CEM Benchmarking’s 2026 study, sponsored by Nareit, provides a comprehensive look at realized investment performance across asset classes, including real estate and its investment styles, over a 26-year period (1998–2023) using a dataset covering public and private sector pensions with nearly $4 trillion in combined assets under management. CEM’s analysis of real estate investment styles found that, on average, internally managed direct funds and REITs have led performance.

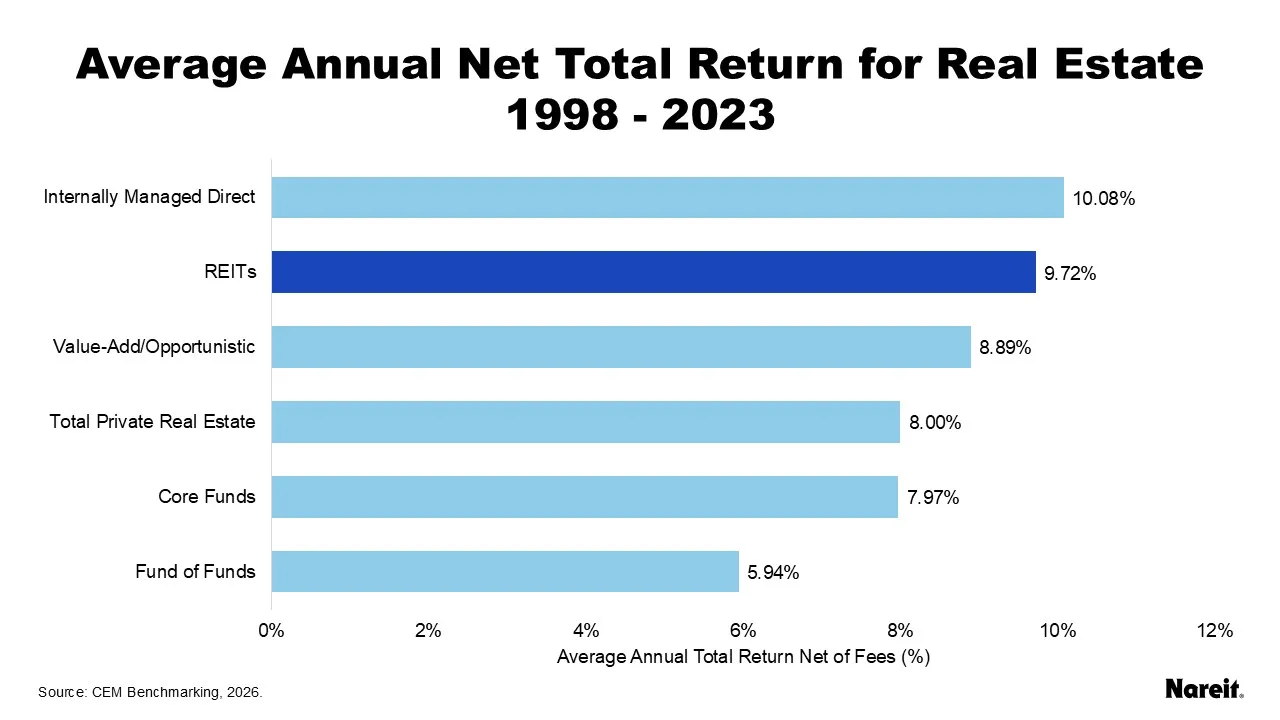

Using as reported performance data from CEM, the chart above displays average annual net total returns from 1998 to 2023 for REITs and total private real estate, as well as several different private real estate investment styles including internally managed direct, value-add/opportunistic, core, and fund of funds. Note that the CEM study provides as reported and adjusted total returns; both are very similar. Adjusted total returns include adjustments for reporting lags associated with illiquid asset classes (private real estate and private equity).

From 1998 to 2023, on average, REITs and total private real estate posted average annual net total returns of 9.72% and 8.00%, respectively, resulting in REITs outperforming private real estate by 1.72%. Drilling down beyond the broad private real estate asset class reveals that performance across real estate investment styles differed markedly.

Slightly edging out REITs, real estate internally managed by pension funds posted the highest average annual net total return; it was 10.08%. Given its significant human capital requirements, this strategy is typically only implemented by larger pension funds. With its double layer of fees, the fund of funds investment style, which is often used by smaller pension funds, had the lowest average annual net total return at 5.94%. The average annual net total returns for private value-add/opportunistic and core real estate funds were 8.89% and 7.97%, respectively. The performance of the higher risk and return strategy outpaced core investing by less than 1%; a disappointing spread that is not commensurate with initial marketing investment expectations.

Over the data’s full history, REITs outperformed all private real estate investment styles except internally managed direct funds on an annual net total return basis. Specifically, on average,

- REITs outperformed private fund of funds by 3.78%,

- REITs outperformed private core funds by 1.75%, and

- REITs outperformed private value-add/opportunistic real estate funds by 0.83%.

Given these magnitudes of outperformance, institutional investors should further explore how REITs can play greater tactical and strategic roles in their investment portfolios. REITs can help investors by offering relative value opportunities, complementing existing portfolio allocations, providing broader diversification benefits, and improving overall portfolio performance.