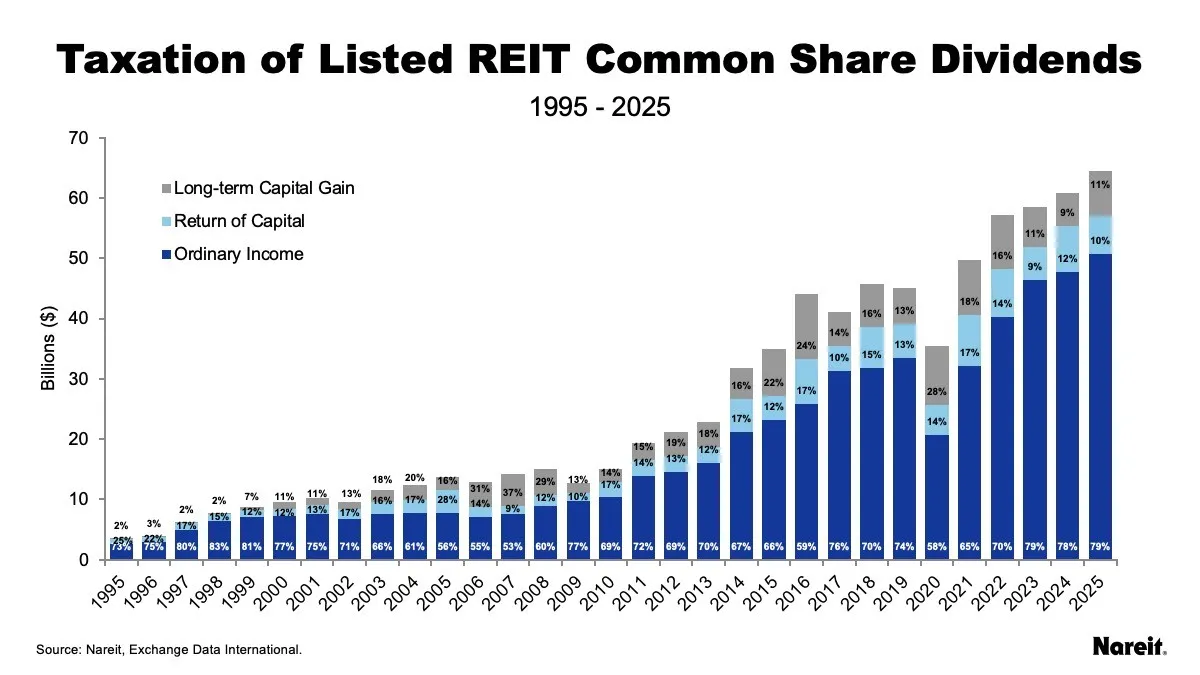

In 2025, U.S. listed REITs distributed approximately $71 billion in dividends, as reflected in Nareit’s REIT Industry Tracker. These distributions are categorized into three primary tax treatments:

- Ordinary Income: For individual and non-corporate shareholders, taxed at the shareholder’s marginal individual income tax rate and generally qualifying for a 20% deduction under Section 199A.

- Capital Gains: For individual and non-corporate shareholders, generally subject to preferential long-term capital gains tax rates.

- Return of Capital (ROC): Not immediately taxable, instead reducing the investor's adjusted cost basis, with amounts exceeding basis generally taxed as capital gains.

Of the dividends recorded by Nareit in our Year-End Dividend Reporting Project, 79% were classified as ordinary dividends, 11% were classified as long-term capital gains, and 10% were classified as return of capital.

The chart above reflects the historical breakdown of REIT dividend taxation. In 2025, approximately 77% qualified as section 199A dividends. Section 199A dividends represent ordinary distributions from REITs that qualify for a 20% qualified business income tax deduction. This tax provision allows eligible noncorporate shareholders to deduct up to 20% of qualifying REIT dividends from their taxable income, effectively lowering the maximum federal tax rate on such distributions from 37% to 29.6%. In 2025 this deduction was permanently codified into the tax code, providing long-term clarity to investors about the taxation of REIT dividends.

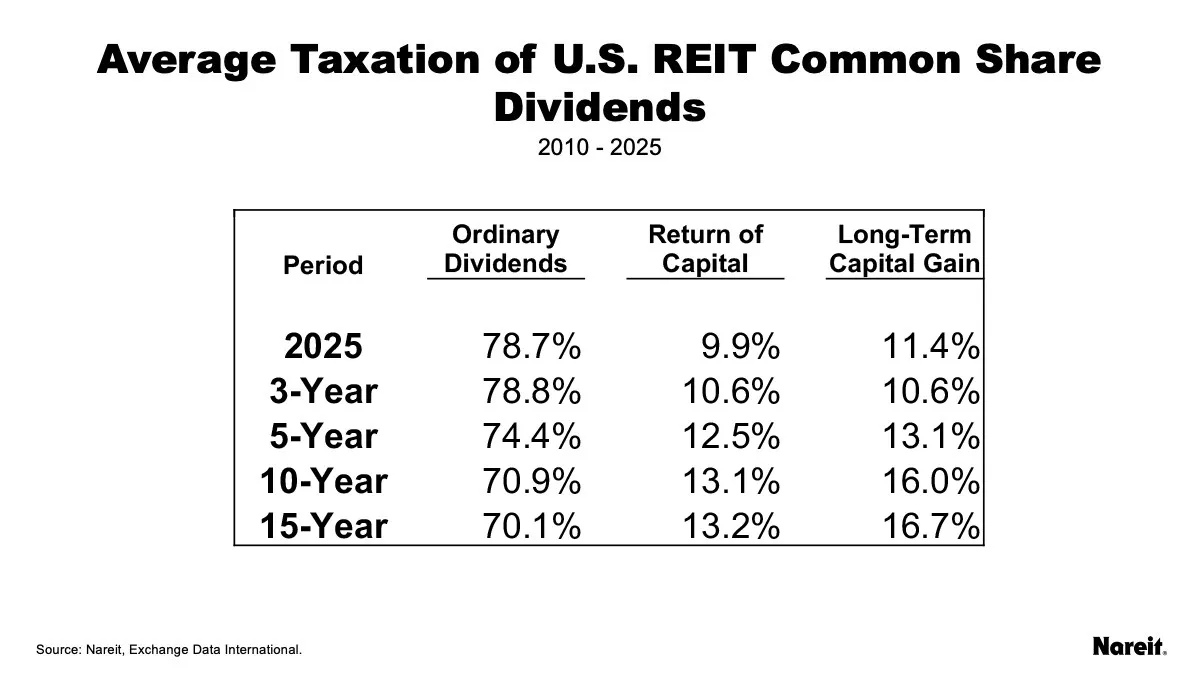

As the table above shows, a significant portion of REIT dividends can qualify as capital gains and as return of capital. Each year, Nareit collects and collates REIT 1099 information in partnership with Exchange Date International. Nareit’s 2025 data can be viewed here.