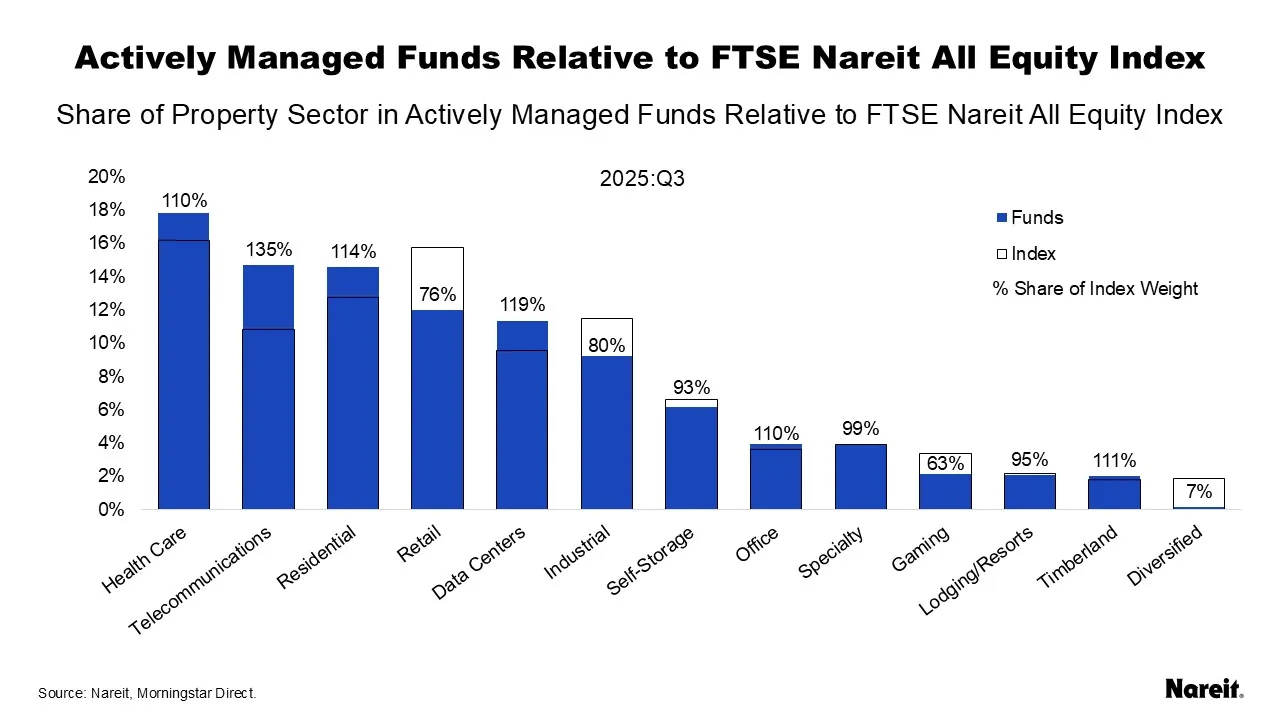

Nareit tracks quarterly investment holdings for the largest actively managed real estate investment funds focusing on REIT investment for insights into expert investor sentiment. In the third quarter of 2025, health care had the largest share in actively managed funds for the first time, as telecommunications dropped to second place.

Despite health care leading funds at nearly 18% of assets under management, telecommunications remained the most overweight sector relative to its index weight, invested at 135% of its index share. Recent recovery in sectors affected by the pandemic have led to office moving from underweight to overweight for the first time since the beginning of 2020, and lodging/resorts coming close to parity with their index shares.

Both office and lodging/resorts have seen steady gains through the past year and are among the few sectors that increased for both the quarter and annually. Office is now 110% of its index share, and lodging/resorts is at 99% of its index share.

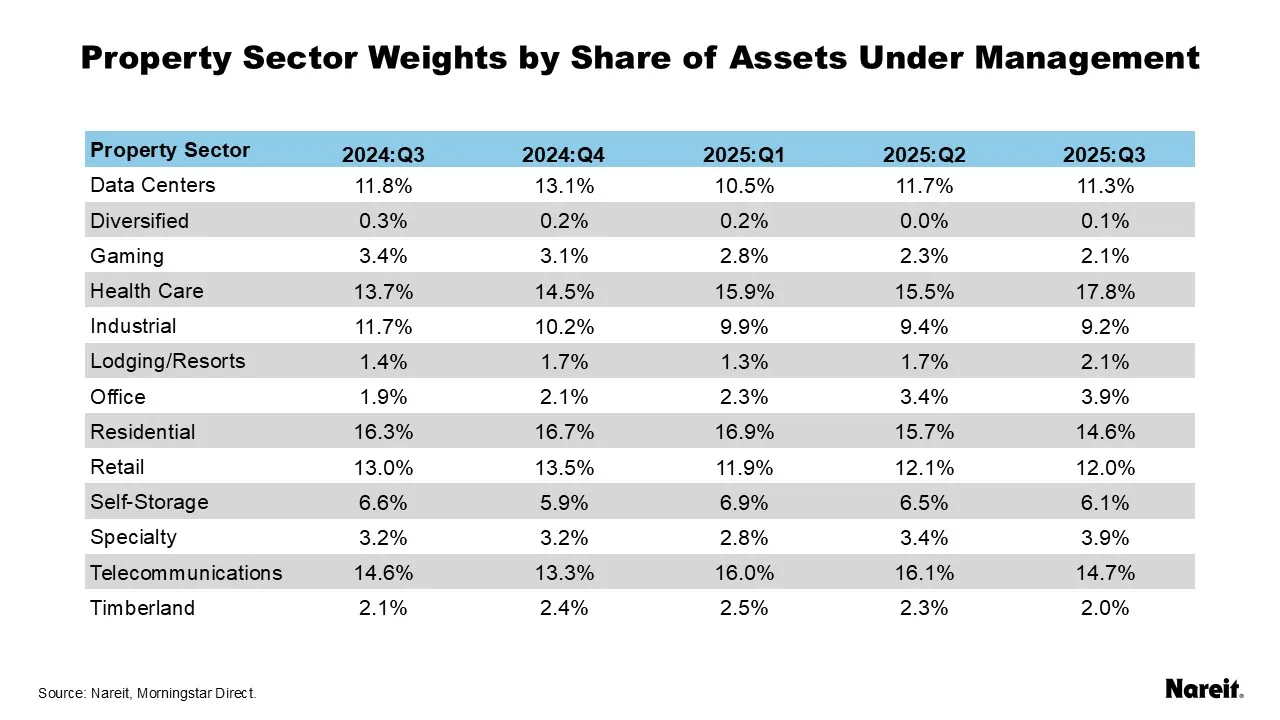

The table above shows the share of each equity REIT property sector by assets under management.

- Health care claimed the top spot for allocations at nearly 18%, surpassing telecommunications at 15%, which briefly ranked first last quarter.

- Residential drops to third largest sector, edged out by telecommunications by less than one percentage point.

- Office has moved from under 2% a year ago to nearly 4% in the third quarter of 2025.

- Lodging/resorts has seen modest growth from under 2% through the year to 2.1% in the third quarter of 2025.

- Diversified remained in last place, with slightly more than a 0.01% share.

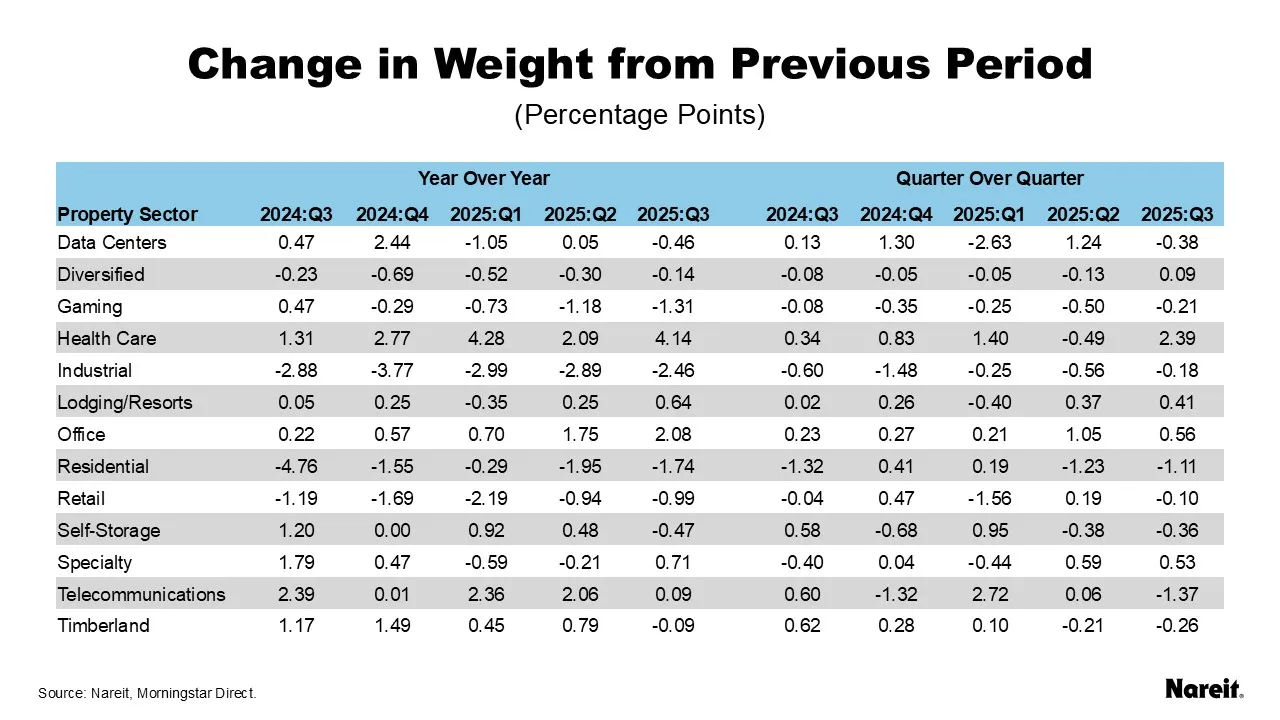

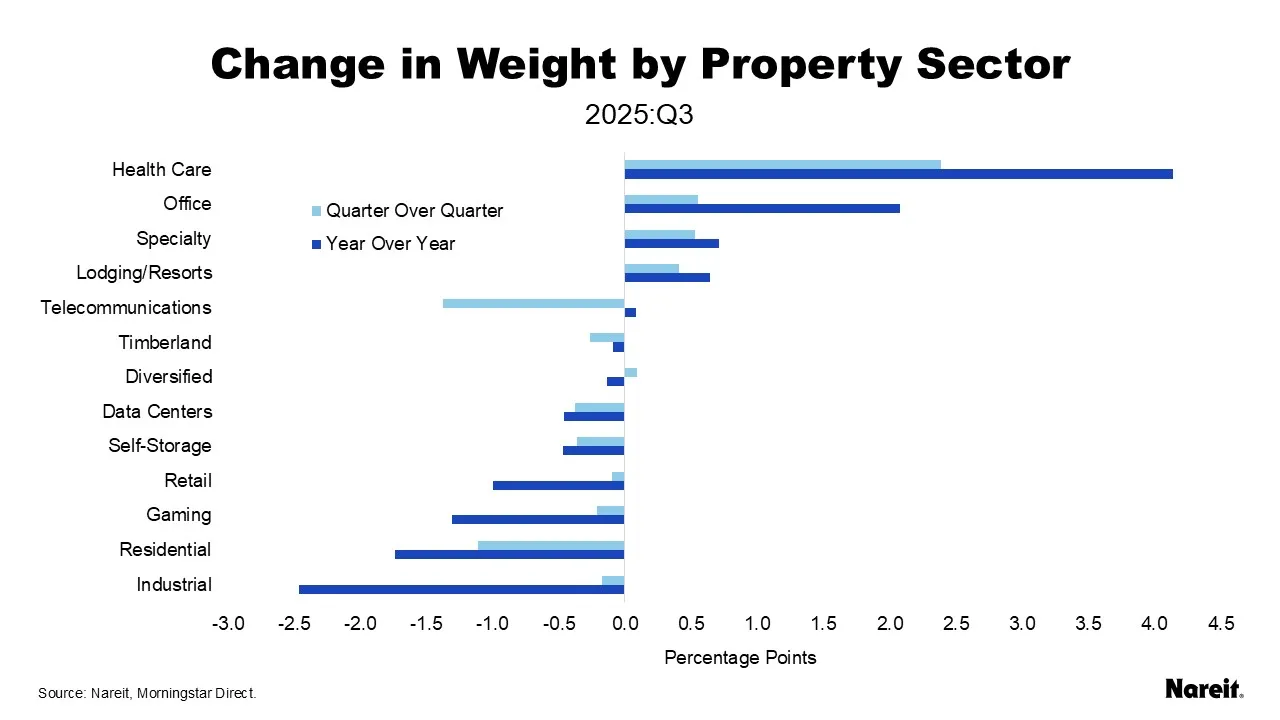

The table and chart above show the change in property sector asset share by quarter and from the previous year.

- Health care had the largest annual and quarterly gain in weight of 4.1 and 2.4 percentage points, respectively.

- Office’s rebound continues with the second largest annual and quarterly gain. Office is up 2.1 percentage points for the year and 0.6 percentage points for the quarter.

- Specialty had the third highest annual increase at 0.7 percentage points after two quarters of annual declines.

- Lodging/resorts has seen small but steady growth over the last year, up less than 0.5 percentage points every quarter, except for the first quarter of 2025. The sector is up 0.6 percentage points, putting its allocation over 2% for the first time since mid-year 2023.

- Industrial had only a slight decline of 0.2 percentage points in the third quarter following more than two years of quarterly declines. Industrial is down 2.5 percentage points annually.

- Telecommunications had the largest quarterly decline at 1.4 percentage points but was flat for the year, up less than 0.1 percentage points.

- Residential had a second consecutive quarter of over a one percentage point decline and is down 1.7 percentage points for the year.

- Several sectors—gaming, retail, self-storage, data centers, and timberlands—were down for both the quarter and the year.

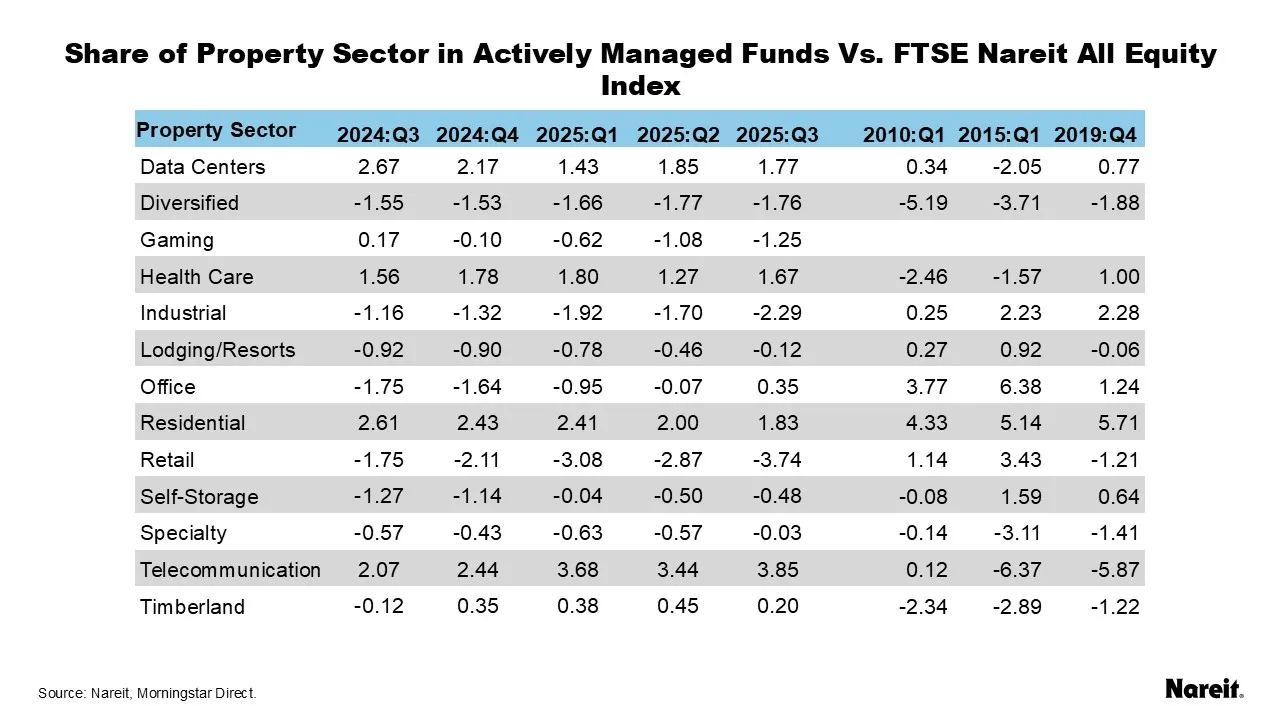

The charts and table above compare the weight of the sectors in actively managed funds to the weight of the sectors in the All Equity index.

- Office moved to overweight for the first time since the beginning of 2020 in the third quarter of 2025. Overweight by 0.4 percentage points, office was at 110% of its index share.

- Despite the quarterly loss, telecommunications remained the property sector with the highest overweight relative to its index share, at 135% in the third quarter of 2025. Telecommunications was also the highest overweight in absolute terms, at 3.9 percentage points overweight its index share.

- Lower exposure to data centers and residential reduced their share overweight this quarter. Data centers was 119% of its index share (1.8 percentage points) and residential was overweight 114% (1.8 percentage points).

- Timberland and health care remained overweight at 111% and 110% of their index weights respectively. Both sectors have been overweight by more than 110% over the past year.

- Increases in lodging/resorts put the sector near parity this quarter after flipping to underweight at the end of 2021. At 99% of its index weight, the sector is now less underweight than self-storage at 93%

- Retail and industrial are both meaningfully underweight. Retail is down to 76% of its index share while industrial is down to 80%.

Note that two of the 23 funds had not reported third quarter data for this analysis.

For more information on the active manager project, see Reading the Real Estate Market: Tracking Active Managers’ Allocations Over Time.