The global active manager tracker follows the quarterly investment holdings by the 25 largest actively managed funds invested globally. As of the end of first quarter of 2026, the funds were invested in 35 countries and regions with $17 billion in assets under management.

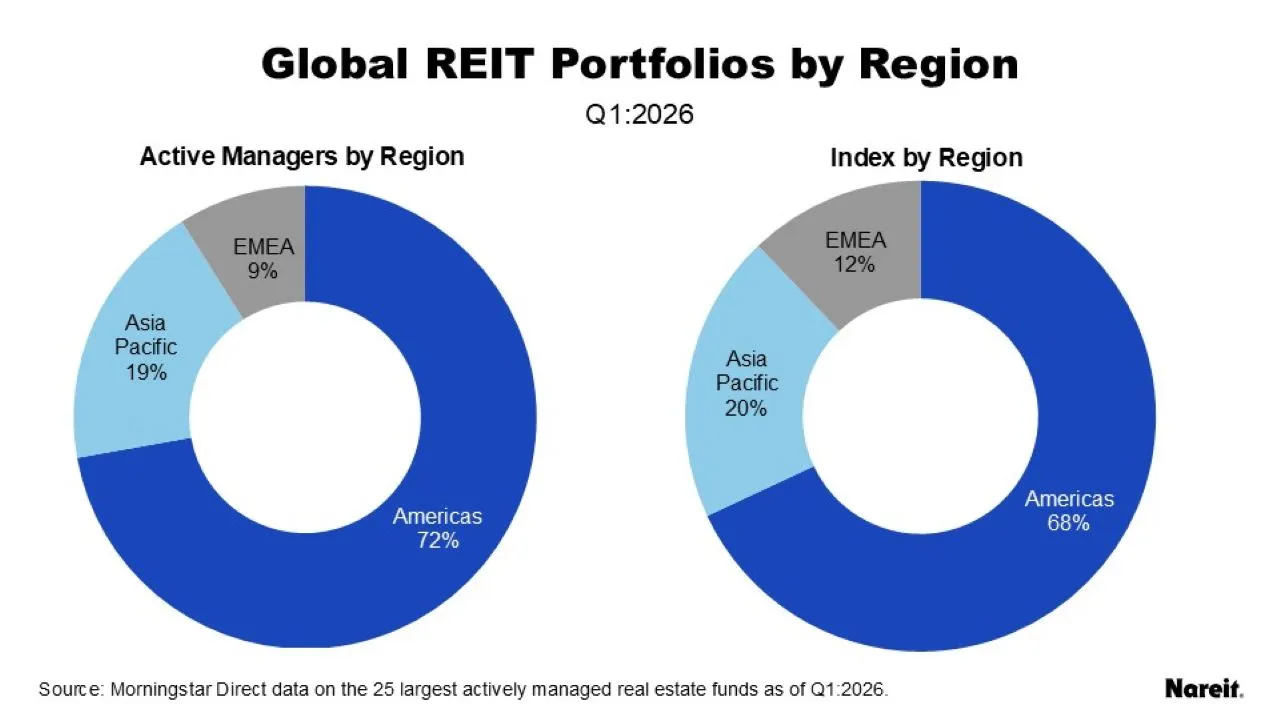

- In the first quarter of 2026, active managers maintained their overweight exposure in the Americas (AMER). In comparison, the Europe, the Middle East, and African region (EMEA) and Asia Pacific region (APAC) were underweight to the FTSE/EPRA Nareit Developed Extended Index. Although overall weights in the Americas increased quarter over quarter, they decreased year over year.

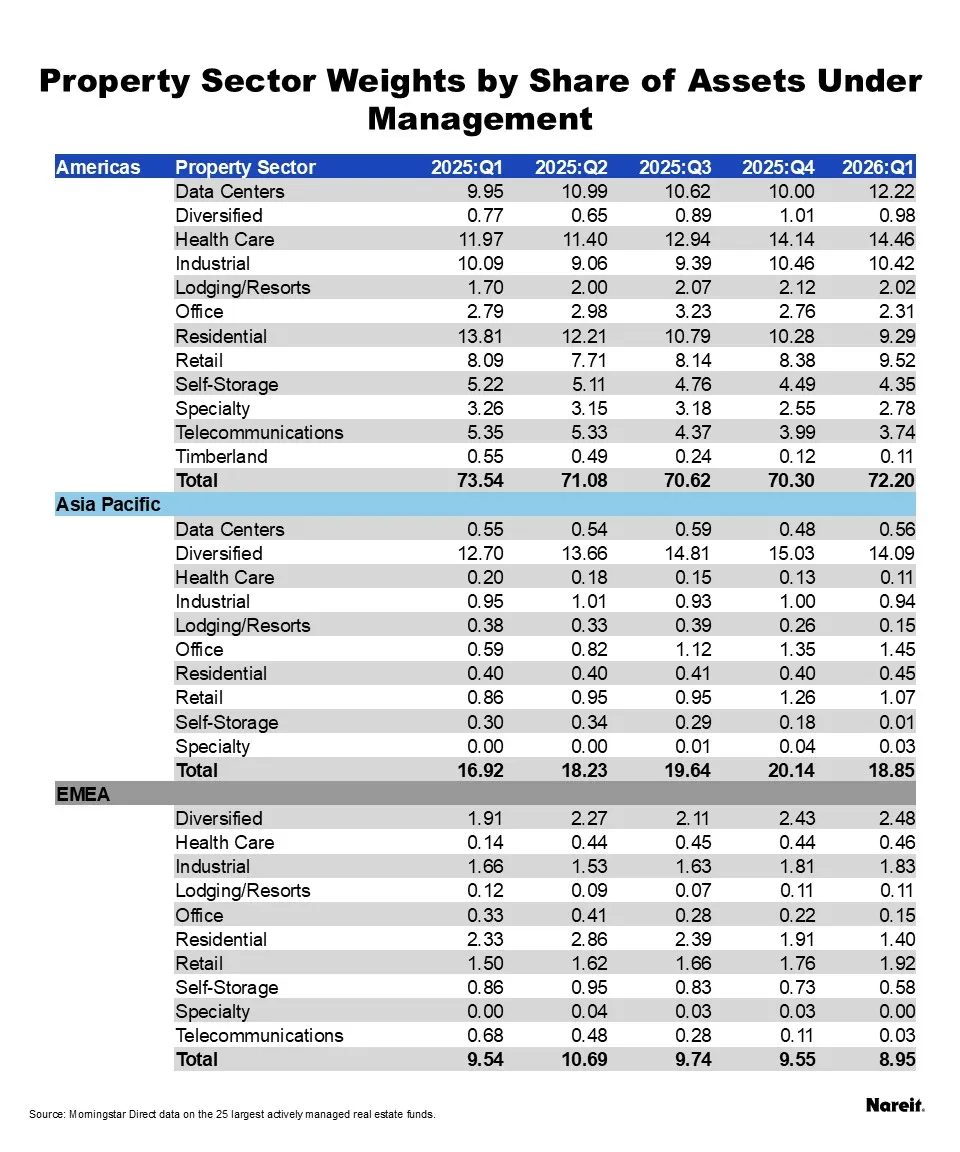

- AMER health care overtook APAC diversified as the largest allocation at 15%.

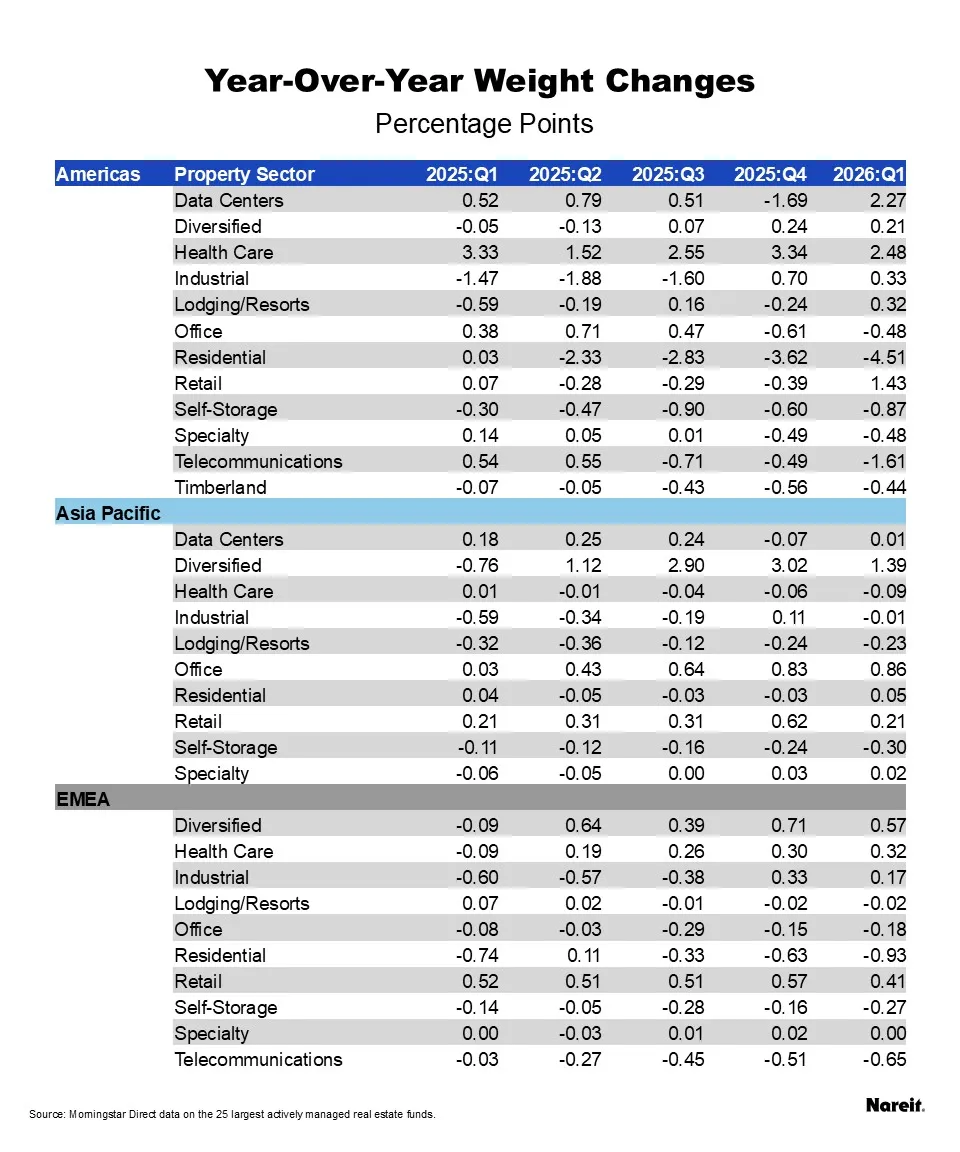

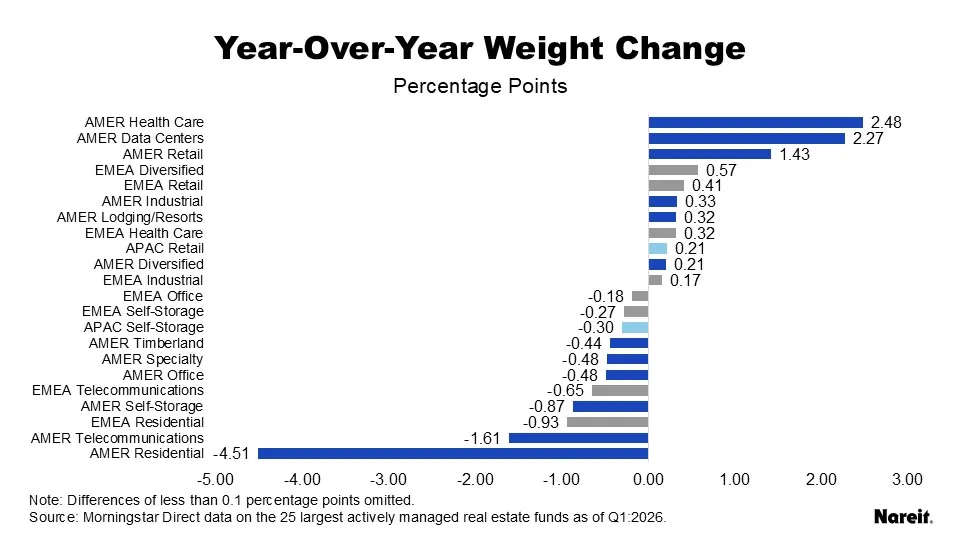

- AMER data centers had the largest quarterly gain of all regional sectors (up 2.2 percentage points), while AMER health care had the largest annual gain (up 2.5 percentage points).

- AMER data centers replace AMER health care as the most overweight sector. Data centers are overweight by 3.2 percentage points while health care is overweight by 2.4 percentage points.

- Within EMEA, retail saw the largest quarterly gain (up 0.2 percentage points), while diversified had the highest annual gain (up 0.6 percentage points).

- Within APAC, office posted the highest quarterly gain (up 0.1 percentage points) and diversified recorded the highest annual gain (up 1.4 percentage points).

Compared to the FTSE Nareit Developed Extended Index, the actively managed funds are overweight in AMER (primarily the U.S.) and underweight in EMEA and APAC as shown in the chart above.

The sector weights by region over the past five quarters are shown in the table above with the most recent quarter weights shown in the chart. With the funds overweight in AMER, most of the sectors in the region outweigh other regional sectors.

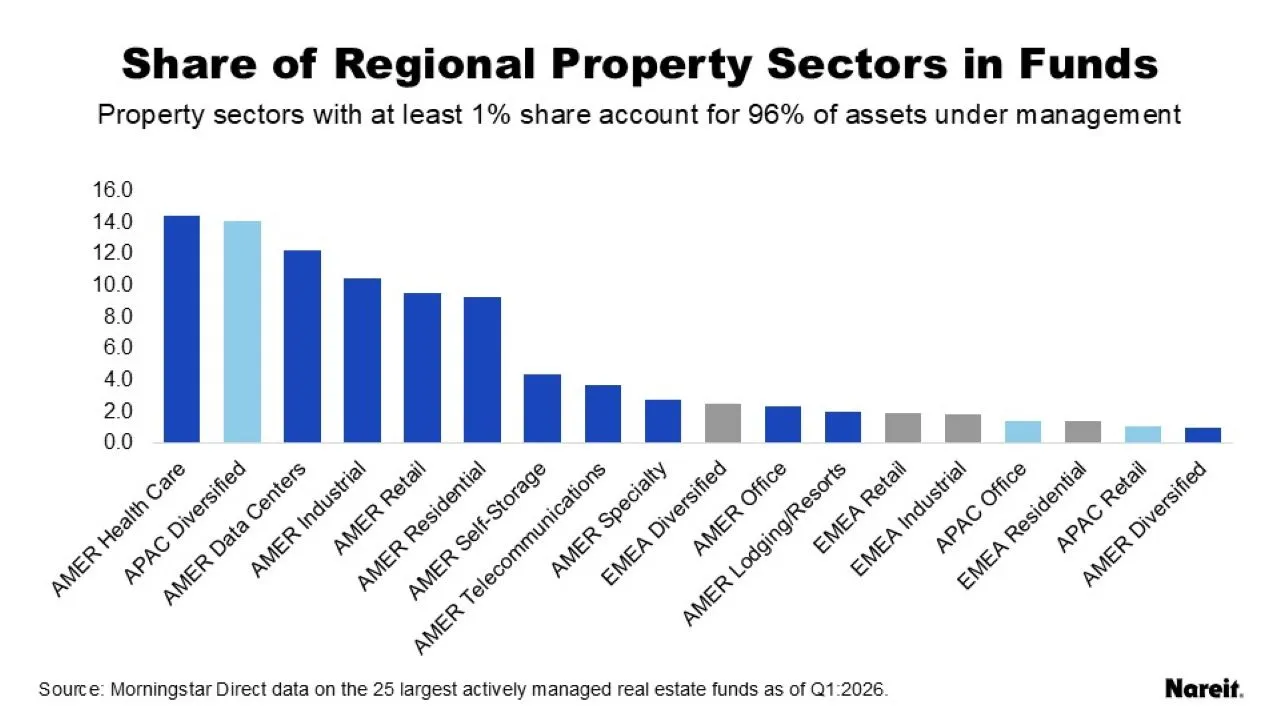

- AMER health care overtook APAC diversified as the largest allocation in the funds at 14.5%, increasing over the year.

- APAC diversified has the second highest allocation at 14.1% after decreasing slightly from 15.0% in the previous quarter.

- AMER data centers surged to 12.2% to take the third highest allocation, overtaking AMER industrial (10.4%) and AMER residential (9.3%), which continued its steady decline over the past year.

- For EMEA, the sector with the largest allocation is diversified at 2.5%, followed by retail at 1.9% and industrial at 1.8%.

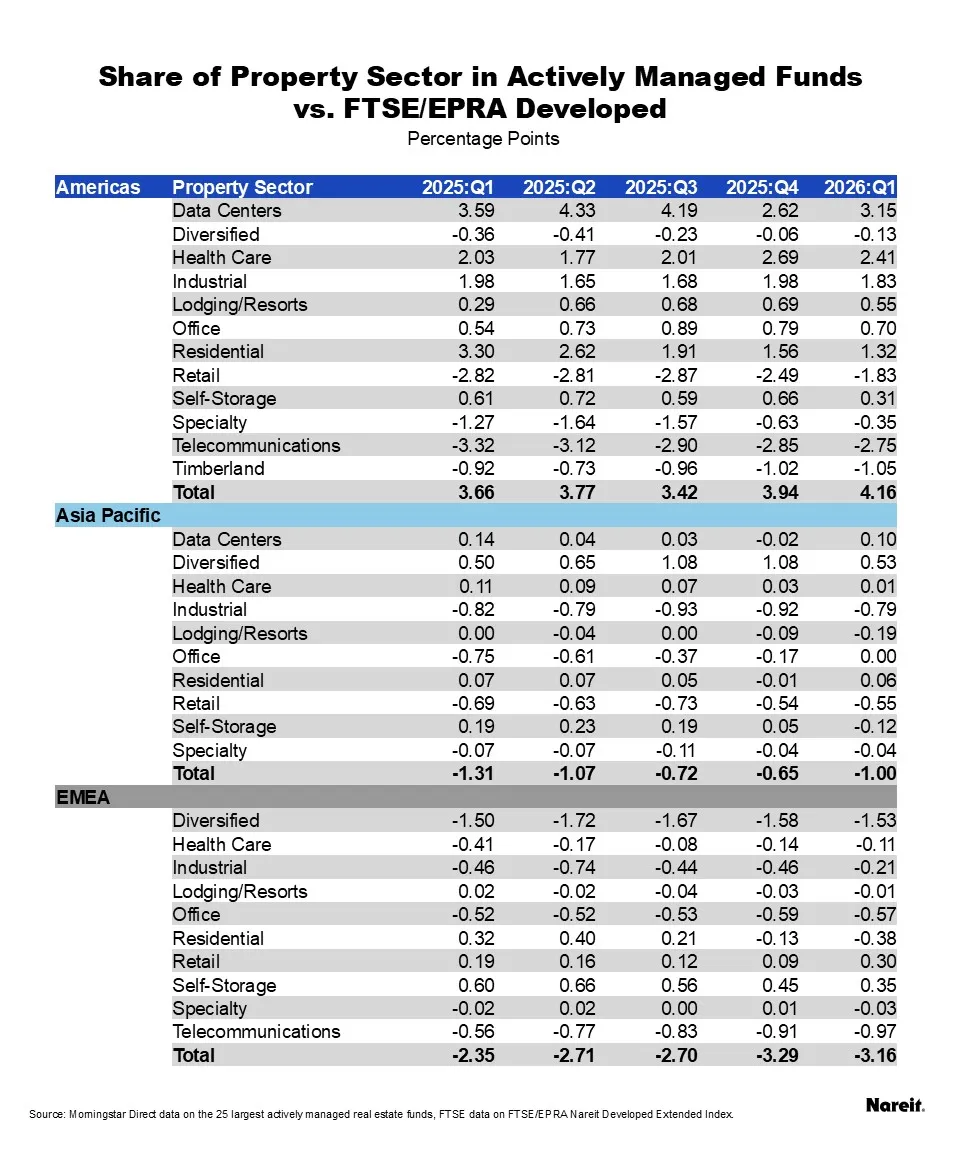

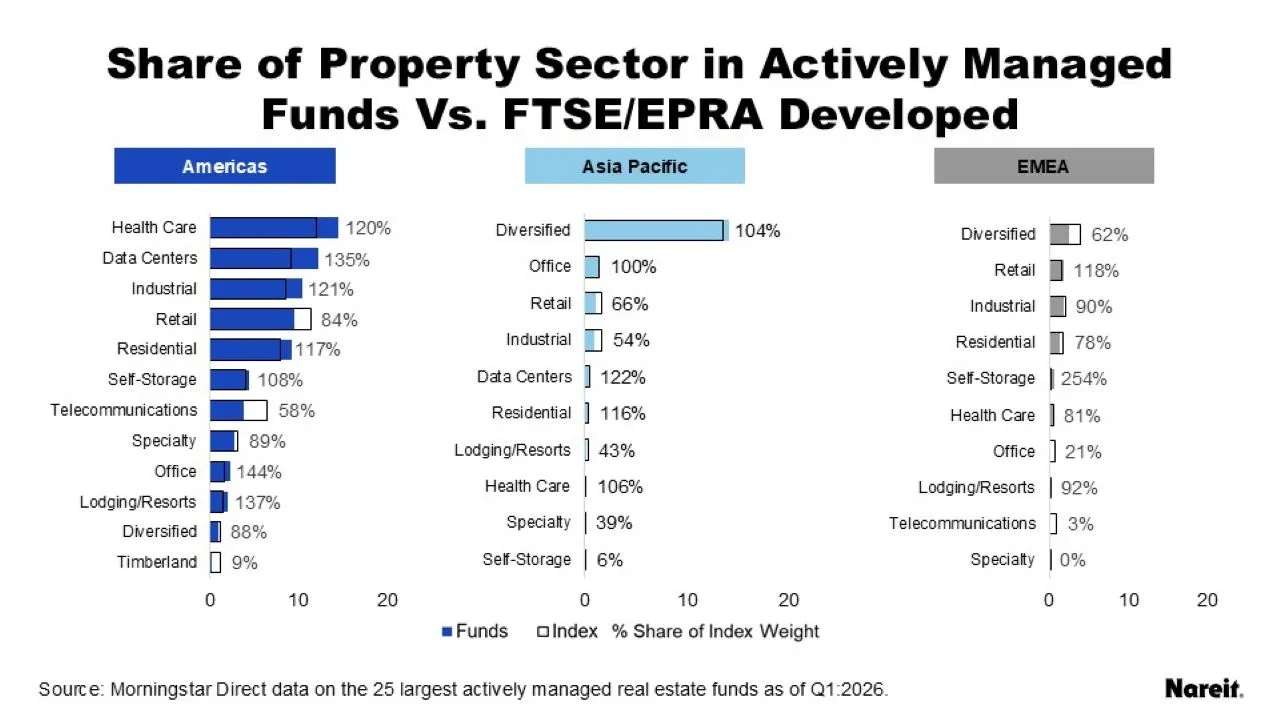

The charts and table above compare the weight of the sectors in actively managed funds to the weight of the sectors in the FTSE/EPRA Nareit Developed Extended index. The colored bars in the charts represent the weight of the regional sectors in the funds, the outlined bars represent their weights in the index, and the percentage represents the ratio of the fund weight to the index weight.

- AMER data centers is now the most overweight sector at 135% of its index weight. Seven out of 12 AMER sectors are overweight in the funds.

- Four out of 10 APAC sectors are overweight this quarter. Diversified, which comprised 13.6% of the FTSE/EPRA Nareit Developed Extended Index in the first quarter of 2026, was the most overweight APAC sector by 0.5 percentage points, 104% of its index share. APAC office notably sits at parity with the index in the first quarter of 2026.

- Just two sectors in EMEA are overweight this quarter, led by self-storage and followed by retail. EMEA self-storage is the most overweight of all the regional sectors by index share at 254% on a very small base; EMEA retail is overweight at 118% of index share.

- Other notably overweight AMER sectors by index share are office (144%) and lodging/resorts (137%).

- APAC overweight sectors by index share are led by data centers (122%) and followed by residential (116%), health care (106%) and diversified (104%).

- AMER telecommunications continues its position as the most underweight sector by 2.7 percentage points, just 58% of its index share. AMER retail follows at 84%, underweight by 1.8 percentage points, and then EMEA diversified at 62%, underweight by 1.5 percentage points.

- AMER timberland is under 10% of its index weight and EMEA office is only 21% of its index weight.

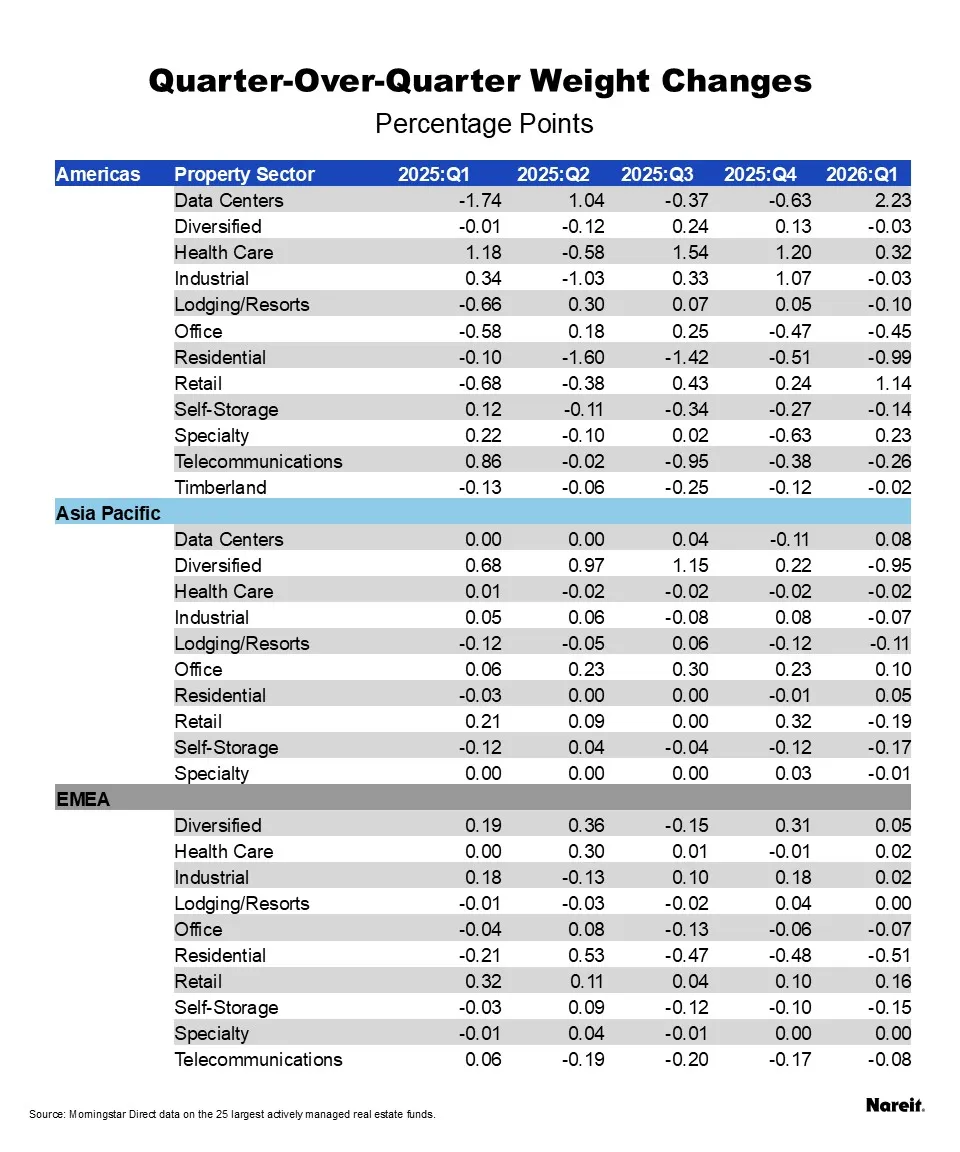

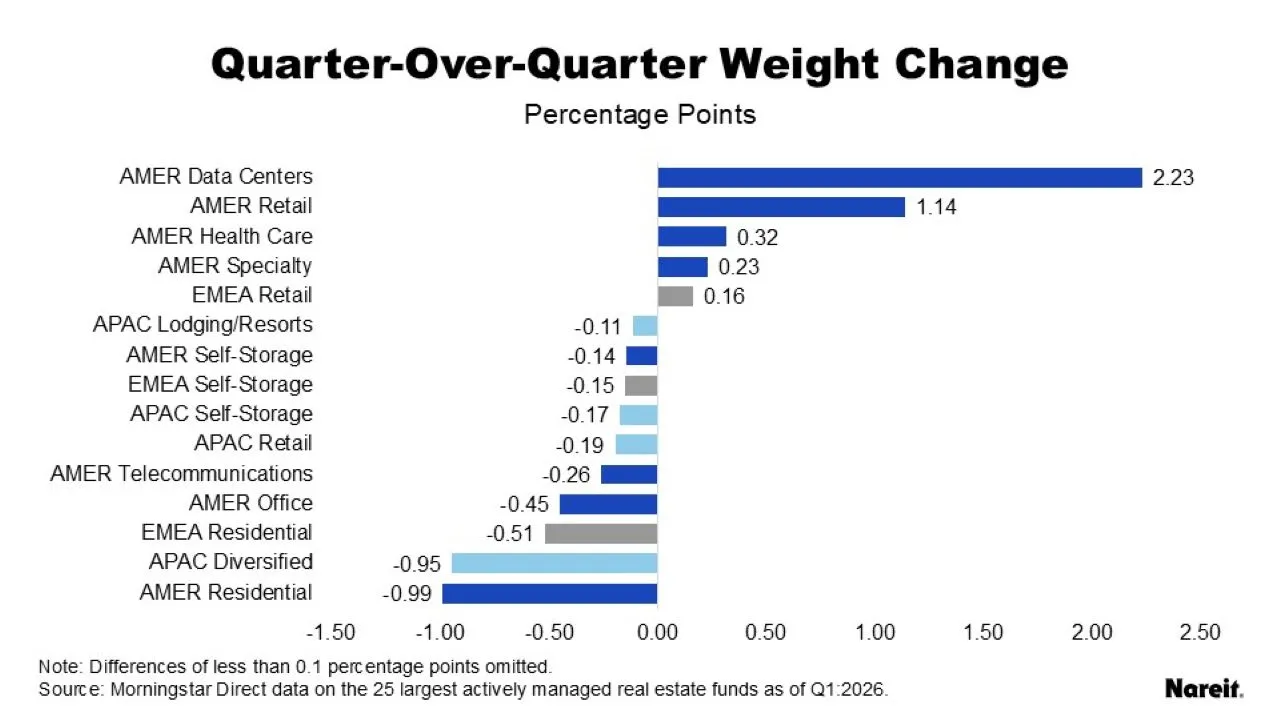

Changes from the previous quarter and previous year are shown in the tables and charts above.

- Overall, most property sectors in the AMER region showed modest annual declines with significant gains only in health care, data centers, and retail. For EMEA, losses and gains across sectors were evenly distributed on average. For APAC, there were neither large gains nor losses year over year.

- AMER health care had the largest annual gain in the first quarter, up 2.5 percentage points for the year. AMER data centers took the second spot annually, up 2.3 percentage points for the year, while claiming the largest quarter-over-quarter gain, up 2.2 percentage points.

- AMER retail had the second highest quarterly gain at 1.1 percentage points, after a year with both modest quarterly increases and quarterly decreases.

- For EMEA, diversified had the largest annual gains of 0.6 points. The quarterly gain was marginal, at less than 0.1%.

- AMER Residential had the largest declines for both the quarter and for the year, down 1.0 percentage points and down 4.5 percentage points, respectively. In the first quarter of 2026, the year-over-year loss in residential was its largest annual decline of the past year.

Note that two of the 25 funds had not reported first quarter data for this analysis.

For more information on the global active manager project, see New Actively Managed Global Real Estate Funds Tracker Shows Diversity in Geographic, Sector Holdings