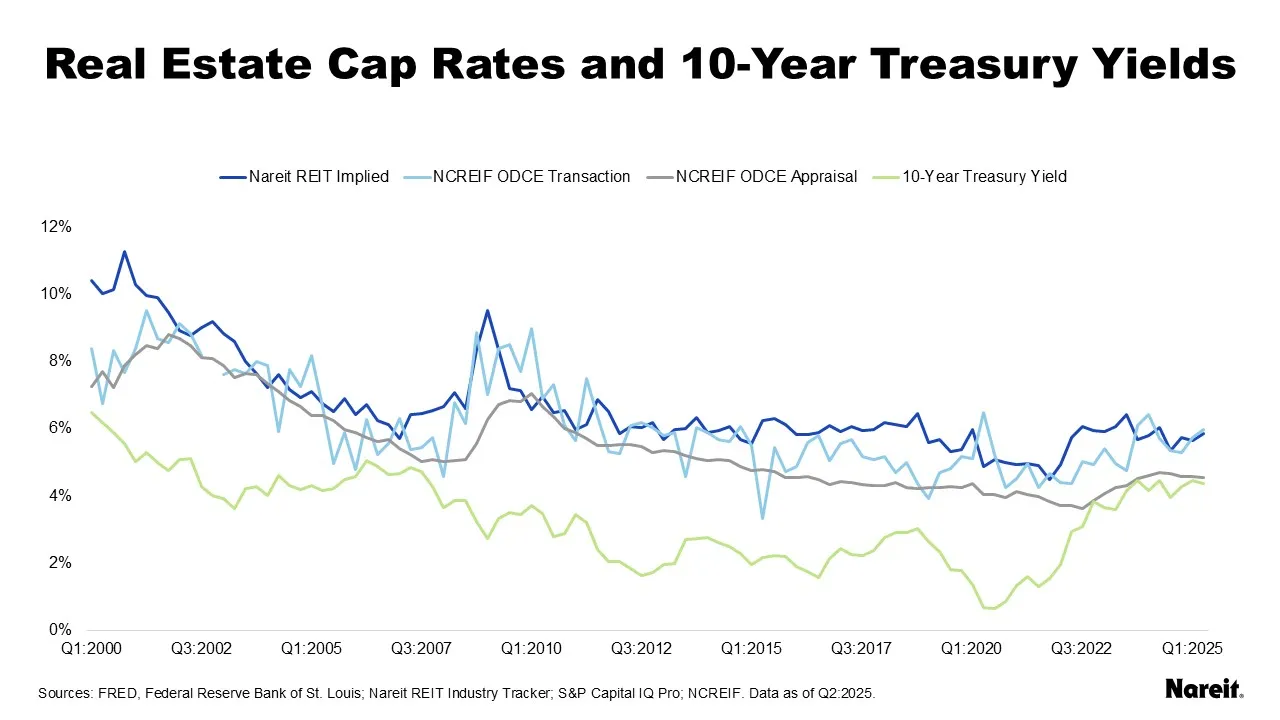

A recent Nareit commentary highlighted the stubbornly slow-to-close and wide public-private real estate cap rate spread. While the market-driven REIT implied and private real estate transaction cap rates have essentially been in sync with one another, private appraisal cap rates seem to remain disconnected from reality. Maintaining only a slight premium to the 10-year Treasury yield, private appraisal cap rates have clearly struggled to embrace current market conditions.

A review of data since 2000 revealed that cap rates driven by market forces, i.e., REIT implied and private transaction cap rates, have historically tended to be in alignment with one another. In addition, outside the current valuation divergence, it was uncommon, or even rare, for private appraisal cap rates to maintain only modest positive spreads over 10-year Treasury yields. The recent inability of appraisers and portfolio managers to mark their real estate assets to market has resulted in a lengthy divergence in public and private valuations and contributed to the slow pace of commercial real estate transactions.

The chart above displays public (REIT implied) and private (transaction and appraisal) real estate cap rates, as well as average U.S. 10-year Treasury yields, from the first quarter of 2000 to the second quarter of 2025. REIT implied cap rate data are from Nareit’s quarterly REIT Industry Tracker. The National Council of Real Estate Investment Fiduciaries (NCREIF) transaction and appraisal cap rates solely focused on properties from open end diversified core equity (ODCE) funds.

Historically, the market-driven REIT implied and NCREIF ODCE transaction cap rates have tended to be in sync with one another. Since 2000, the average and median spreads between the REIT implied and private transaction cap rates have been 55 and 45 basis points, respectively. Since the second quarter of 2024, the gap has averaged a mere 11 basis points.

Over the last five quarters, the NCREIF ODCE appraisal cap rate and 10-year Treasury yield averaged 4.62% and 4.30%, respectively, a spread of 32 basis points. Outside the current property valuation divergence, the private appraisal cap rate spread over the 10-year Treasury yield was less than 100 basis points only seven times; it was less than 50 basis points just two times.

The current relationship between the private real estate appraisal cap rate and the 10-year Treasury yield is untenable, but it persists due to private real estate appraisers’ and portfolio managers’ inaction. Failure to properly value assets impedes the market’s price discovery process, limits transaction market liquidity, and obliges investors to pay artificially high investment management fees. It also increases the appeal of U.S. public equity REITs, as they offer investors access to high-quality, well-located properties at fair market prices.