The wide gap between public and private real estate valuations has remained stubbornly slow-to-close. While REIT implied cap rates have meaningfully reacted to market forces, private real estate appraisal cap rates appear to be stuck in a rut and seem disconnected from reality. Proof of their struggle to embrace current market conditions lies in the relationship between private appraisal cap rates and the 10-year Treasury yield. Appraisal cap rates have unrealistically continued to maintain only a slight premium to the 10-year Treasury yield.

The inability of appraisers and portfolio managers to mark their real estate assets to market has not gone unnoticed. In a recent paper, Jeffrey D. Fisher, professor emeritus at Indiana University and consulting director of research and education for the National Council of Real Estate Investment Fiduciaries (NCREIF), recognized the shortcomings of the traditional real estate appraisal process in volatile markets and proposed a supplemental framework to assist appraisers in reconciling value indications using market-based rationales.

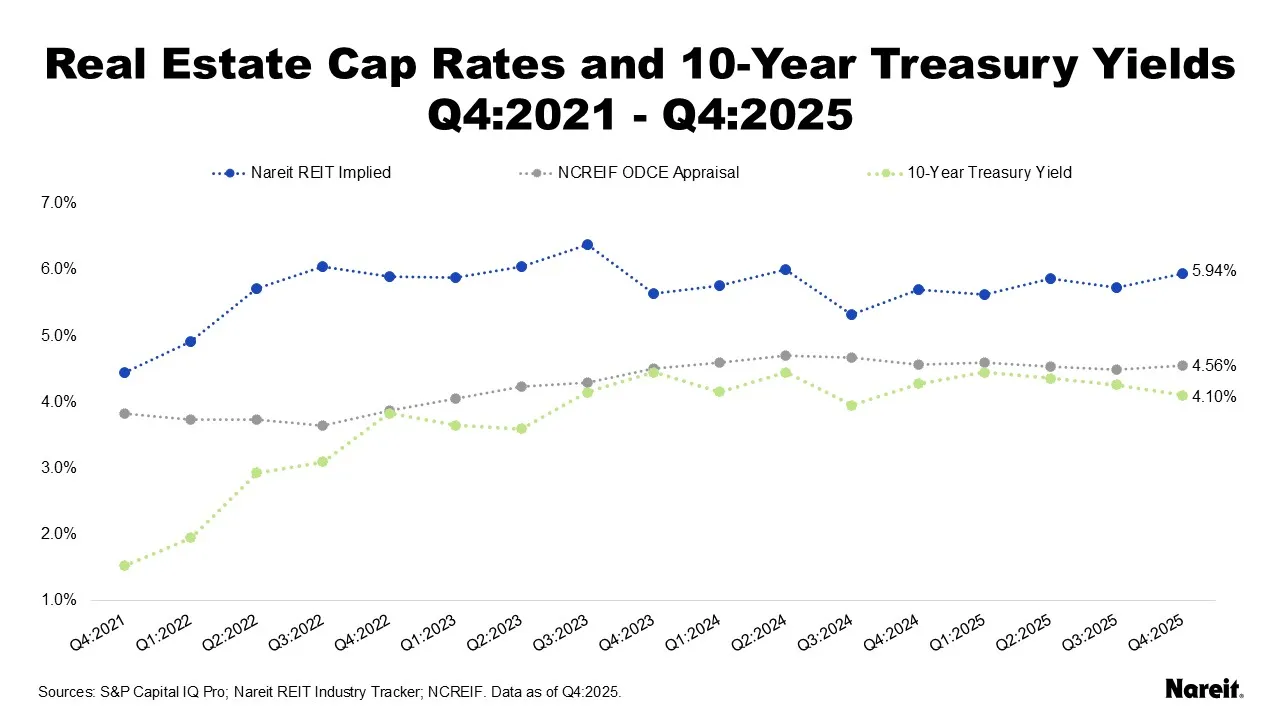

The chart above displays REIT implied cap rates from Nareit’s REIT Industry Tracker and private real estate appraisal cap rates from properties in the NCREIF open end diversified core equity (ODCE) funds, as well as average U.S. 10-year Treasury yields, since the fourth quarter of 2021.

The tenure of the current public-private real estate valuation divergence has now reached four years. As of the fourth quarter of 2025, the REIT implied and private real estate appraisal cap rates were 5.94% and 4.56%, respectively, resulting in a spread of 138 basis points. Highlighting private real estate appraisers’ and portfolio managers’ inaction, the appraisal cap rate has been essentially unchanged since the end of 2024. It has also continued to maintain a very modest spread over the 10-year Treasury yield; this is an untenable relationship.

Private real estate appraisal cap rates seem to be stuck in a rut. As appraisers and portfolio managers have been waiting for the market to come to them, the 10-year Treasury yield has increased dramatically since the start of the Iranian conflict; it stood at 4.30% at the end of March. With this rise in interest rates, it is unlikely that private real estate valuations have been meaningfully revised. The failure to properly value private assets has impeded the market’s price discovery process and limited liquidity, but it has also continued to increase the appeal of REITs. The closing of the public-private real estate cap rate gap is expected to result in REITs outperforming private real estate.