The new global active manager tracker follows the quarterly investment holdings by the 25 largest actively managed funds (22 reporting as of September 2025) invested globally. The previous commentary gave an overview of the actively managed funds’ investments from the beginning of 2020 to mid-2025 across geographies and property sectors. This analysis builds on the previous work by analyzing property sector investments within the Americas, Asia Pacific, and Europe, Middle East, and Africa (EMEA) regions.

The funds hold investments in property sectors across regions, highlighting the effect of geography on the market for different types of real estate.

- While there is broad sector representation in the Americas and EMEA, Asia Pacific is heavily weighted toward the diversified property sector.

- Residential has the largest share in the Americas and EMEA regions, but a small share in Asia Pacific. Diversified has the largest share in Asia Pacific and the second largest share in EMEA. All three regions have significant shares in retail and industrial.

- Retail, health care, and self-storage increased across all regions from 2020 to mid-2025, while office and industrial declined. Data centers rose in the Americas and Asia Pacific but are not present in EMEA.

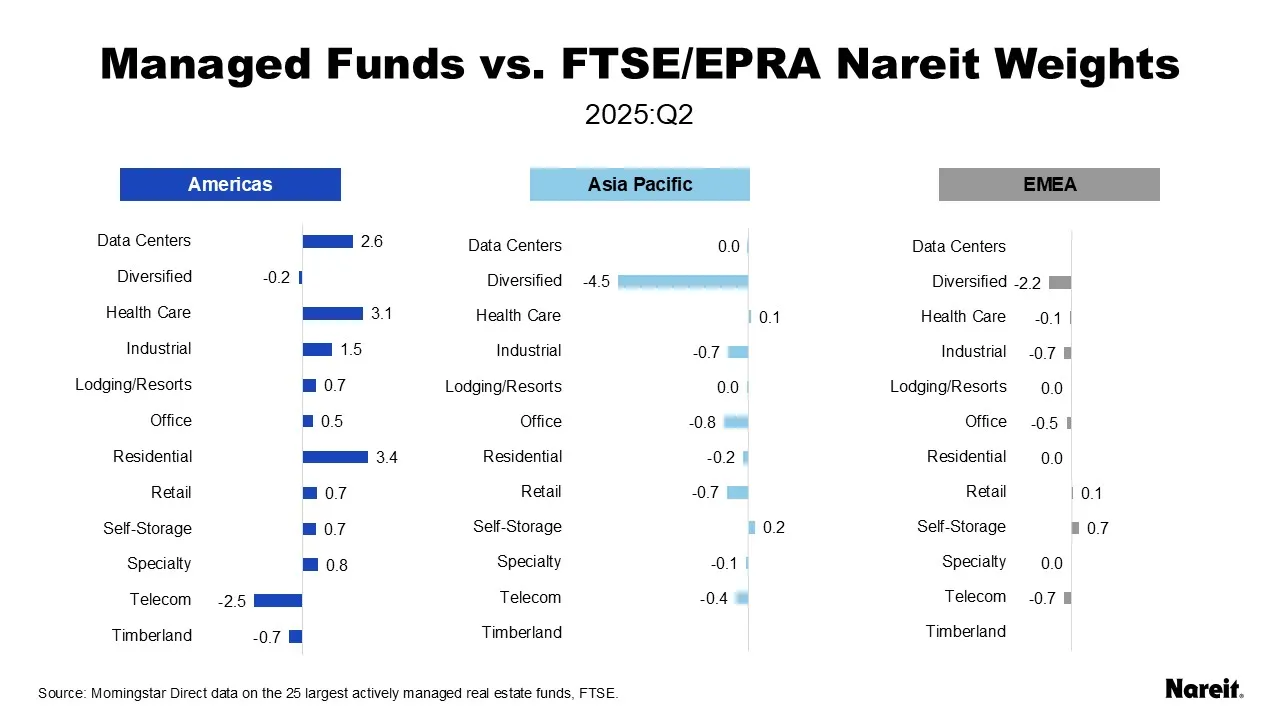

- Self-storage is overweight in all regions compared to the FTSE EPRA Nareit Global Real Estate Extended Index.

- Health care is overweight in Americas and Asia Pacific but underweight in EMEA.

- Diversified, telecommunications, and office are underweight across the regions.

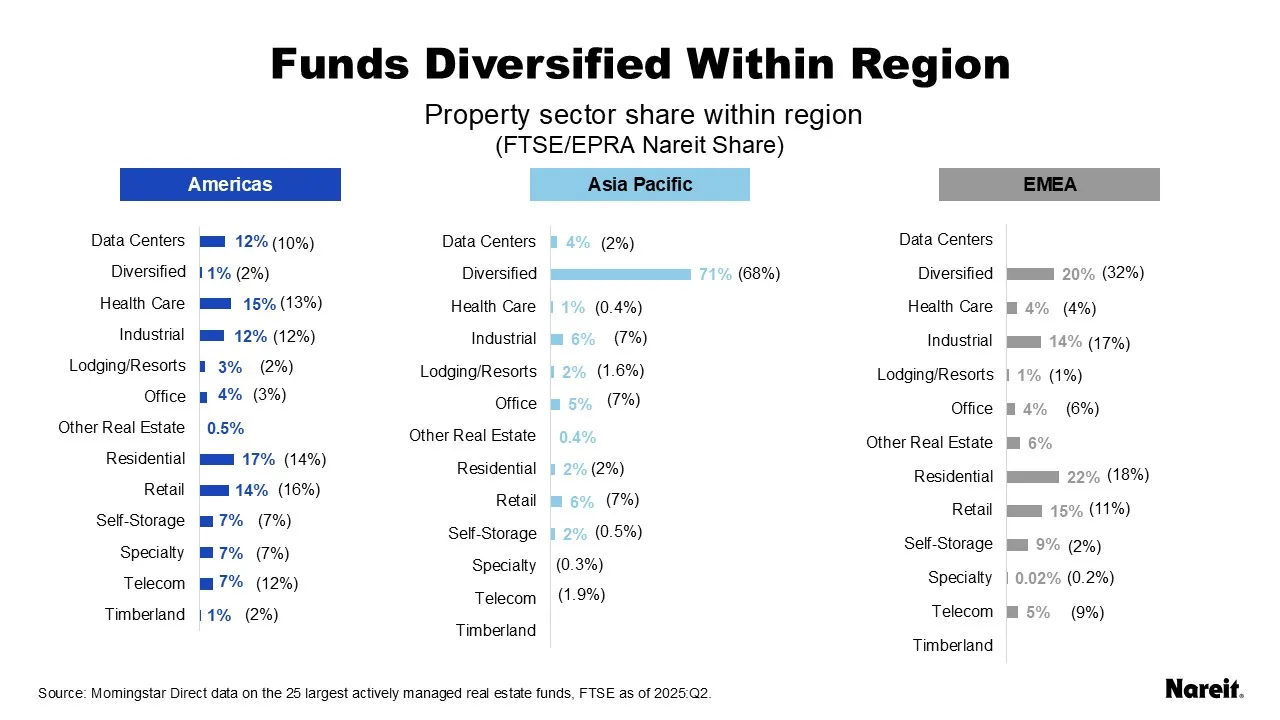

Global funds are diversified within regions, as shown in the chart above. The funds are more broadly dispersed in the Americas and EMEA, while Asia Pacific is largely dominated by diversified REITs. Other real estate includes non-REIT real estate companies whose primary business is not operating real estate. The share in the FTSE EPRA Nareit Global Extended Index is in parentheses for reference.

The funds are invested in 12 REIT sectors in the Americas:

- Residential has the largest allocation at 17% followed by health care at 15%.

- Retail (14%), industrial (12%) and data centers (12%) all have allocations in double digits for the Americas, while diversified and timberland have the lowest allocations.

In Asia Pacific, the funds are invested in nine sectors, missing specialty, telecommunications, and timberland.

- Diversified is the dominant sector in Asia Pacific with a 71% share of assets.

- There are meaningful allocations to retail (6%), industrial (6%), office (5%), and data centers (4%) in the region.

Investment in EMEA covers 10 sectors, missing data centers and timberland.

- Similar to the Americas, residential has the largest allocation in the region at 22%.

- Similar to Asia Pacific, diversified has the second largest allocation at 20%, with double digit allocations to retail (15%) and industrial (14%).

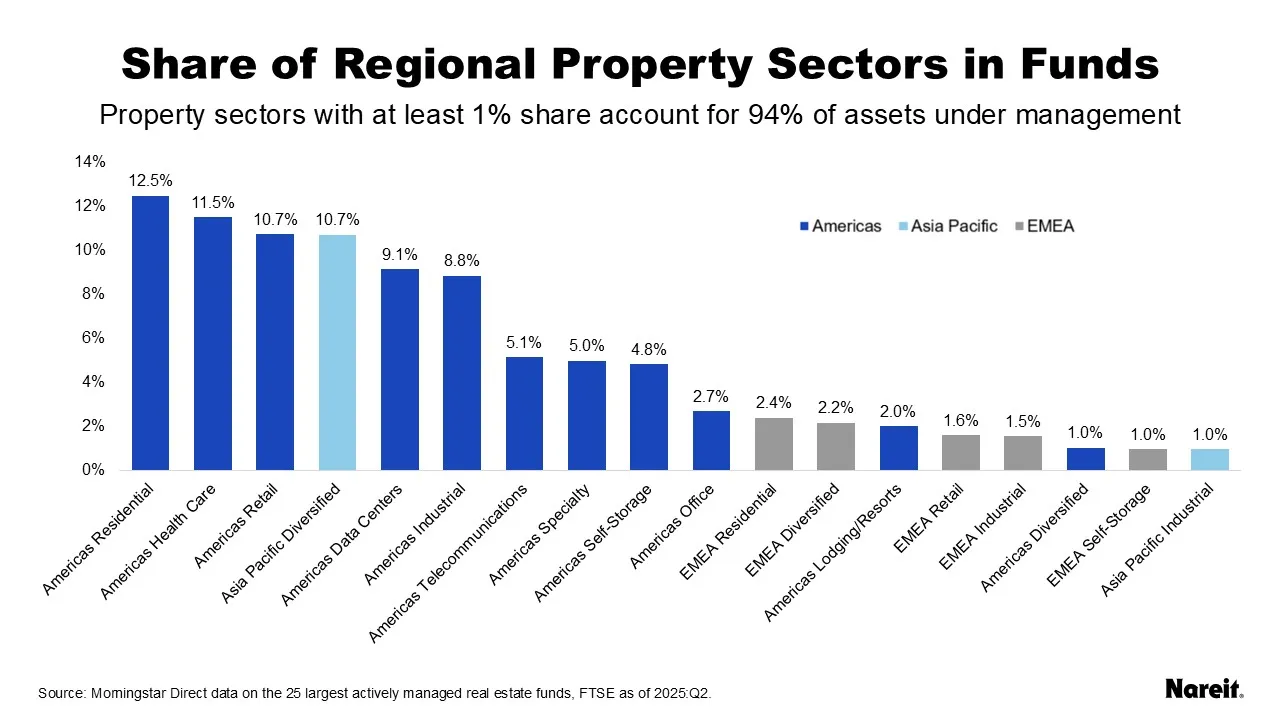

Across all three regions, the funds’ highest allocations are generally in the Americas. The chart above shows the share of assets under management for each regional sector, truncated at shares of at least 1%. The bars are color coded by region. The top two sectors are residential (12.5%) and health care (11.5%) in the Americas, but diversified in Asia Pacific is tied with retail in the Americas for the third slot (10.7%). The highest allocation to any sector in EMEA is 2.4% for residential.

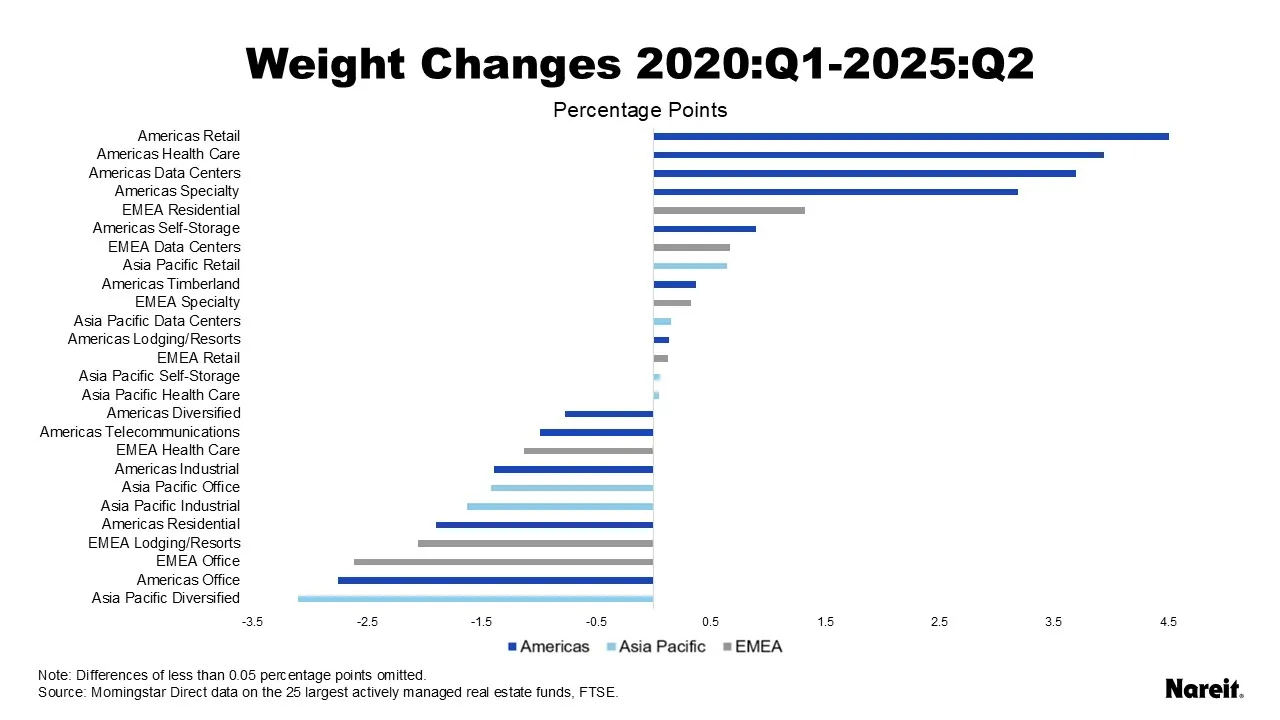

The chart above shows the changes in allocation by sector and region from the beginning of 2020 to mid-year 2025 by the percentage point difference in weight between the two time periods.

- Americas retail had the largest increase in weight at 4.5 percentage points. EMEA retail and Asia Pacific retail also increased by 1.3 and 0.6 percentage points respectively.

- Americas health care, data centers, and self-storage increased shares by over three percentage points. Regional shares in all three sectors also increased for Asia Pacific and EMEA except for data centers, which are not present in EMEA.

- EMEA residential had the largest increase of any sector in EMEA, up 1.3 percentage points.

- Asia Pacific diversified had the largest decrease in weight for the period, down 3.1 percentage points. Americas diversified was also down, but EMEA diversified was up 0.7 percentage points.

- Americas and EMEA office have the largest decrease for their respective regions. Americas office was down 2.8 percentage points and EMEA office was down 2.6 percentage points.

- EMEA lodging/resorts are also down by more than 2 percentage points.

- All three regional shares of industrial were down by more than 1 percentage point.

- Regional shares in residential are down strongly in EMEA by 2.6 percentage points and the Americas by 1.9 percentage points, but only down 0.3 percentage points in Asia Pacific.

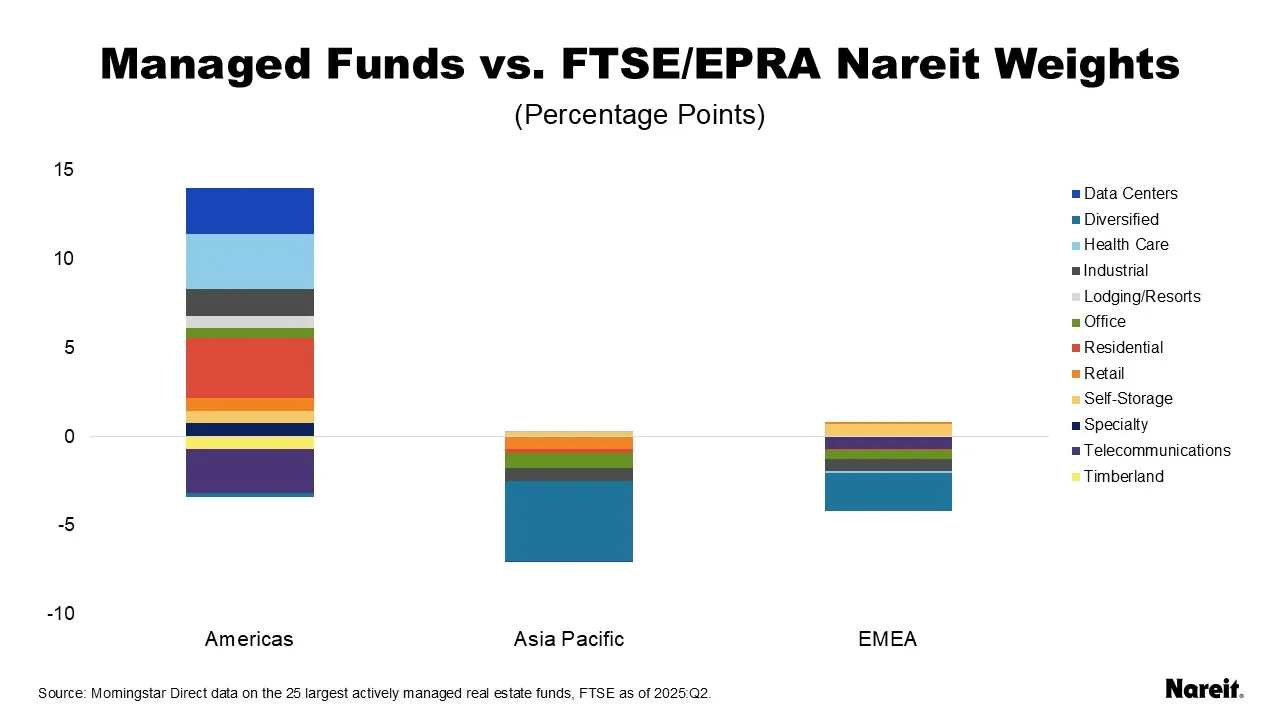

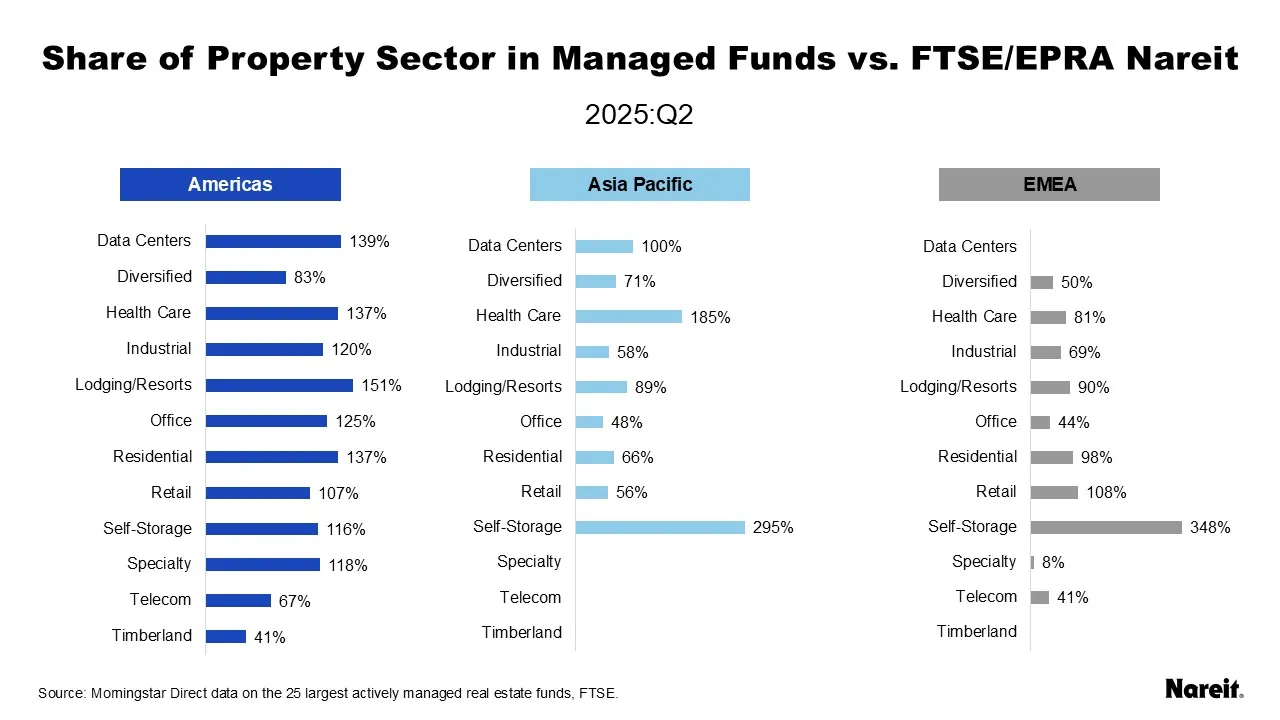

Active managers’ allocations differ from the market in key ways. The charts above show the difference in weights of each sector across the three geographic regions and their relative shares in the FTSE/EPRA Nareit Global Extended Index. The funds are overweight in the Americas at 74% of the geographic share compared to 64% for the index. Given the strong regional focus in the Americas, most sectors in the region are overweight except for diversified, telecommunications, and timberland.

- Self-storage is the only sector overweight for all three regional allocations, albeit with weights under 1% in all three regions. While self-storage is mostly on par in the Americas, active managers are strongly overweight in Asia Pacific at almost triple its small weight in the index, and by almost 350% in EMEA.

- Asia Pacific health care is the most overweight sector behind all three regional self-storage sectors at 185% of its index share, Americas health care is also overweight at 137% its index share, but EMEA health care is slightly underweight at 81%.

- Americas lodging/resorts is strongly overweight at 151%, while Asia Pacific and EMEA lodging/resorts are underweight at 89% and 90% respectively.

- Americas data centers, residential, office, and industrial are all overweight by more than 120% of their index shares.

- Americas timberland and EMEA telecommunications are the most underweight sectors at only 41% of their index shares.

- Diversified is underweight in all three of its regional shares, 83% for the Americas, 71% for Asia Pacific, and 50% for EMEA.

- Asia Pacific and EMEA office are both underweight at 48% and 44% respectively compared to the overweight in Americas office.

Active managers of global real estate funds make strategic use of both geography and property sectors in investing over time. Active managers favor the residential sector in the Americas and EMEA, and the diversified sector in Asia Pacific. Sector trends from 2021 to mid-2025 show a pivot toward retail and health care, particularly in Asia Pacific, and self-storage in EMEA and the Americas.

Active managers diverge significantly from index benchmarks, favoring lodging/resorts and self-storage across all three regions, and data centers in the Americas and EMEA, while underweighting telecommunications and office across all regions. Shifts in active managers’ allocations highlight regional trends in commercial real estate.