A recent Nareit commentary explored average annual net total returns for REITs and total private real estate, as well as private real estate investment styles, using realized pension fund performance from CEM Benchmarking. The analysis found that REITs outperformed all private real estate investment styles except internally managed direct funds. It also showed that private value-add/opportunistic real estate funds outpaced core investing by less than 1%; a less than satisfying spread that is not commensurate with initial investment expectations.

Using CEM data, the table above displays private value-add/opportunistic real estate performance relative to private core real estate investments on a net of fee total return basis. Time period starting and ending years range from 1998 to 2007 and 2014 to 2023, respectively, resulting in a grid of 100 time periods. The minimum and maximum average annual net total return spreads are highlighted in bold. Periods where private value-add/opportunistic real estate outperformed by:

- More than 1.75% are shaded dark green,

- More than 1.50%, but less than or equal to 1.75% are shaded medium green,

- More than 1.00%, but less than or equal to 1.50% are shaded light green,

- More than 0.50%, but less than or equal to 1.00% are shaded light blue,

- More than 0.25%, but less than or equal to 0.50% are shaded medium blue, and

- More than 0.00%, but less than or equal to 0.25% are shaded dark blue.

As expected, private value-add/opportunistic real estate outperformed private core funds in all the examined time periods. The minimum average annual net total return spread was 0.12%; the maximum was 2.02%. Over the data’s full history (1998 – 2023), the average annual net total return for the value-add/opportunistic style was just 0.92% more than the core average. A broader review of the table reveals that value-add/opportunistic investments have delivered modest net outperformance for higher active risk and leverage levels.

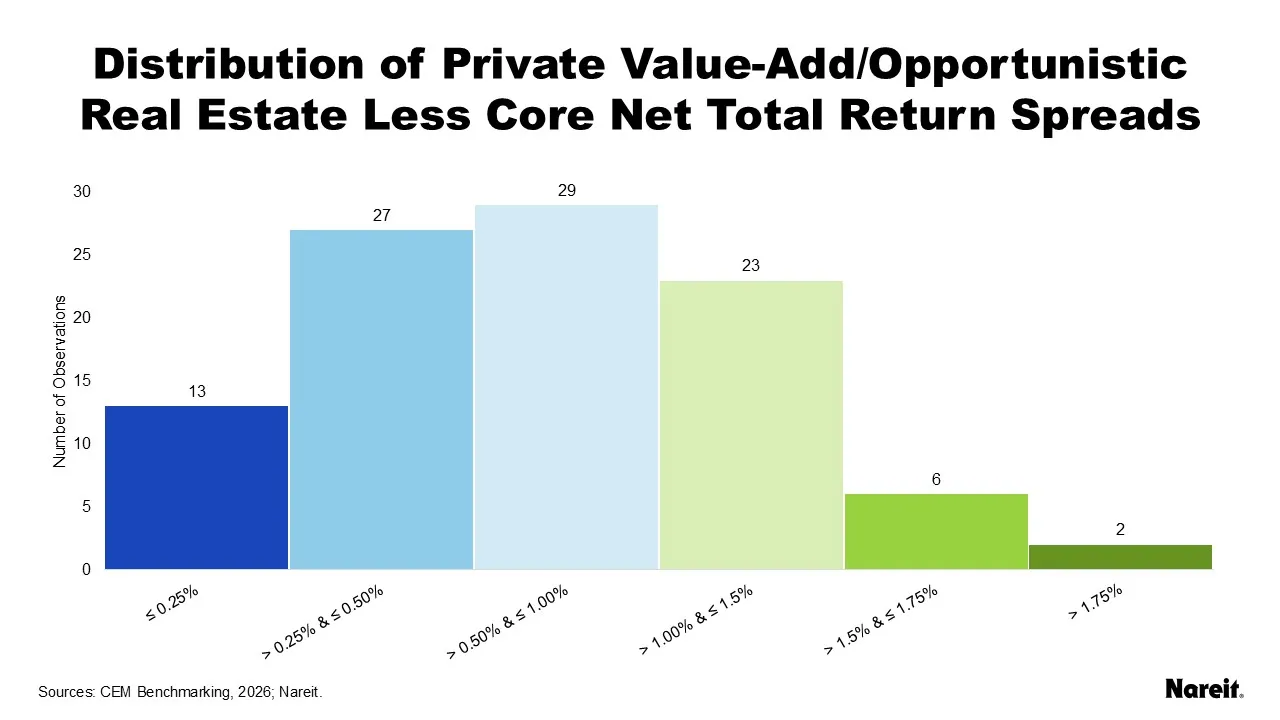

The bar chart above presents a distribution of private value-add/opportunistic real estate’s net outperformance relative to private core investments for the 100 examined time periods. Value-add/opportunistic outpaced core by less than or equal to 1.00% in 69 of the 100 examined periods (blue hues) and by less than or equal to 0.25% in 13 periods (dark blue shading). Value-add/opportunistic bested core by more than 1.00% in 31 periods (green hues) and by more than 1.75% in only 2 periods (dark green shading).

These results are disappointing, but not unusual. An article in the Fall 2023 PREA Quarterly, “Academics Question the Value of Private Real Estate Funds: What’s an Investor to Do?”, summarized academic research which consistently found closed-end private real estate fund underperformance.

Given the modest magnitudes of outperformance relative to core property investing, institutional investors should place greater scrutiny on the realized net performance of their private value-add/opportunistic real estate investment strategies. They should also further explore how REITs can play greater tactical and strategic roles in their investment portfolios. REITs can help investors by offering relative value opportunities, complementing existing portfolio allocations, providing broader diversification benefits, and improving overall portfolio performance.