Hodes Weill & Associates (HW) recently published a thoughtful research note, REITs versus Private Real Estate Funds: Partners, Not Rivals, that addressed the merits of public and private real estate in an institutional investor’s portfolio. The sentiment suggested by the article’s title is correct. Public and private real estate complement each other. But, using actual, realized pension fund investment return data from CEM Benchmarking (CEM)—rather than the simulations employed in the HW study—a better understanding can be had of how public and private real estate investments have performed across a variety of market cycles.

Specifically, CEM data have shown that:

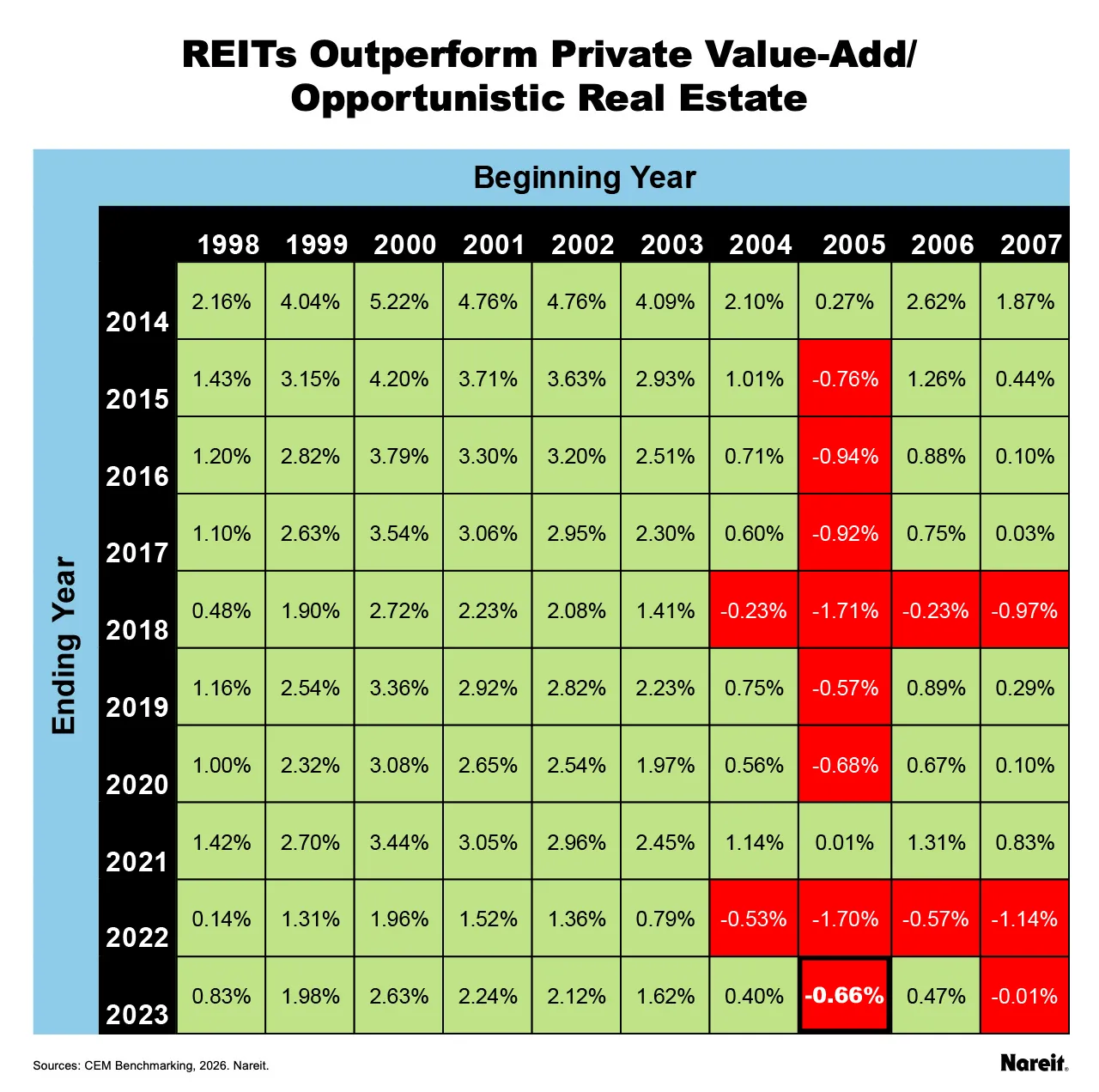

- REITs outperformed private value-add/opportunistic real estate investments in 85 of the 100 examined time periods.

- Over the longest time period available, 1998 through 2023, REITs outperformed private value add/opportunistic real estate funds by 0.83% per year on a net total return basis.

- REITs also substantially outperformed private core real estate, posting superior net total returns in 96 of the 100 examined time periods.

- From 1998 to 2023, REITs, on average, outperformed private core real estate investments by 1.75% on an annual net total return basis.

CEM is a global investment and pension administration benchmarking firm with access to a rich proprietary dataset on pension investment performance. CEM’s 2026 study, sponsored by Nareit, provides a unique lens and comprehensive look at realized investment performance across asset classes, including real estate and its investment styles, over a 26-year period (1998–2023) using a dataset covering public and private sector pensions with nearly $4 trillion in combined assets under management. An important and distinguishing feature of this data is that it provides the actual realized performance, net of investment costs, of the assets chosen by plan managers.

The HW study found that private value-add real estate funds moderately outperformed REITs from 2005 to 2023. CEM data indicated a similar finding over the same time period, but the opposite results were found if the time period started just a year earlier or later. These reversals highlight the time sensitivity of investment return measurement. A broader review of the CEM data revealed that, on average, REITs have generally outperformed private value-add/opportunistic real estate investments on an annual net total return basis.

Using CEM data, the table above displays REIT performance relative to private value-add/opportunistic real estate investments on a net-of-fee total return basis. Time period starting and ending years range from 1998 to 2007 and 2014 to 2023, respectively, resulting in a grid of 100 observations (time periods). Each time period where REITs outperformed is shaded green; periods with REIT underperformance are colored red. The outline of the cell for the time period used in the HW study, 2005 to 2023, is bolded, as is its REIT relative performance metric.

REITs outperformed private value-add/opportunistic real estate investments in 85 of the 100 examined time periods. The majority of periods where REITs underperformed (eight of 15) had a start year of 2005. In that year, REITs were placed behind the eight ball as they underperformed private value-add/opportunistic real estate by 20.91%. Over the longest time period available, 1998 through 2023, REITs outperformed private value add/opportunistic real estate funds by 0.83% per year.

The HW study also found that REITs substantially outperformed private core real estate funds from 2005 to 2023. CEM results were consistent with this finding and confirmed its robustness.

Using the same formatting and data source as the previous exhibit, the table above displays REIT performance relative to private core real estate investments. REITs outperformed private core real estate in 96 of the 100 examined time periods. In the few periods when REITs underperformed, the shortfall averaged less than 1% per year. Using CEM’s full history (1998 to 2023), REITs, on average, outperformed private core real estate investments by 1.75% on an annual net total return basis.

Ultimately, the goal for any institutional investor should be to build a resilient portfolio that leverages the unique strengths of both public and private real estate. CEM data have demonstrated that, on average, REITs have generally delivered superior net-of-fee total returns compared to private value-add/opportunistic and core real estate investments. These attractive return characteristics should serve as catalysts for investors to explore how REITs can play more significant tactical and strategic roles in their investment portfolios. REITs can help investors by offering relative value opportunities, complementing existing portfolio allocations, providing broader diversification benefits, and improving overall portfolio performance.