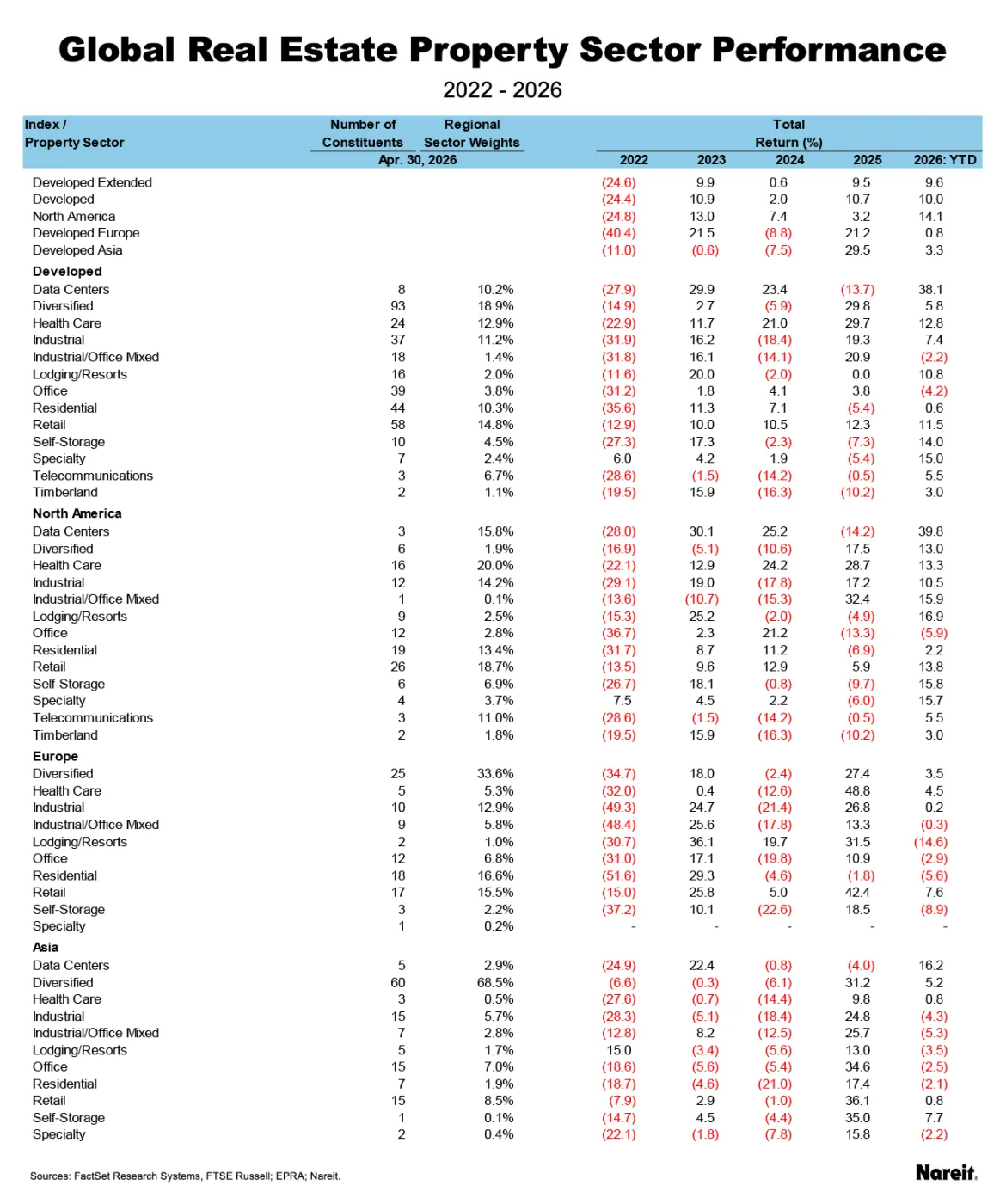

The FTSE EPRA Nareit Developed Extended Index and the FTSE EPRA Nareit Developed Index each returned 8.6% in April, as markets recovered from the volatility attributed to the conflict in the Middle East. On a year-to-date basis, the Developed Extended index has gained 9.6% and the Developed index is up 10.0%.

Broader market equities rebounded from the crisis as well, but on a year-to-date basis real estate continues to outperform by nearly 300 basis points. While the pause in open hostilities remains in place through early May, a long-term solution to the Middle East crisis remains outstanding and the longer-term impacts of the closure of the Strait of Hormuz will take time to assess.

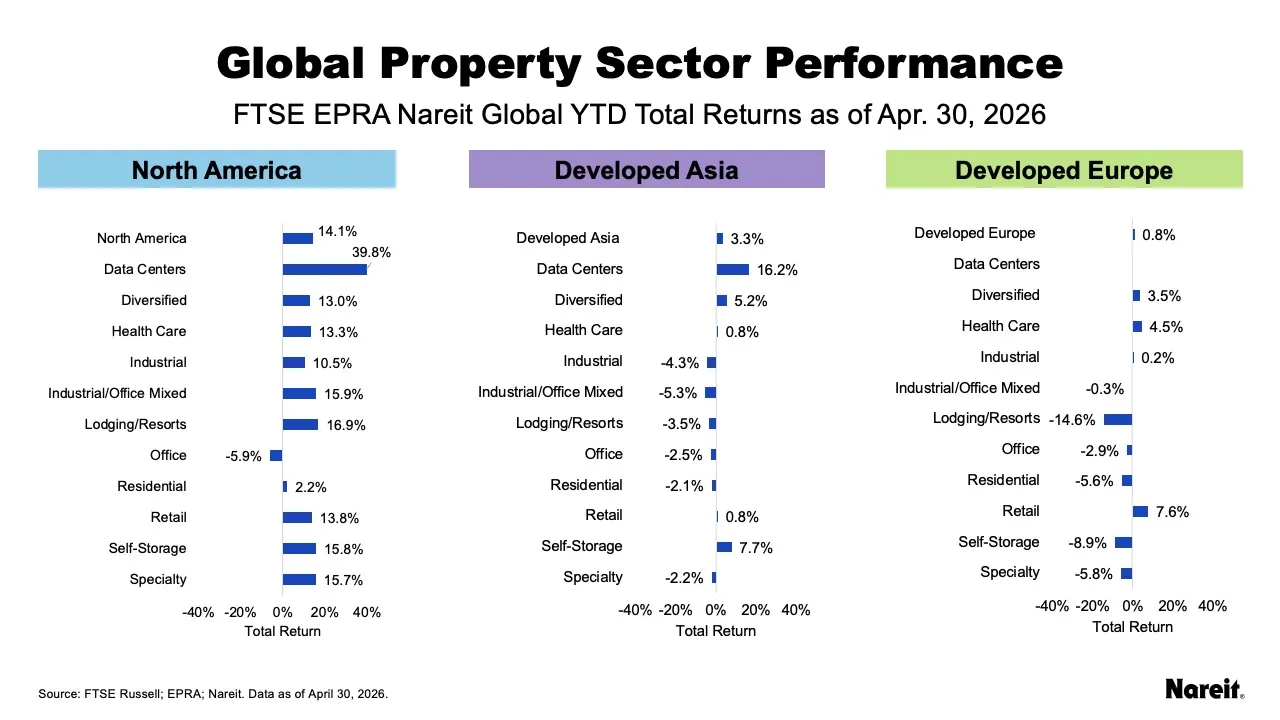

Global return figures mask a significant divergence in regional performance that has defined the market since the close of March. North America, which makes up 66% of the FTSE EPRA Nareit Global series, has outperformed with a 14.1% year-to-date total return while gains in Developed Asia and Developed Europe have been more subdued, with respective returns of 3.3% and 0.8%. This decoupling marks a sharp pivot from the start of the year; prior to the geopolitical volatility in the Middle East, all three regions were performing in lockstep, with each delivering year-to-date returns exceeding 11% through late February.

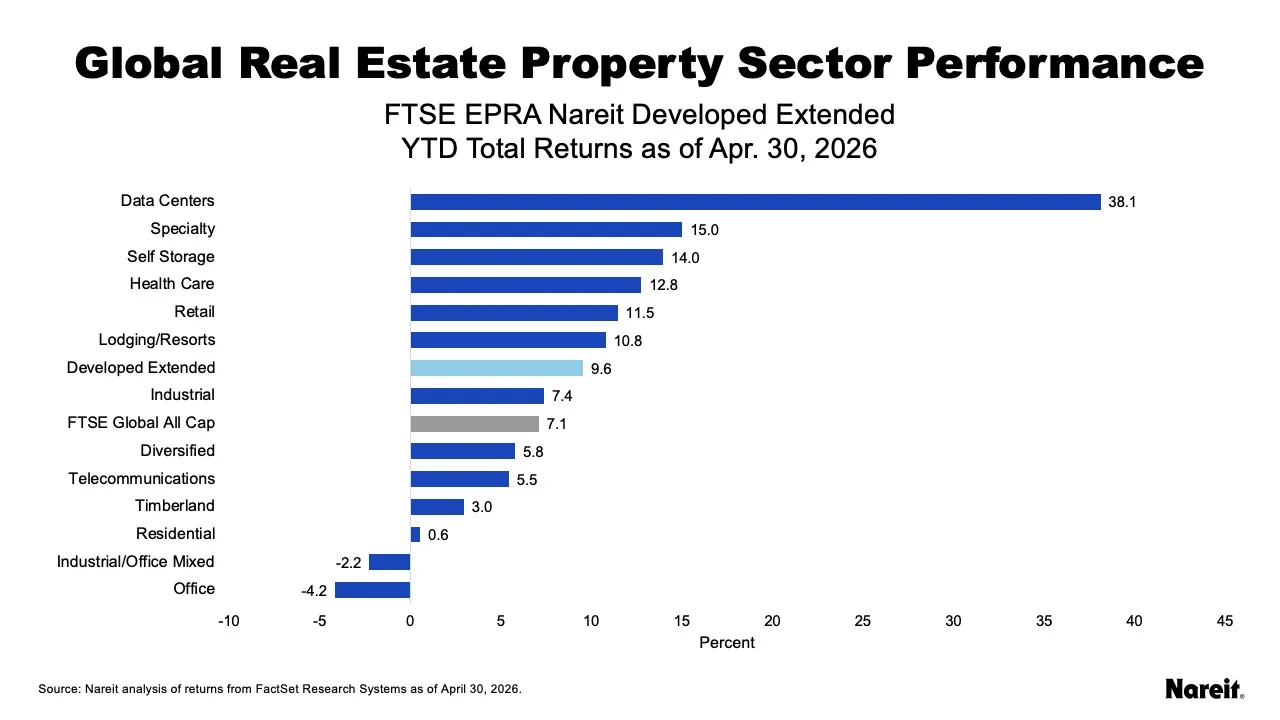

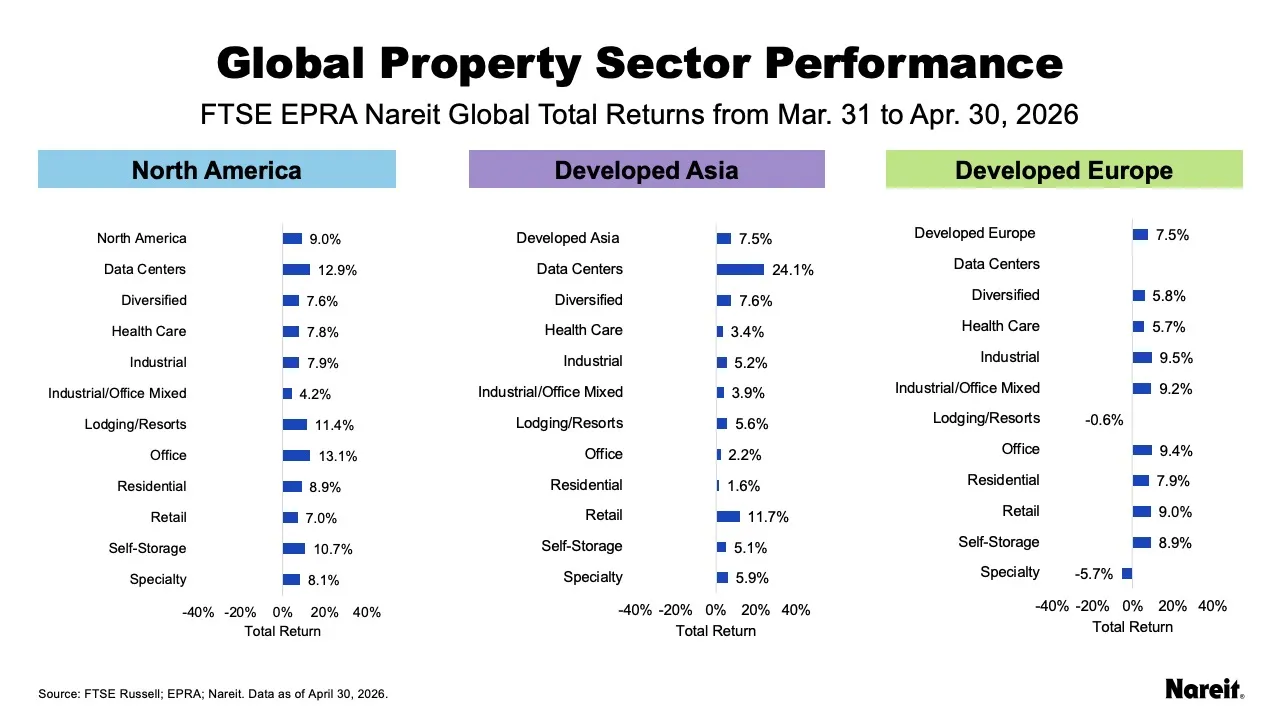

As reflected in the chart above, real estate has been broadly positive in 2026, led by data centers, specialty, and self-storage, with respective returns of 38.1%, 15.0%, and 14.0%. Global real estate performance in 2026 has been defined by three distinct phases: a robust start through February, a sharp correction related to geopolitical turmoil in March, and a broad recovery in April, led by North America. Performance across the following periods highlights the shifting market dynamics.

The above exhibit reflects the broad outperformance of North America on a year-to-date basis as of April 30, posting a total return of 14.1%, while Asia is up 3.3%, and Europe has risen 0.8%. Data centers lead in both North America and Asia, with respective total returns of 39.8% and 16.2%. Retail leads in Europe, returning 7.6%.

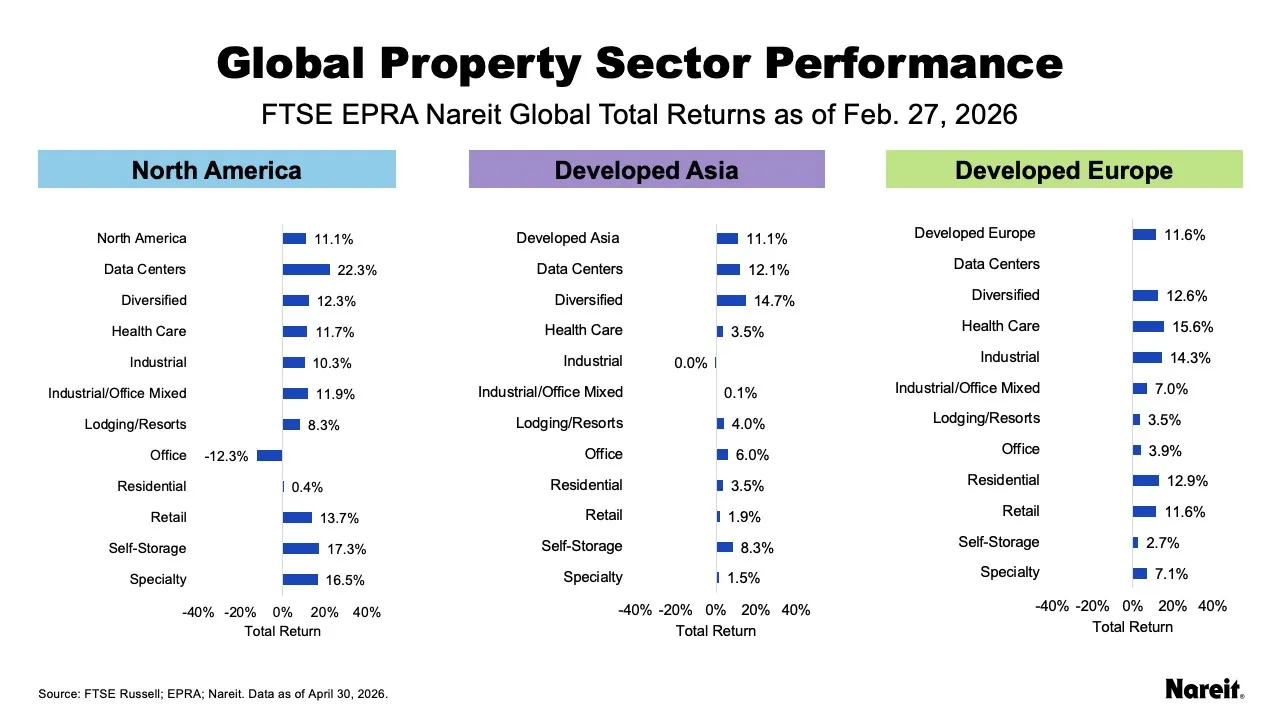

As reflected in the exhibit above, all regions showed strong growth through the end of February, with greater than 11% returns from each region, with data centers leading in North America, diversified leading in Asia, and health care outperforming in Europe. North American office was the lone sector exhibiting strong downward pressure. Real estate outperformed global equities as the FTSE Global All Cap returned 4.9% in this period.

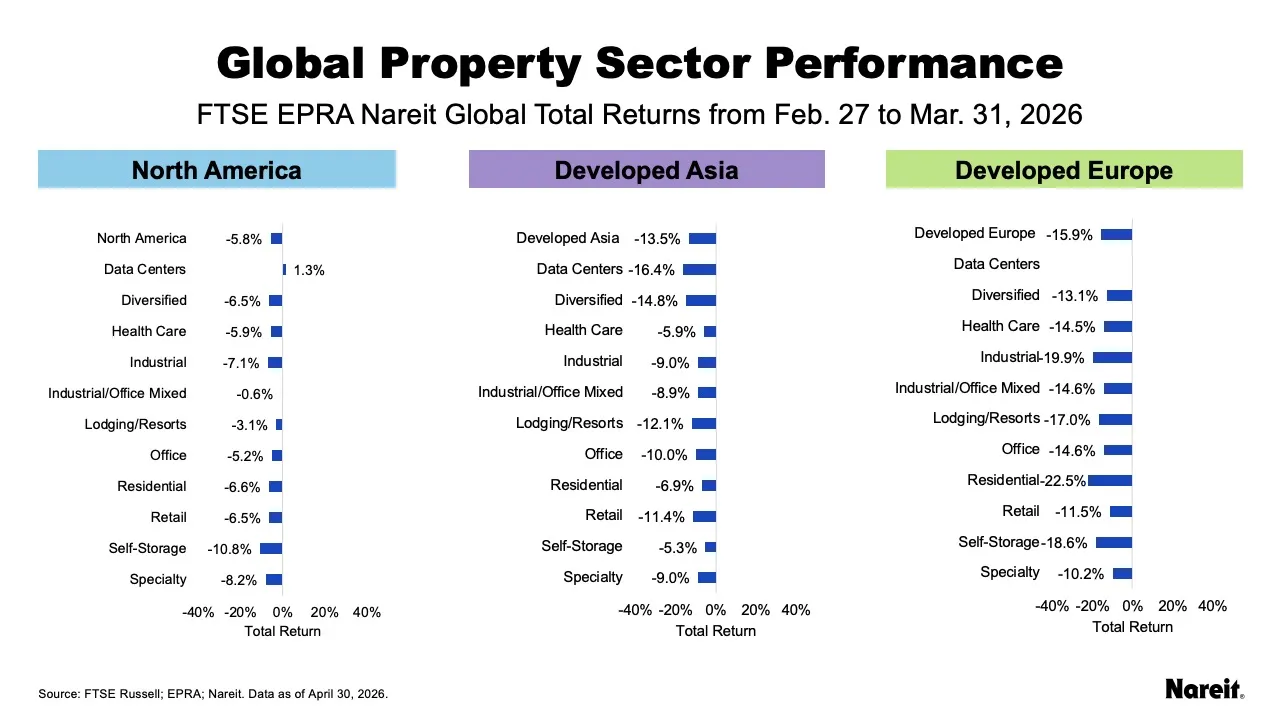

After the start of hostilities at the end of February, all regions pulled back, with North America proving the most resilient, as shown above. North America declined 5.8%, Asia was down 13.5%, and Europe fell 15.9%. North American data centers was the lone sector with positive returns during this period, rising 1.3%. In Asia, self-storage was most resilient, with a -5.3% return, while the specialty sector led in Europe with a decline of 10.2%. The FTSE Global All Cap fell 7.3% in March.

The above exhibit demonstrates that, after the pause in kinetic warfare at the end of March, all regions recovered, led by North America, with a total return of 9.0%, while Asia and Europe both rose 7.5%. Office led in North America, with a total return of 13.1%, followed closely by data centers, which rose 12.9%. Data centers led in Asia, returning 24.1%, and industrial rose 9.5% in Europe. Broad market equities outperformed over this period as the FTSE Global All Cap gained 10.1% in April.

Property Sector Highlights

As reflected in the preceding exhibits, technology-centric real estate has continued to provide a significant cushion against broader market headwinds throughout 2026. At the global level, the data center sector remains the clear leader, delivering a year-to-date total return of 38.1% through April 30. Conversely, office-related sectors have lagged. While office rallied strongly in North America during April, it continues to underperform globally, falling 4.2% on a year-to-date basis, while the industrial/office mixed sector is the only other sector posting negative returns in 2026, with a decline of 2.2%.

Regional Performance

North America

As reflected in the table above, North America was the primary driver of the global recovery in April, with the region's 9.0% total return for the month leading to a year-to-date total return of 14.1% as of April 30. The rally was broad-based but particularly strong in data centers. North American real estate navigated the volatile environment better than international peers, benefiting from relative insulation from Middle East energy shocks.

Developed Europe

Developed Europe also recovered, posting a monthly total return of 7.5%. The region’s year-to-date total return stands at 0.8% after the 15.9% decline suffered in March. Retail and health care lead on a year-to-date basis, with respective returns of 7.6% and 4.5%, while lodging/resorts has lagged with a return of -14.6%.

Developed Asia

Developed Asia posted a total return of 7.5% in April, bringing the region’s year-to-date total return to 3.3%. Data centers lead year-to-date with a total return of 16.2%. Self-storage followed with a return of 7.7%, while diversified, which accounts for 69% of the region, returned 5.2%.