A recent Nareit commentary highlighted that private real estate appraisers and portfolio managers seem to be valuing property like it’s 2021. Specifically, private real estate appraisal cap rates appear to have hit a ceiling, essentially remaining at year-end 2021 REIT implied cap rate levels for the past three years. Over this time, private appraisal cap rates have also maintained only modest spreads over U.S. 10-year Treasury yields, suggesting that private appraised property values are likely disconnected from economic and financial market realities.

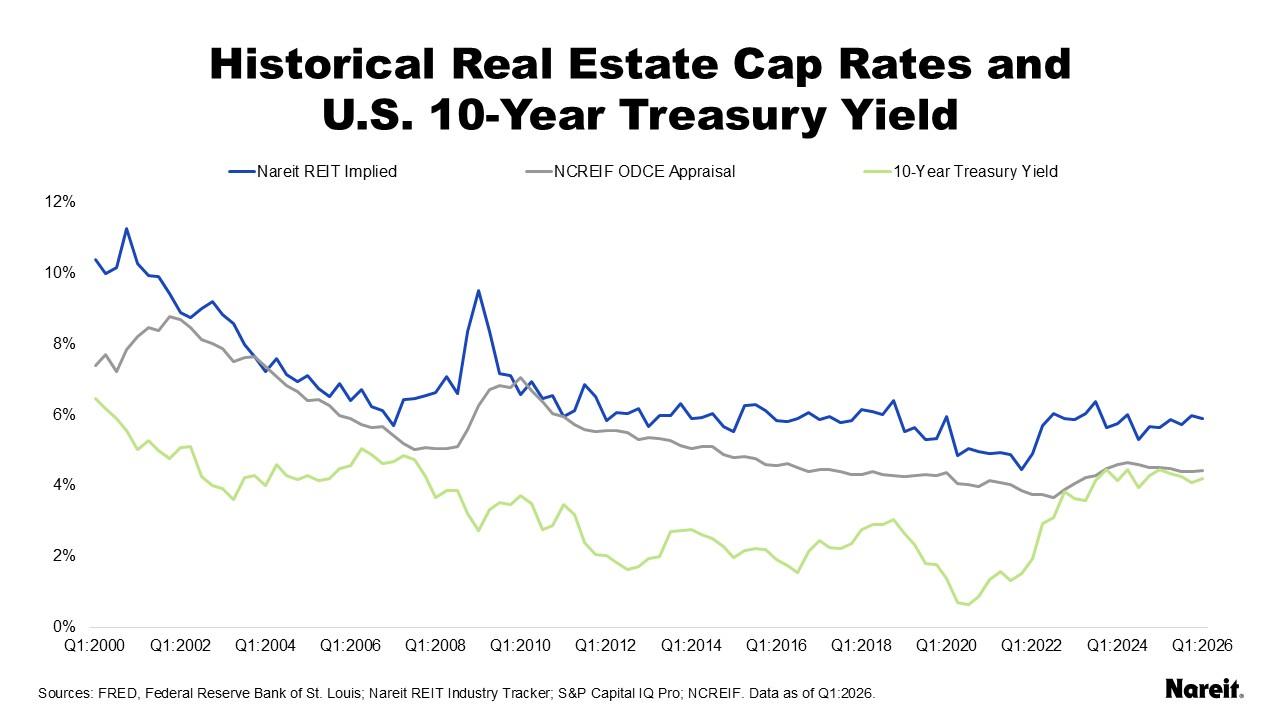

The chart above displays REIT implied cap rates from Nareit’s REIT Industry Tracker and private real estate appraisal cap rates from properties in NCREIF’s open end diversified core equity (ODCE) funds, as well as average U.S. 10-year Treasury yields, from the first quarter of 2000 to the first quarter of 2026.

Focusing on the relationship between the private real estate appraisal cap rate and U.S. risk-free interest rate, there have only been two periods when the gap between the NCREIF ODCE appraisal cap rate and the U.S. 10-year Treasury yield has narrowed substantially. The first occurrence was during the global financial crisis (GFC), but this narrowing was short lived. The second episode occurred during the current public-private real estate valuation dislocation. This time, however, the appraisal cap rate’s modest spread over Treasuries has persisted for years.

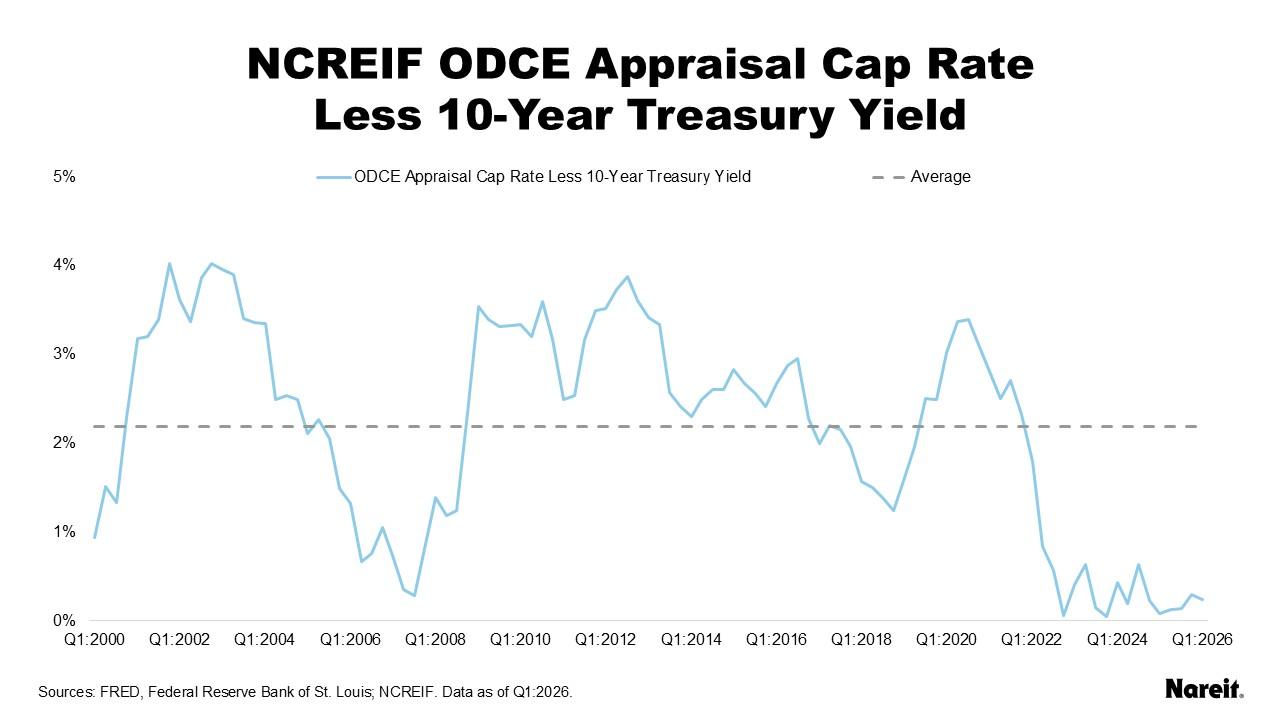

The chart above presents the simple difference between the NCREIF ODCE appraisal cap rate and the U.S. 10-year Treasury yield from the first quarter of 2000 to the first quarter of 2026, as well as the average private appraisal cap rate spread over the time period.

Over the examined timeframe, the average spread of the ODCE appraisal cap rate over the 10-year Treasury yield was 219 basis points. The spread fell below 50 basis points just 14 times; twice during the GFC and 12 times during the current public-private real estate valuation divergence. Excluding these observations, the average spread increased to 249 basis points.

The private real estate appraisal cap rate spread fell below 50 basis points during 12 of the last 14 quarters. Over this time, it averaged just 26 basis points. In comparison, the average REIT implied cap rate spread was 171 basis points and the spread of the Moody’s seasoned Aaa (Moody’s highest credit rating) corporate bond over the 10-year constant maturity Treasury averaged 94 basis points over the same time period. These comparisons highlight prolonged disconnections between private appraised property values and financial markets.

Although modest private appraisal cap rate spreads have persisted, they remain untenable. Private real estate appraisers and portfolio managers may have been hopeful that the market would come to them, but these hopes have been dashed by higher interest rates. In fact, recent U.S. 10-year Treasury yields have been higher than the most recent NCREIF ODCE appraisal cap rate. As private appraised valuations are ultimately marked to market, REITs are expected to benefit, outperforming their private market counterparts on a relative basis.