REIT share prices, like the broader stock market, have been sensitive to changes in the outlook for interest rates, including both the short-term rates set by the Federal Reserve and the long-term rates that are governed more by market forces. Rising interest rates have been identified by some analysts as explaining the disappointing REIT stock performance during January and February. In fact, some analyses suggest that negative announcement effects on REITs associated with rising interest rates have become more pronounced since 2013. Recent performance, however, has been in contrast to earlier periods when REIT share prices generally performed quite well during periods of rising interest rates.

The positive association that has historically been observed between periods of rising rates and REIT returns is consistent with an improvement in the underlying fundamentals. Market interest rates typically increase during periods when macroeconomic conditions are strengthening, the same strengthening that often drives positive REIT investment performance. Strengthening macroeconomic conditions typically lead to higher occupancy rates, stronger rent growth, increased funds from operations (FFO) and net operating income (NOI), rising property values and higher dividend payments to investors.

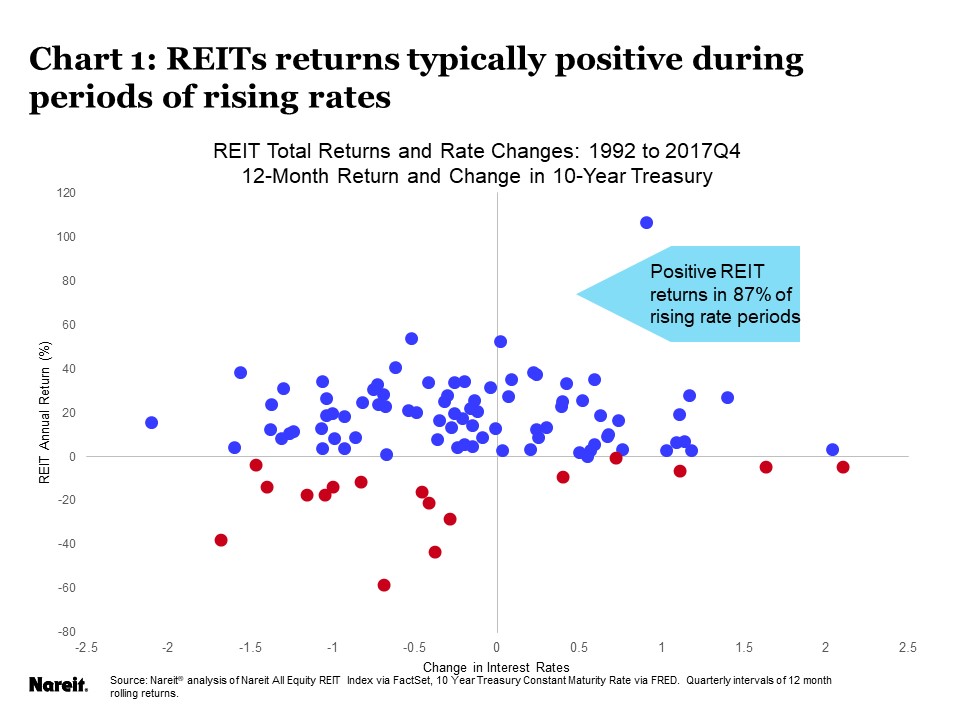

The figure below illustrates the relationship between the four-quarter change in the 10-year Treasury yield and the four-quarter total return on the FTSE Nareit All Equity REIT Index. The illustration reveals that REITs posted positive total returns in 87 percent of episodes of rising Treasury yields over the period 1992Q1 to 2017Q4.

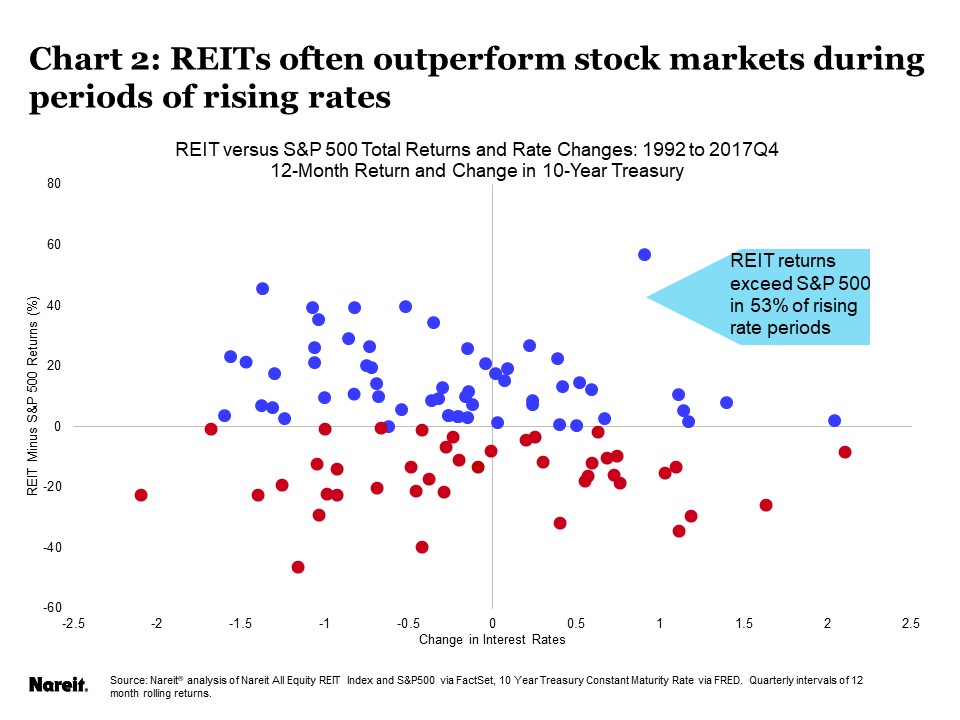

REITs have also outperformed broad equity indexes during many of these periods of rising interest rates. The figure below illustrates the relationship between the four-quarter change in the 10-year Treasury yield and the difference between four-quarter total return on the FTSE Nareit All Equity REIT Index and the S&P 500. This illustration reveals that REITs outperformed the S&P 500 in more than half of the episodes of rising Treasury yields over the period 1992Q1 to 2017Q4.

REITs appear to be well prepared for higher interest rates in the months ahead, according to the Nareit T-Tracker®, a summary of operating performance and financial position of the listed REIT sector. REITs have strengthened their balance sheets and reduced exposures to interest rates. As of 2017:Q4:

- Equity issuance has been strong: REITs have raised significant amounts of equity capital over the past five years, both to strengthen their balance sheets and also to fund the acquisition of new properties.

- Leverage has declined: The debt-to-book assets ratio of REITs has declined to 47.6 percent, down from a pre-crisis peak of 58.3 percent. Book leverage of the REIT industry is at its lowest point since at least 2000, the earliest date in the T-Tracker report.

- Interest expense has declined: Interest expense as a share of net operating income (NOI) is at 22.3 percent, near its record low of 21.7 percent, and a far cry from the 37 percent in 2009.

- Debt maturities have lengthened: REITs have locked in low interest rates for several years into the future. The weighted average maturity of outstanding debt has lengthened to 75 months (more than six years) from 60 months or shorter in 2009.

- Interest coverage ratios are high: Strong earnings growth, low leverage and low interest rates have raised interest coverage ratios to 4.4 times interest charges. Aggregate coverage ratios remain near their highest levels in the past decade and a half.