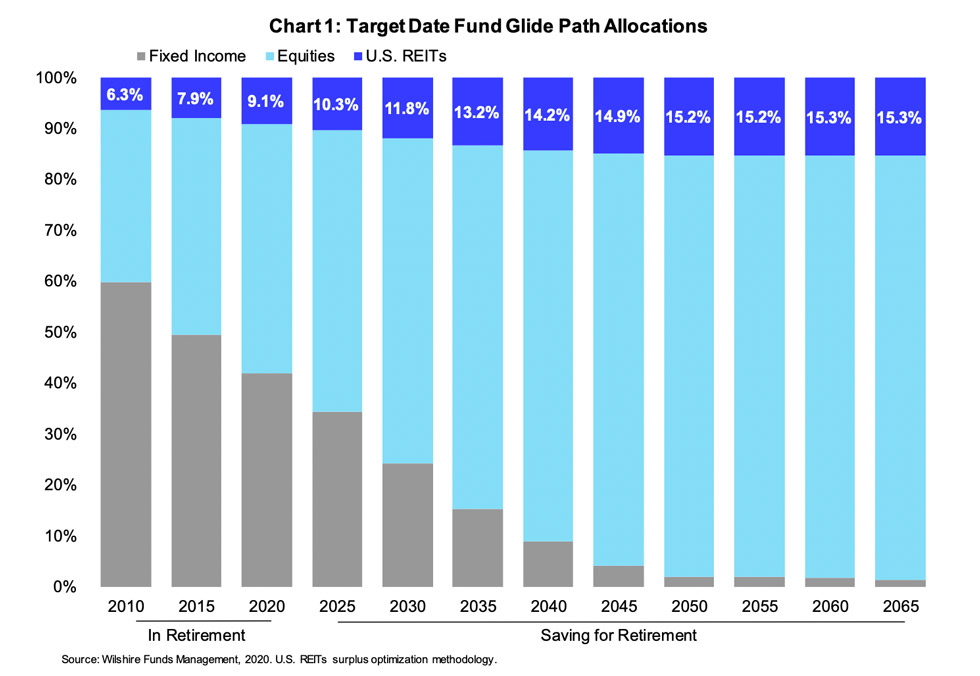

REITs Important Across the Target Date Fund Lifecycle

The figure below summarizes the optimal allocation of U.S. REITs in a retirement portfolio for workers with different retirement horizons.

- REIT allocations range from 15.3% of the portfolio for a young worker with 40 years to retirement to over 10% for an investor near retirement age.

- The REIT allocation declines along with other equities throughout retirement but remains over 6% for an investor nearly 10 years into retirement.

REIT Attributes: High and Stable Income, Long-term Capital Appreciation, Diversification and Inflation Protection

REITs are an important part of retirement portfolios because they provide income, capital appreciation, diversification, and inflation protection.

Portfolio volatility can be reduced by adding assets that have low correlations with the assets currently in the portfolio. The long-term correlations of equity REITs with other major asset classes included in the study range from 0.19 to 0.65, signifying potential diversification benefits from adding REITs to an investment portfolio.

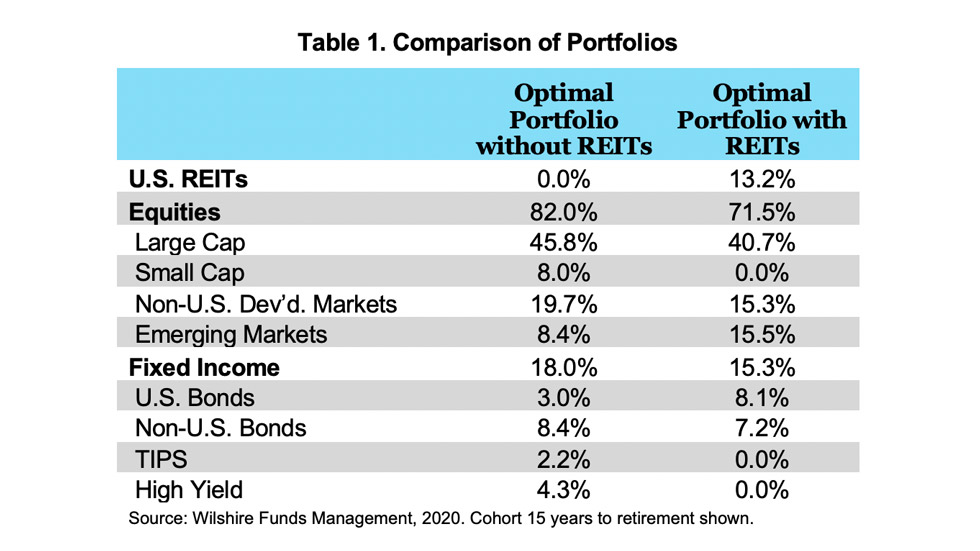

Table 1 compares asset allocations for an optimized portfolio for the 15 years to retirement cohort in the glide path excluding and including REITs in the set of potential investments.

The portfolio constructed with REITs also has significantly lower or zero allocations to U.S. TIPS, U.S. High Yield Bonds and U.S. Small Cap Equities. The fact that REITs take “shelf space” in the optimal allocation from these assets indicates that REITs serve as a more efficient asset class for combining the investment attributes of high and stable income, long-term capital appreciation, and inflation protection.

REITS Improve Retirement Readiness

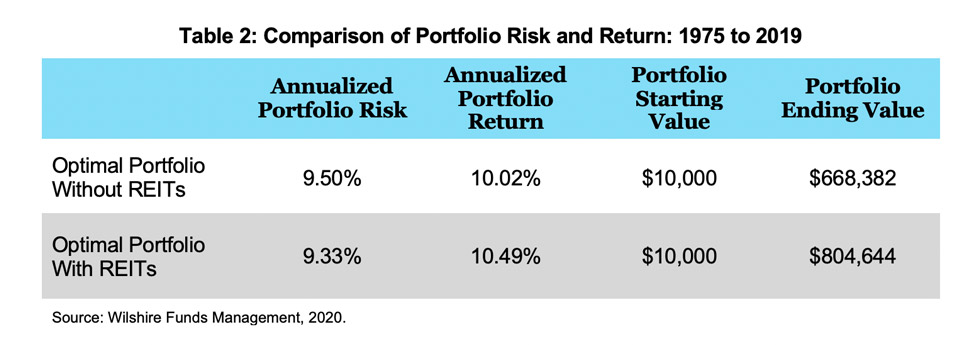

Including REITs in the TDF portfolio increases returns and reduces risk. Table 2 compares risk and return for optimized portfolios in the middle of the glide path excluding and including REITs over the 44-year period 1975 to 2019. A TDF portfolio including REITs has a higher return and lower risk than a portfolio without REITs. The TDF portfolio including REITs returned 10.49% annually with an annualized portfolio risk of 9.33%. This compares to a return of 10.02% and an annualized portfolio risk of 9.50% without REITs. Over the 44-year investment period, the TDF portfolio using Surplus Optimization would have resulted in a portfolio value at the end of 2019 that is 20.4% higher than a portfolio without REITs.

See also: REITs are the Secret Ingredient in BlackRock’s Imitation Pension Fund

Downloads

*The Wilshire study described on this page is an update of a Wilshire study originally done in 2012.