Nareit tracks quarterly investment holdings for the largest actively managed real estate investment funds focusing on REIT investment for insights into expert investor sentiment. In the fourth quarter of 2025, data centers saw a significant rebound with the largest quarterly increase of all the property sectors bumping it up to 134% of its index weight in the funds. Conversely, a large quarterly reduction in gaming left the sector at just 43% of its index weight.

Health care maintained its top spot in the funds at 19% of assets under management, but telecommunications remained the most overweight sector relative to its index weight, invested at 135% of its index weight. Following close behind was data centers at 134%. Specialty also saw quarterly and annual increases in its weight in the funds and flipped to overweight versus the index this quarter. Gaming continued to lose ground in the funds, dropping to just 1.3% of assets, the second smallest allocation after diversified.

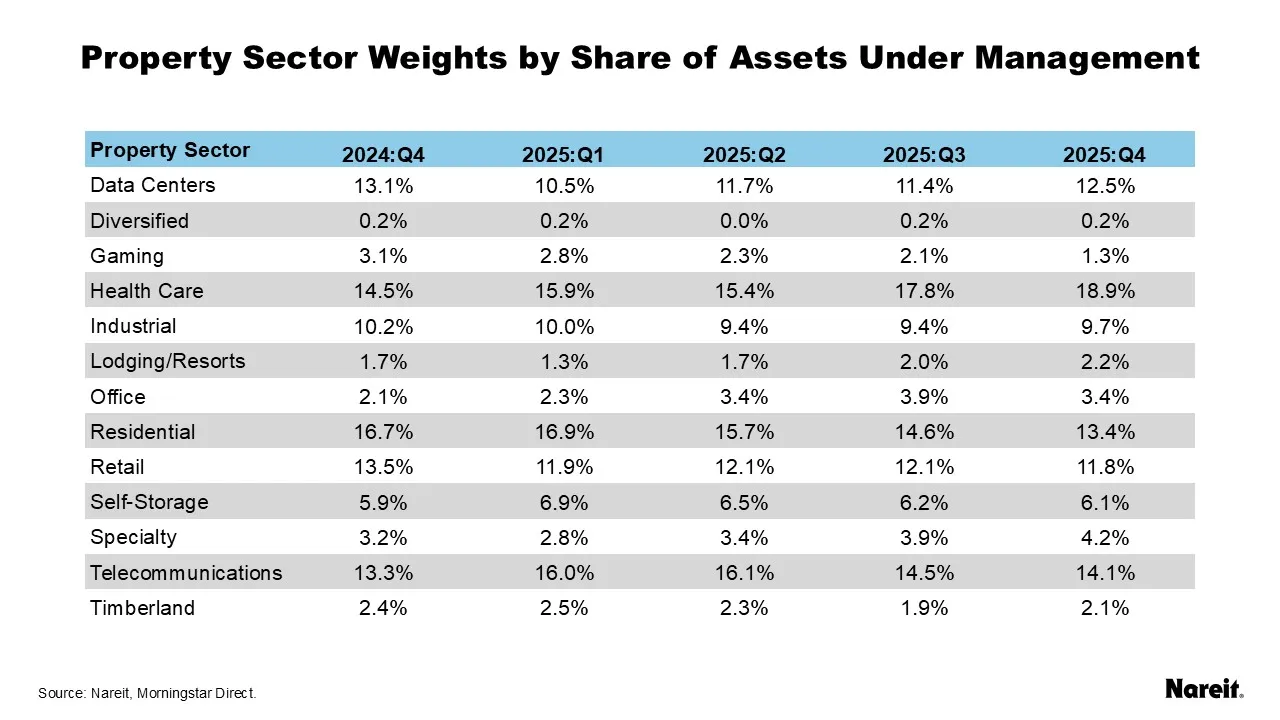

The table above shows the share of each equity REIT property sector by assets under management.

- Health care (19%), telecommunications (14%), and residential (13%) continued to claim the top three spots.

- Data centers edged out retail for the fourth highest allocation at 13% compared to 12% for retail.

- Gaming dropped to the second smallest allocation at 1%, falling behind lodging/resorts and timberland.

- Diversified remained in last place, with slightly more than a 0.01% share.

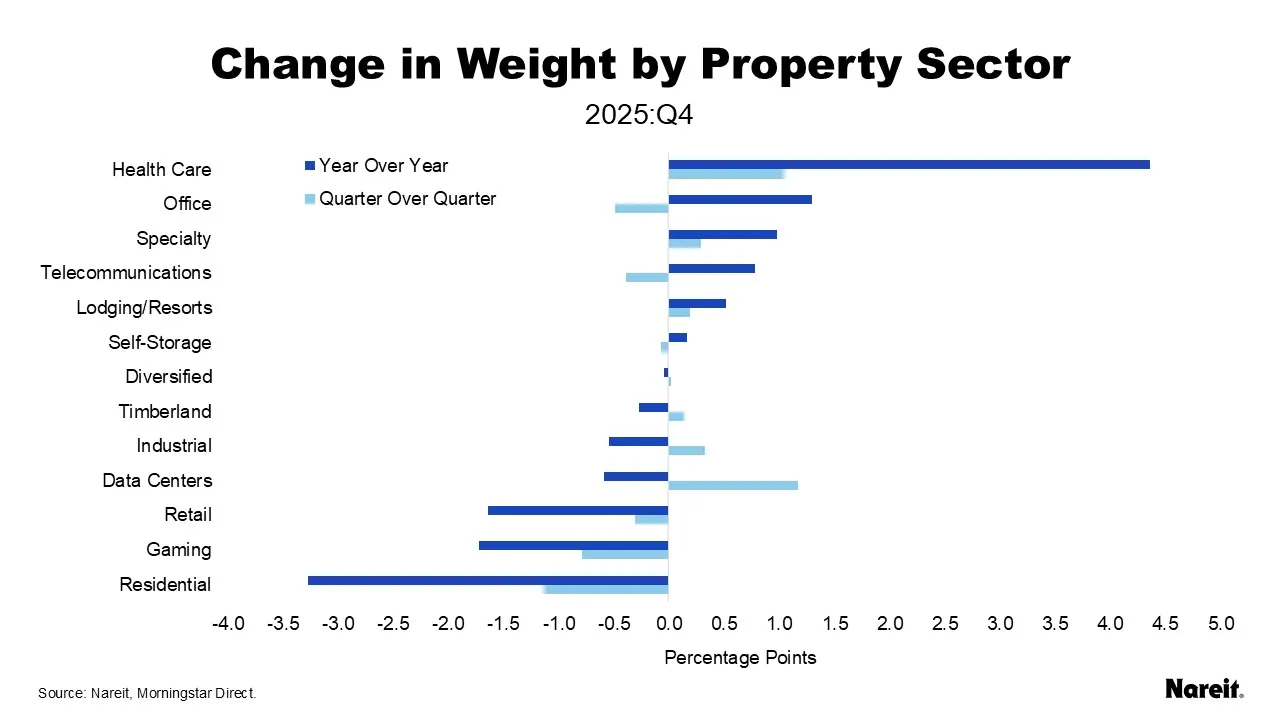

The table and chart above show the change in property sector asset share by quarter and from the previous year.

- Health care had the largest annual gain in weight of 4.4 percentage points. Underlying data show that the strong stock returns in the sector led to the large gain, rather than an increase in shares held by the funds.

- Data centers had the largest quarterly increase at 1.2 percentage points, although was still down slightly for the year.

- Office’s rebound slowed with a quarterly loss of half a percentage point. However, compared to the prior year, the quarter has the second highest increase at 1.3 percentage points.

- Specialty had the third highest annual increase at 1 percentage point.

- Lodging/resorts continued to see quarterly and annual gains, up 0.52 percentage points from the prior year after three quarters of modest gains.

- Timberland, industrial, and data centers were all up for the quarter but down for the year. Timberland and data centers have no steady trend in the past year, showing quarters of gain after quarters of decline. Overall, timberland is down 0.3 percentage points in the funds and data centers are down 0.6 percentage points for the year.

- Industrial’s decline has been steady since the second half of 2023, with 10 straight quarters of decline until the modest increase of 0.3 percentage points this quarter.

- Gaming has seen quarterly declines for seven straight quarters, and was down 0.8 percentage points at the end of 2025. Gaming is down 1.7 percentage points from the prior year.

- Residential had the largest annual and quarterly declines. The sector is down 1.1 percentage points for the quarter and 3.3 percentage points for the year.

The charts and table above compare the weight of the sectors in actively managed funds to the weight of the sectors in the All Equity index.

- Telecommunications has been the highest overweight sector by both percentage points and index share for the entire year, overweight the index 3.7 percentage points in the fourth quarter and 136% of its index share.

- The rebound in data centers put the sector back in second place for overweight its index share. After hovering around 2 percentage points overweight for the past two quarters, data centers are overweight 3.2 percentage points this quarter, 134% of its index weight.

- Specialty jumped to overweight this quarter at 116% of its index share after being underweight for the past year.

- Residential and health care moved closer to parity with their index weights over 2025. Residential started 2025 at 117% its index weight and is down to 106%, and health care started at 113% and is down to 110%.

- Despite its quarterly decline, office stayed overweight at 112% of its index share.

- Retail and industrial were the most underweight in absolute terms, with retail nearly 4 percentage points underweight the index (75% of its index share) and industrial 3 percentage points underweight (76% of its index share).

- Gaming started 2025 at 82% of its index weight and is now down to only 43%, almost 2 percentage points underweight.

Note that three of the 21 funds had not reported fourth quarter data for this analysis.