Early January 2019 has seen a continuation of the stock market turmoil that dominated December 2018: the Russell 3000 dropped by 1.5 percent or more on nine separate days and showed smaller declines on four other days. I have been particularly worried about tech stocks, and they certainly led the market’s turmoil with the S&P Information Technology sector index plummeting on the same nine days by an average of three percentage points per day, with daily declines as bad as 5.03 percent and never less than 1.88 percent.

REITs have generally provided a solid bulwark against stock market declines, with both a low correlation (typically about 60 percent when measured using monthly returns) and a low beta (typically about 0.6, also based on monthly returns) to the broad stock market. Many investors, though, are especially curious about downside beta and upside beta, which measure how a group of investments perform while the broad stock market is losing or gaining. In particular, downside beta and upside beta measure, respectively, how strongly REITs joined in a broad stock market decline or rally: a beta greater than one shows that REITs tended to move in the same direction but even more strongly, whereas a (positive) beta less than one shows that REITs tended to move in the same direction but not as strongly.

The big reason to focus on downside beta and upside beta (collectively called semi-betas) is that ideal investment return attributes will enable you to have it both ways: when the broad market is declining you would like investments that insulate your portfolio (downside beta <1), but when the broad market is increasing you would like investments that magnify the gains (upside beta >1). More generally, you want investments with favorably asymmetric semi-betas—that is, where upside beta is greater than downside beta.

No investment is likely to be “the magic bullet” in terms of semi-beta properties, but it turns out that REITs have performed pretty darn well.

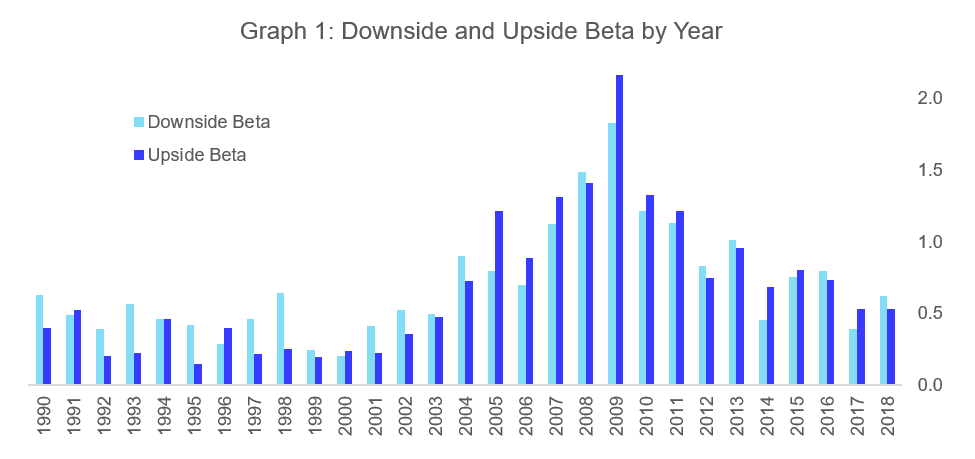

Graph 1 shows downside beta and upside beta for REITs by year. The first thing to notice is that both semi-betas have usually been less than one, indicating that REITs have tended to reduce the volatility of a stock portfolio—that is, they have tended to provide a diversification benefit.

Unfortunately that wasn’t true during the Great Financial Crisis and its aftermath: semi-betas exceeded one from 2007 through 2011. The large increase in REIT beta during the GFC still hasn’t been explained—and it’s worth noting that the exact opposite had happened during the previous stock market crisis, the dot-com bust of 2000-2003, when REIT betas were at or near their lowest-ever values, so it’s definitely not true that betas can be expected to increase during a stock market crisis. Whatever the reason for the 2007-2011 surge in betas, it’s certainly a relief to see that it quickly faded away.

The second thing to notice about Graph 1 is that upside beta has typically been larger than downside beta, especially from 2005 on. That means that, especially more recently with the maturation of the REIT industry, REITs have tended to provide the favorable asymmetry that investors crave: REIT gains have more closely approximated the stock market’s gains when the stock market has been rallying, whereas when the stock market is pulling back REITs have done more to moderate the losses. In fact, that was true even during 2007-2011 (except, marginally, during 2008): even though the betas were greater than one, they were larger on the upside than on the downside.

The favorable asymmetry in REIT semi-betas is reflected in the long-term outperformance of REITs relative to the broad stock market: over the past 40 years (since the inception of the Russell 3000) the total return on REITs has averaged 12.12 percent per year, compared to just 11.48 percent per year for the broad stock market. REIT performance has more closely approximated stock market performance when the stock market was gaining, whereas when the stock market declined, REITs have tended to decline more modestly.

If the difference between 12.12 percent per year and 11.48 percent per year over four decades doesn’t seem impressive, consider this: if you had made an initial investment of $10,000 in a portfolio of stocks replicating the Russell 3000 at the end of 1978, by the end of 2018 your balance would have grown to $773,311—but if you had replicated the FTSE Nareit All Equity REIT index instead, your balance would have grown to $979,952. If you still don’t think a difference in wealth of more than two hundred thousand dollars from an initial investment of just ten thousand dollars is impressive, then you and I are simply on different pages.

Downside beta and upside beta can help investors form a more complete understanding of how REITs interact with other assets and therefore how they contribute to overall portfolio performance. Because REITs give investors exposure to an entirely different market cycle—the real estate cycle, which is very different from (and longer than) the business cycle that drives returns for most non-REIT stocks—REITs provide a diversification benefit that investors can’t replicate without maintaining a substantial allocation to the real estate asset class. And listed equity REITs have proven, in literally every empirical comparison ever conducted, to be a better way of investing in the real estate market cycle than private equity real estate investments .

Technical note: semi-betas are computed by regressing daily total returns for REITs on daily total returns for the broad stock market, restricting each analysis to days when stock market total returns were negative (for downside beta) or positive (for upside beta). For REITs I use the FTSE Nareit All Equity REIT Index, except that before the beginning of 1999 I use a composite of available daily returns from the S&P US REIT Index, the FTSE EPRA/Nareit USA Index, the MSCI US REIT Index, the Wilshire US REIT Index, and the Dow Jones US Select REIT Index. For stocks I use the Russell 3000 Index.

If you have any questions or comments, please drop me a note at bcase@nareit.com.