Styles change, but people can have trouble adapting to new trends. Some folks just cannot let go of their outdated hair and fashion choices from the past. Economic and financial conditions also change, and while investment valuations should reflect the current market environment, some private asset class valuations have failed to do so.

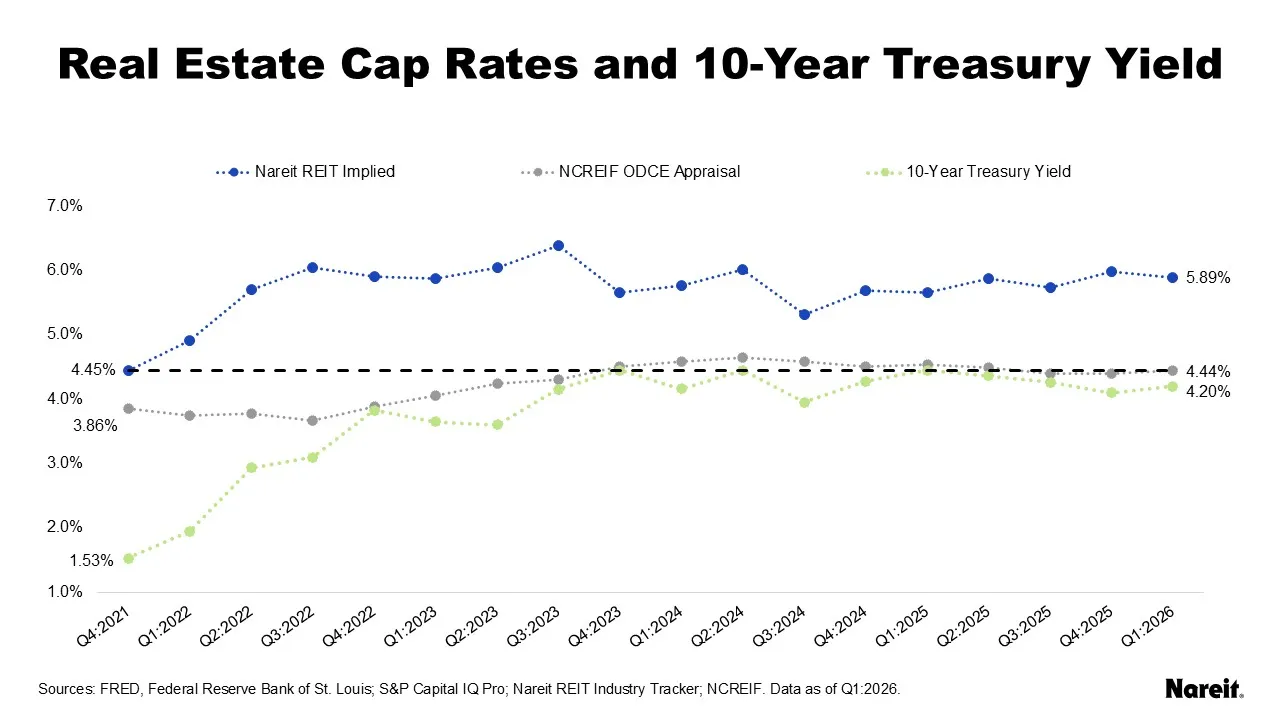

Recent data from Nareit’s Industry Tracker and NCREIF’s open end diversified core equity (ODCE) funds show that, on average, private real estate appraisal cap rates have essentially remained at year-end 2021 REIT implied cap rate levels for the past three years. Despite an elevated 10-year Treasury yield, private real estate appraisers and portfolio managers appear to be stuck in the past, valuing property like it’s 2021.

The chart above displays REIT implied cap rates from Nareit’s REIT Industry Tracker and private real estate appraisal cap rates from properties in the NCREIF ODCE funds, as well as average U.S. 10-year Treasury yields, since the fourth quarter of 2021. The chart also includes a horizontal black dashed line at the current ODCE appraisal cap rate level of 4.44%.

The current public-private real estate valuation divergence has continued to linger; its tenure has now reached 17 quarters. As of the first quarter of 2026, the REIT implied and private real estate appraisal cap rates were 5.89% and 4.44%, respectively. The resultant gap has remained wide at 1.45%. While the REIT implied cap rate has reacted meaningfully to changes in the 10-year Treasury yield, the private appraisal cap rate has not. The appraisal cap rate has essentially remained stagnant at the year-end 2021 REIT implied cap rate level for the past three years. This persistence suggests that the private real estate appraisal cap rate may have hit a ceiling.

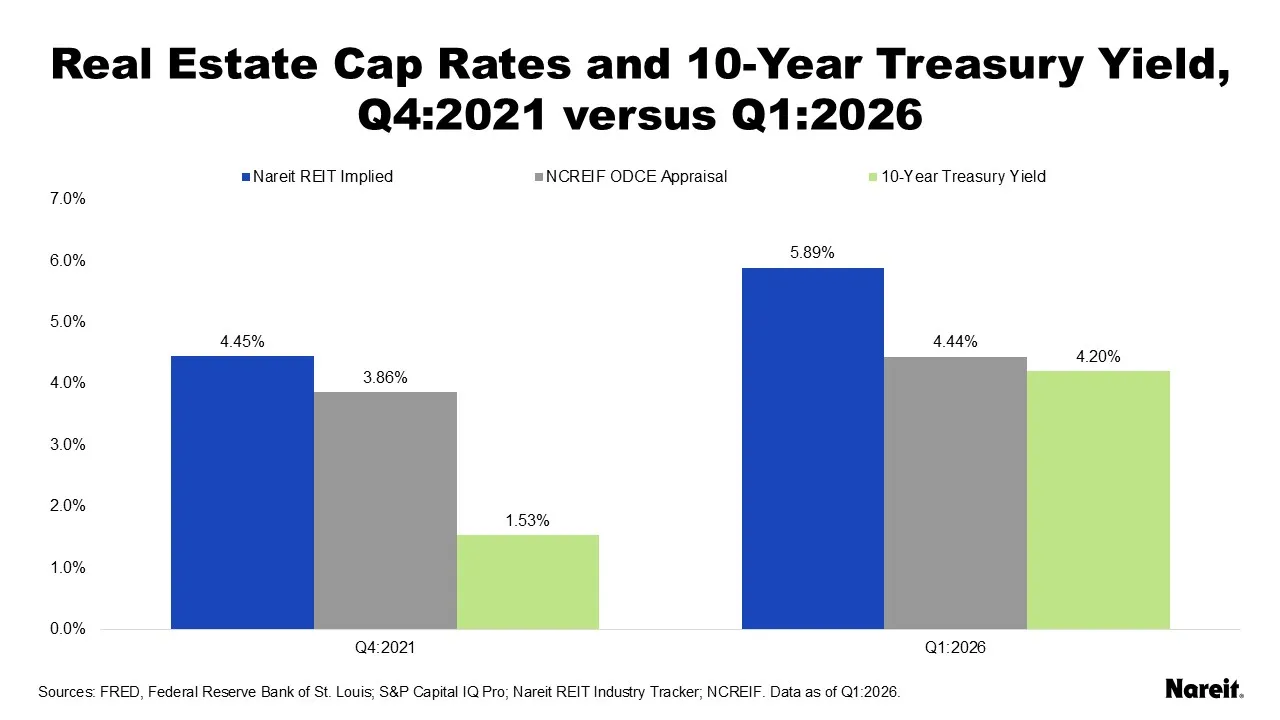

The chart above presents REIT implied cap rates, private real estate appraisal cap rates, and U.S. 10-year Treasury yields for the fourth quarter of 2021 and first quarter of 2026.

During the current divergence, the U.S. Treasury yield increased from 1.53% to 4.20%, a rise of 2.67%. The REIT implied cap rate reacted meaningfully to this rise, increasing by 1.44% from 4.45% to 5.89%. The change in the ODCE appraisal cap rate was just 0.58%; it reached 4.44% in the first quarter of 2026, standing at a level comparable to the REIT implied cap rate in the fourth quarter of 2021.

Throughout this dislocation, the REIT implied cap rate has maintained a material spread over the risk-free rate. It was 2.92% in the fourth quarter of 2021 and 1.69% in the first quarter of 2026. The ODCE appraisal cap rate spread was 2.33% and 0.24% in the early and later examined periods, respectively. The current modest spread remains an untenable relationship.

With the rise in the risk-free interest rate, the current private real estate appraisal cap rate appears to be disconnected from economic fundamentals and financial market realities. At current appraised values, these properties likely could not be sold in market transactions or receive bank financing. Historically divergences have closed through REIT outperformance and private real estate underperformance, which is likely to be the route in this cycle, but the timing of the convergence remains uncertain.