REITs have provided investors solid returns over the years, despite short-term zigs and zags along the way, in part because of structural features of the REIT model. Let’s take a look at two of them. First, REITs are an efficient, low-cost structure for managing commercial real estate, and second, most REITs align the incentives of management closely with shareholders’ interests, which motivates them to maximize value for the shareholders.

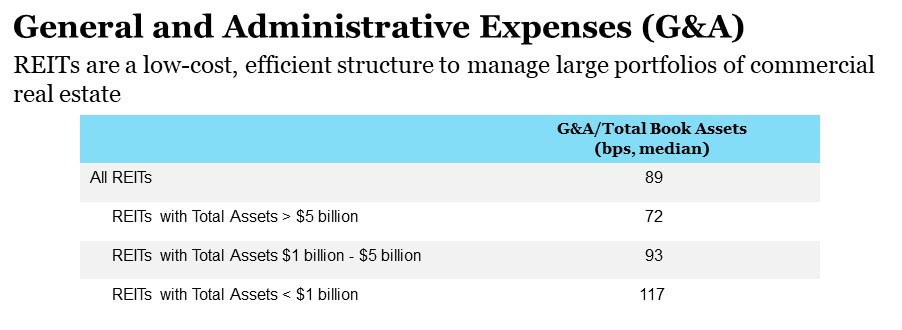

Most of the costs of owning and operating a portfolio of commercial buildings are reported under general and administrative expenses, or G&A. G&A represented 89 basis points of total book assets for the median REIT in 2017, according to their financial filings with the SEC. To get an idea of whether these total costs of less than one percent of assets are large or small, consider the management fees charged under the private equity real estate “2 & 20” model. Managers of these real estate funds typically take fees of up to two percent of assets under management (AUM), plus their incentive based on performance (often 20 percent of the return above a hurdle rate).

While the total fees for private equity real estate differ from year to year and from fund to fund, on average they charge as much as three times what REITs require to manage the same types of properties. Over the long haul, REITs avoid paying the extra one to two percent of assets that goes to the managers of a private equity fund, providing a strong tailwind for performance for REIT investors.

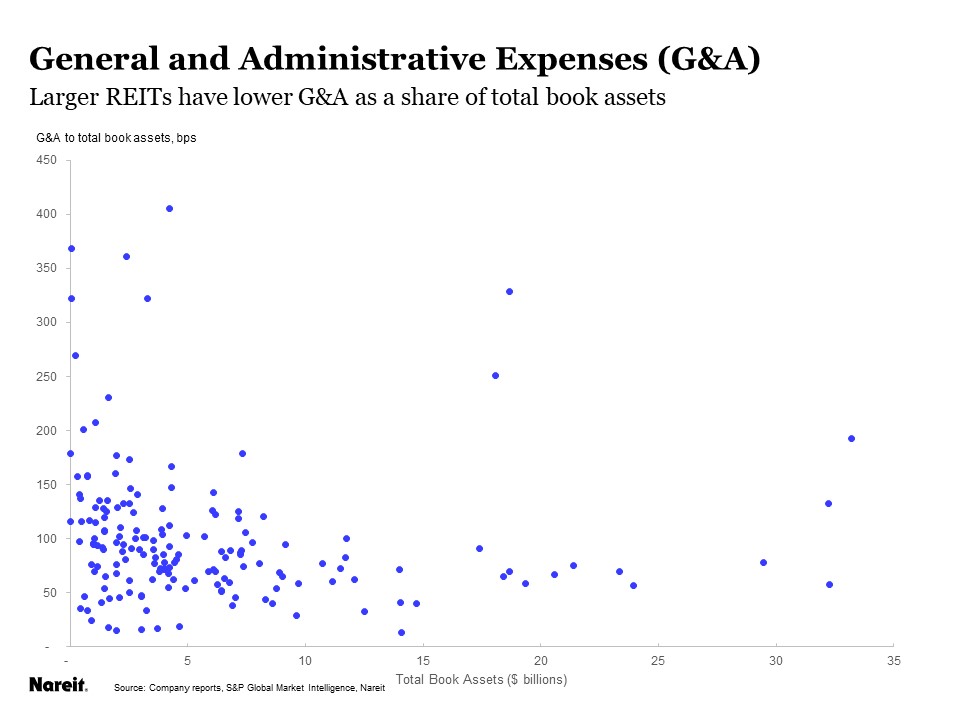

It is also interesting to note the economies of scale within the REIT industry, as larger REITs can manage significantly more real estate without a commensurate rise in costs. Among REITs with book assets over $5 billion, the median G&A charges were just 72 bps of total assets, compared to nearly 120 bps for the median REIT with assets below $1 billion. These scale efficiencies are among the factors that have encouraged M&A among REITs.

Another structural feature favoring REITs is that management faces strong incentives to pursue investors’ interests rather than their own. Consider the “2 & 20” model often used in private equity real estate. Managers receive two percent of AUM, but only if they actually deploy investors’ capital by buying properties. What happens if a private equity fund raises a lot of money, but has concerns that property values are overheating? The fund managers could look out for the investors and hold the money in cash, until they believe property values are more reasonable. But then they don’t get paid! Alternatively, they could buy properties despite concerns they may be overpaying. Too often, private equity real estate fund managers choose their own interests rather than those of the investor in the fund, paying top dollar at the peak of the market.

Incentive compensation in private equity funds (the “20” in 2 & 20) creates another conflict between the interests of managers and the investors in the fund. Management gets 20 percent of the upside once the fund returns exceed the hurdle rate, but don’t lose out for declines below the hurdle rate. This “heads-I-win, tails-you-lose” compensation often drives private equity fund managers to take on excessive risk in the fund investments, as they get a chunk of the upside but investors bear all the costs if the gamble doesn’t work out.

REITs do not suffer from these types of conflicts between management and investors. REITs avoid the weaknesses of management incentive structure in the private equity model discussed above by offering compensation that aligns the interests of management completely with those of investors. This is surprisingly easy to do! Most REITs do not base compensation on AUM or offering stock options, which have the same “heads-I-win, tails-you-lose” incentive for choosing riskier investments as the 2 & 20 model. Instead, they offer the CEO and other members of the management team shares in the company. These are the same class of shares owned by outside investors, so, by definition, management is motivated to act in the best interests of all investors. Furthermore, these stock grants typically have restrictions that require the management to hold them for several years. This makes them in the game for the long haul rather than short-term.

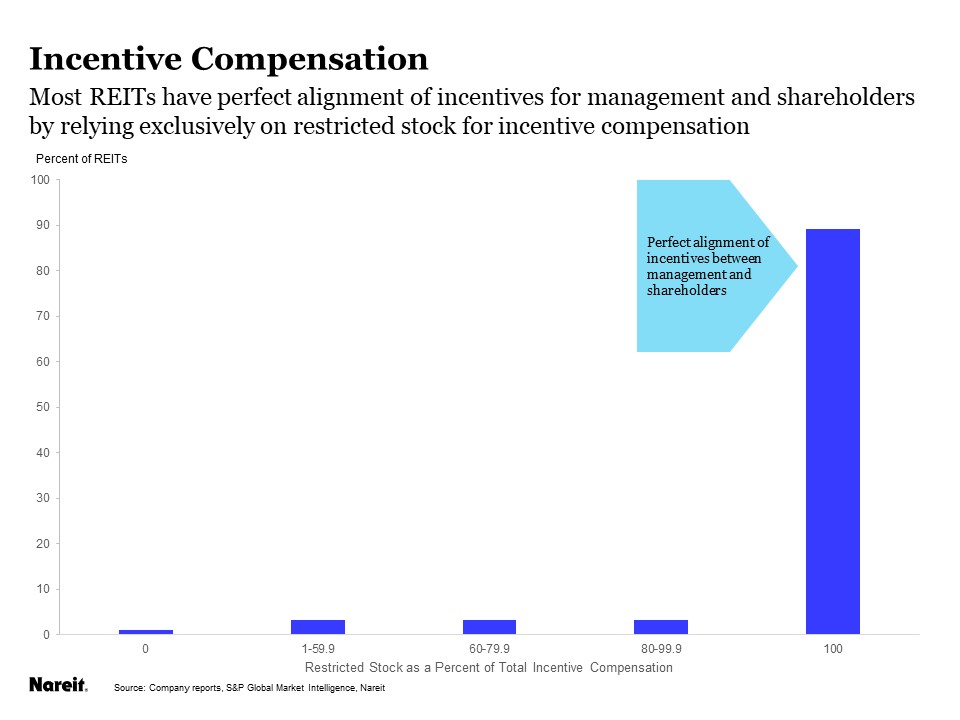

The vast majority of REITs provide 100 percent of the incentive compensation to management in the form of restricted stock (the right bar in the chart above). This ensures that management acts in the best interests of investors. Efficient management and alignment of incentives are important features in the favorable long-term performance of REITs.