A recent research note by Hodes Weill & Associates (HW) called REITs versus Private Real Estate Funds: Partners, Not Rivals addressed the merits of public and private real estate in an institutional investor’s portfolio. The sentiment suggested by the article’s title is correct. Yes, both private real estate and REITs can, and do, play important roles and are often integral parts of well-constructed institutional investor portfolios. However, the study’s primary conclusion deserves more elaboration:

“…History demonstrates that a well-selected portfolio of value-add funds can generate sufficient alpha to justify the illiquidity and higher risk—and in combination with REITs can yield a resilient and flexible portfolio...”

The best performing private value-added real estate funds have posted strong returns and blending REITs and private strategies in a real estate portfolio has many advantages. But, the conclusion also raises the question of how REITs and private real estate strategies have performed across the distribution of returns. Obviously, while easy to do, the comparisons of top-performing private value-add real estate funds to a passive REIT index (exchange-traded fund) are not apples-to-apples comparisons.

Data from CEM Benchmarking (CEM) can help investors better understand the alpha generation abilities and performance across the distributions of net total returns for REITs and private real estate. It indicates that REITs have historically delivered superior net total return performance compared to private real estate across return distributions.

Specifically, CEM data have shown that:

- Both REITs and private real estate offered the potential to generate alpha before investment management fees, but only REITs continued to deliver alpha after fees.

- REITs, on average, have outperformed private real estate and this outperformance was persistent across the return distributions, i.e., 10th, 25th, 50th, 75th, and 90th

CEM is a global investment and pension administration benchmarking firm with access to a rich proprietary dataset on pension investment performance covering a 26-year period (1998–2023) for public and private sector pensions with nearly $4 trillion in combined assets under management. An important and distinguishing feature of this data is that it provides the actual realized performance, net of investment costs, of the assets chosen by plan managers.

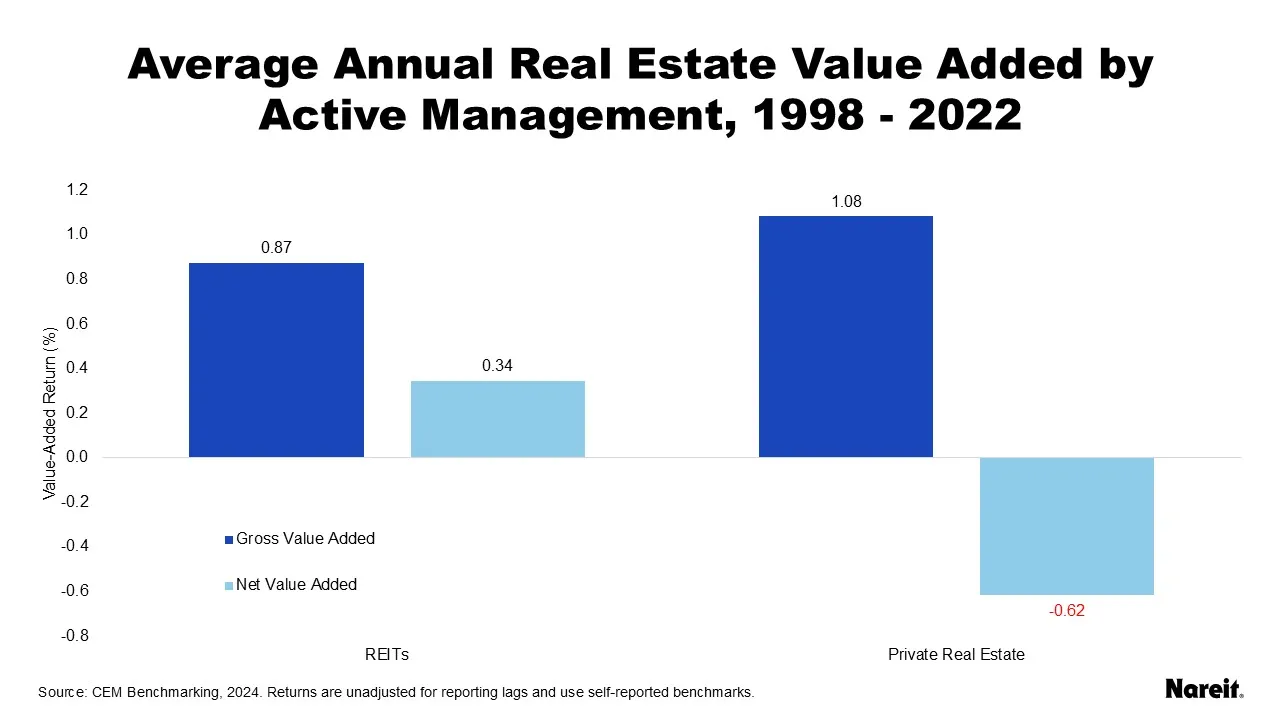

Using CEM data, the chart above displays the average annual gross and net value-added returns of REIT and private real estate actively managed investments relative to their respective benchmarks from 1998 to 2022. Note that benchmarks are self-selected and reported by investors themselves, which may result in an upward bias in value added measures.

The good news is that real estate as an asset class offered the potential to add value, i.e., alpha, before investment management fees for both REITs and private real estate. Gross value-added returns for REITs and private real estate were 0.87% and 1.08%, respectively. The bad news is that institutional private real estate investors, on average, underperformed their benchmarks after fees with a net value-added return of -0.62%. In contrast, the average REIT portfolio still delivered alpha with 0.34% of net value-added return.

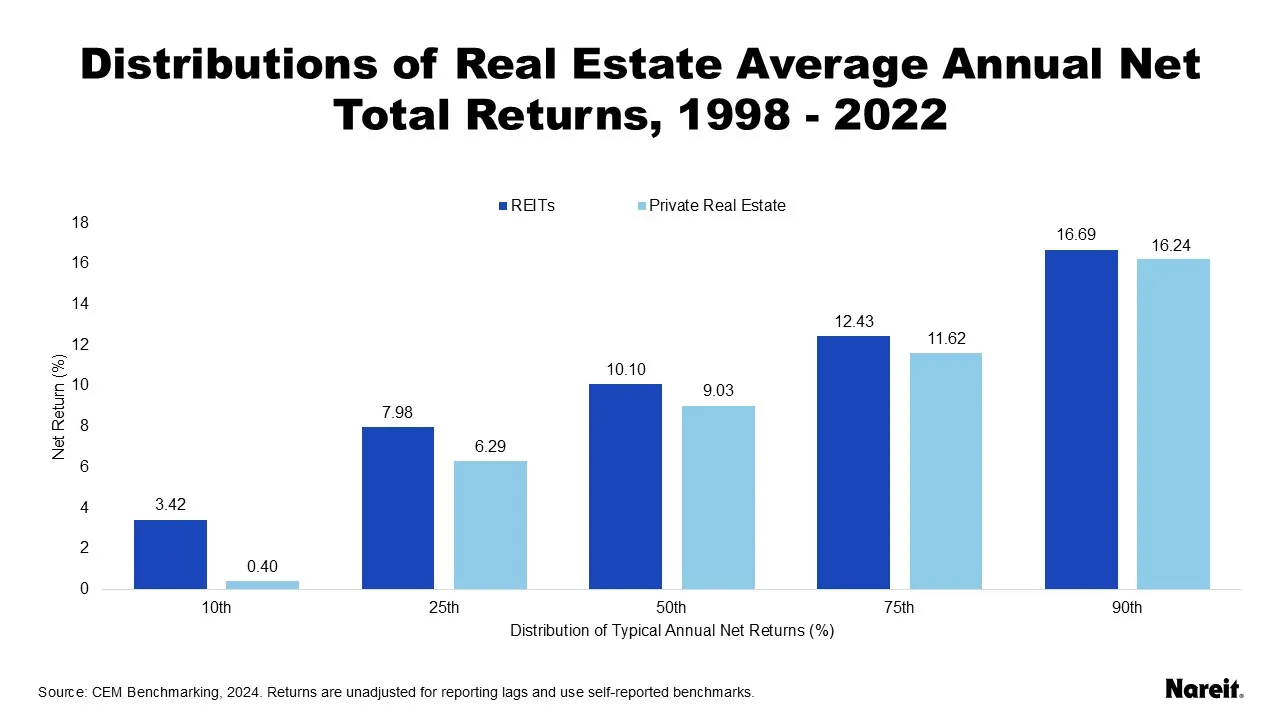

Even though realized pension investment returns have shown that, on average, REITs have outperformed private real estate, some investors still believe that private real estate can outperform REITs through the selection of top-quartile managers who display persistently high performance. Using CEM data from 1998 to 2022, the chart above explores this notion by showing the average annual net total return distributions for REITs and private real estate across the 10th, 25th, 50th, 75th, and 90th percentiles.

Across the distributions, REITs outperformed private real estate. At the lowest examined performance levels (10th percentiles), REIT outperformance was highest at 3.02%. Among the top-performing funds (90th percentiles), REIT outperformance was lowest at 0.45%. Given the consistent REIT outperformance across the distributions, investors who possess superior private real estate fund selection skills may be better off if they could adapt those skills to select top-performing REIT funds.

CEM data shows that the alpha conversation for public and private real estate is nuanced. Given that only REITs delivered alpha after accounting for investment management fees and that REITs outperformed private real estate across the distributions of net total returns, institutional investors should take a closer look at how REITs can play greater tactical and strategic roles in their investment portfolios. REITs can help investors by complementing existing portfolio allocations, providing broader diversification benefits, offering relative value opportunities, and improving overall portfolio performance.