REITs have been active property buyers and sellers throughout real estate cycles. History shows that REIT transaction activity has declined markedly across consistent periods of divergence and higher capital costs, and accelerated when public-private valuations were aligned and costs were lower. Data from Nareit’s quarterly REIT Industry Tracker show a recent uptick in REIT transaction activity. REITs are expected to pursue even more property transactions as public and private real estate values become more in sync.

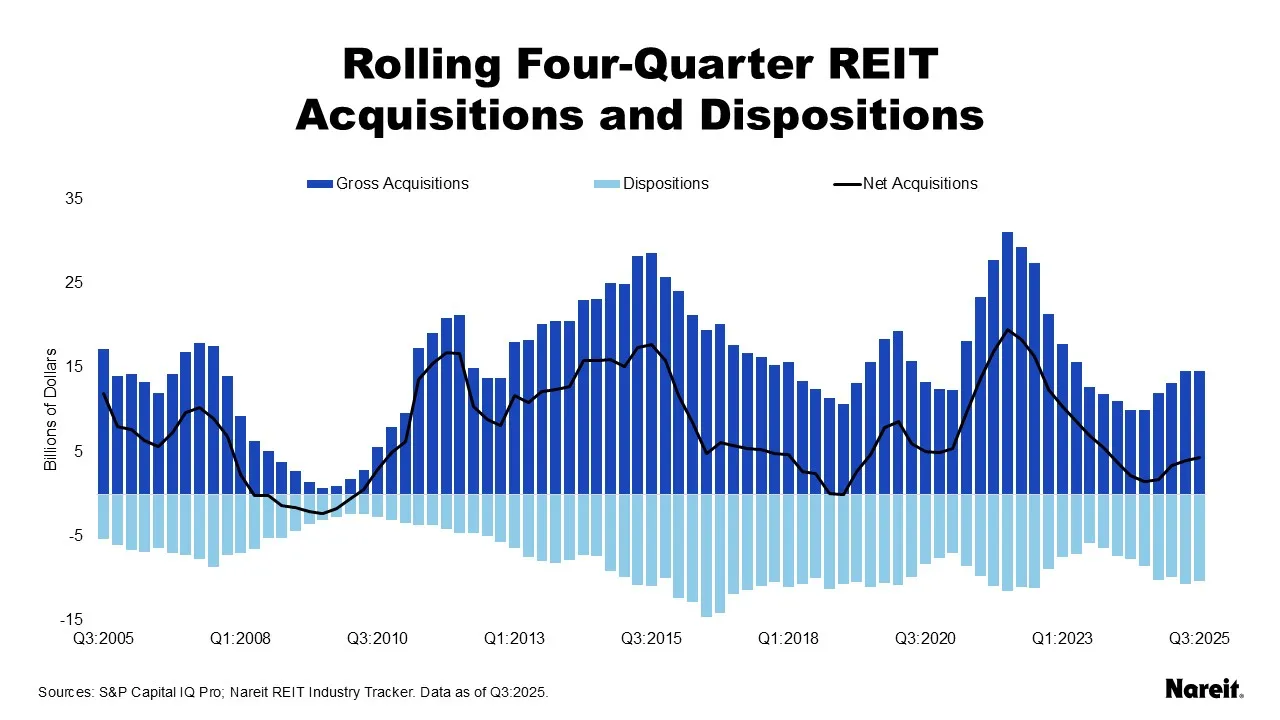

The chart above presents REIT rolling four-quarter gross acquisitions (positive values, dark blue bars), dispositions (negative values, light blue bars), and net acquisitions (positive or negative values, black line) for the last 20 years. These aggregate measures include property purchases and/or sales from all 13 REIT property sectors with the exception of timberland, which does not report its transaction activities. The net acquisitions metric was calculated by subtracting dispositions from gross acquisitions.

REITs have generally been net buyers of real estate. The global financial crisis (GFC) marked the last prolonged period when REITs were net sellers. REITs have also consistently pruned their property portfolios throughout real estate cycles. Despite the lingering public-private real estate valuation divergence, REIT net acquisitions have trended upward over the past year.

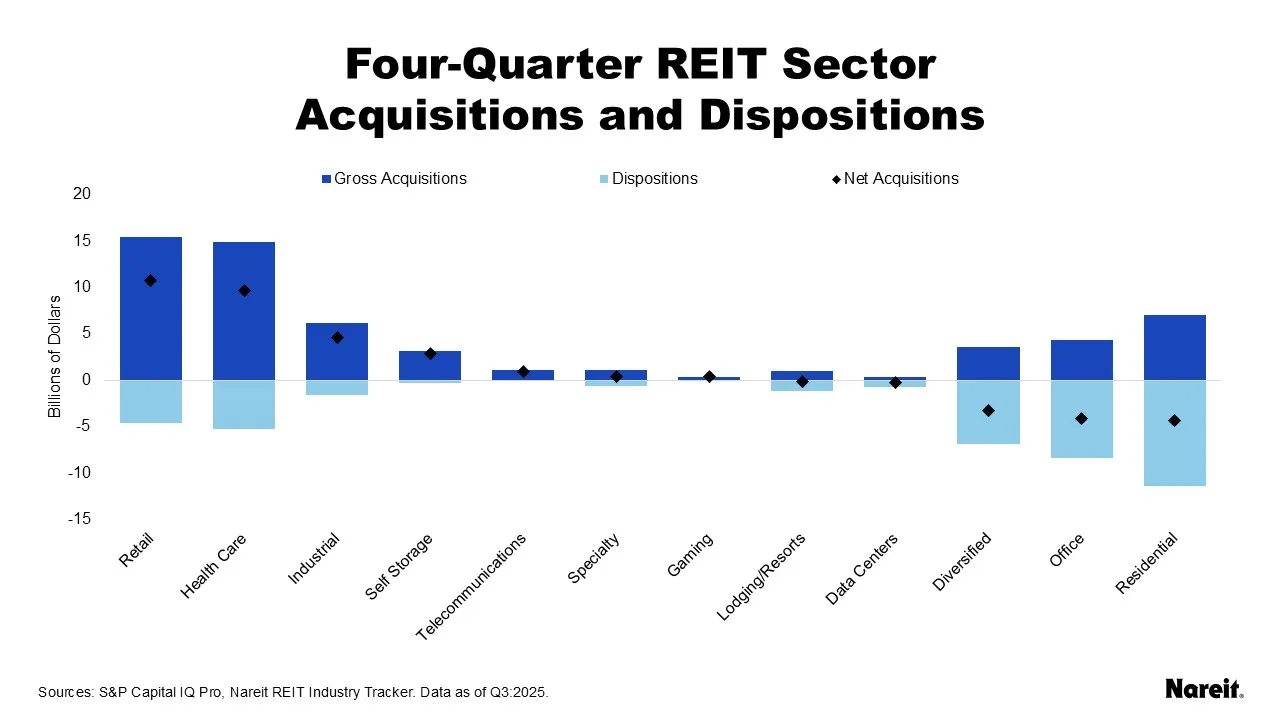

Highlighting significantly different transaction experiences, the chart above presents REIT four-quarter gross acquisitions, dispositions, and net acquisitions for all equity REIT sectors except timberland as of the third quarter of 2025.

Retail, health care, industrial, and self-storage were the largest net buyers. For the retail sub-sectors, regional malls reported the fewest transactions. Free standing stores and shopping centers accounted for 52.5% and 43.3% of total retail gross acquisitions, respectively. Shopping centers comprised 61.3% of total sector dispositions; free standing stores were 22.5%.

Residential, office, and diversified were the biggest net sellers over the past year. For the residential sub-sectors, apartments and single family homes comprised nearly all residential gross acquisitions at 71.9% and 27.3% of the total, respectively. Manufactured homes accounted for 50.0% of residential dispositions; apartments were 38.5%.

As public-private real estate valuations continue to converge, property transaction activity is anticipated to accelerate. When this happens, REITs are ready for action. With disciplined balance sheets and access to cost-advantaged capital, REITs are expected to be well-positioned to enter a growth cycle and pursue accretive growth opportunities.