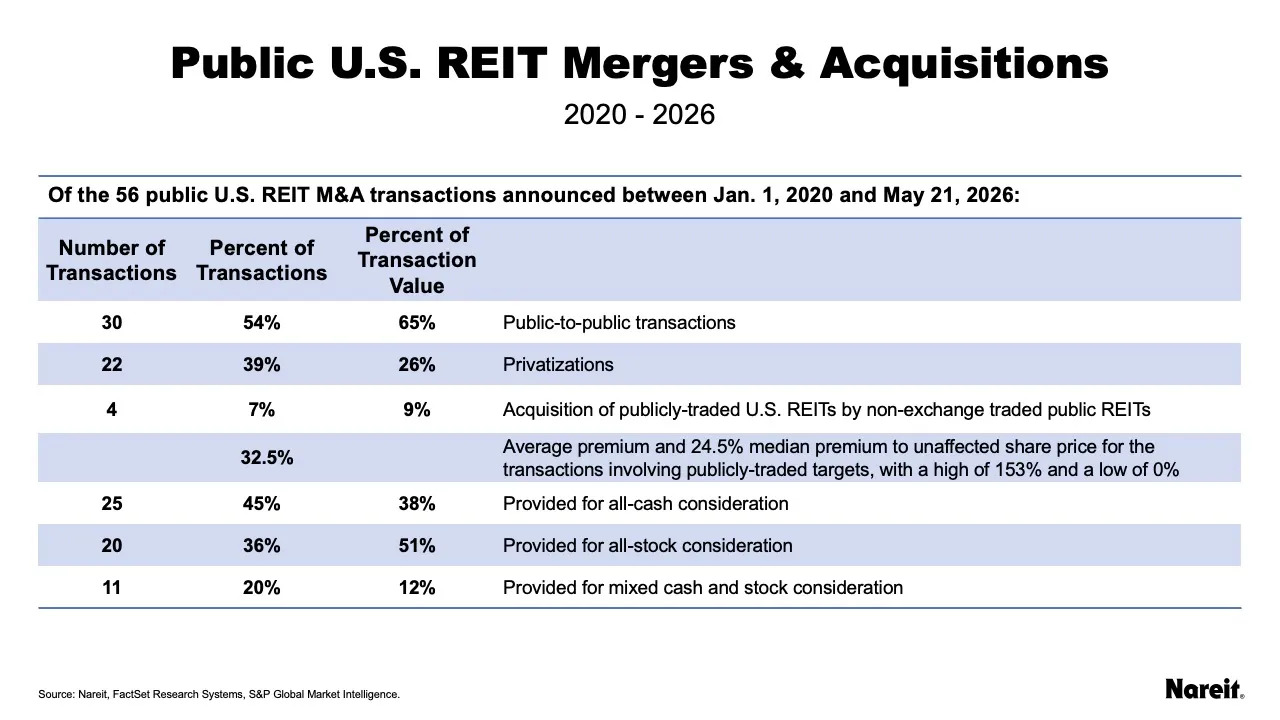

The landscape of U.S. REIT M&A over the last six years has been defined by a significant volume of high-value consolidation. Between early 2020 and mid-May 2026, the listed REIT sector saw 56 total M&A transactions totaling $324 billion. Of these:

- 30 mergers were between listed REITs at a transaction value of $211 billion,

- 22 acquisitions were by private entities at a transaction value of $83 billion, and

- 4 acquisitions were by non-listed REITs at a transaction value of $30 billion.

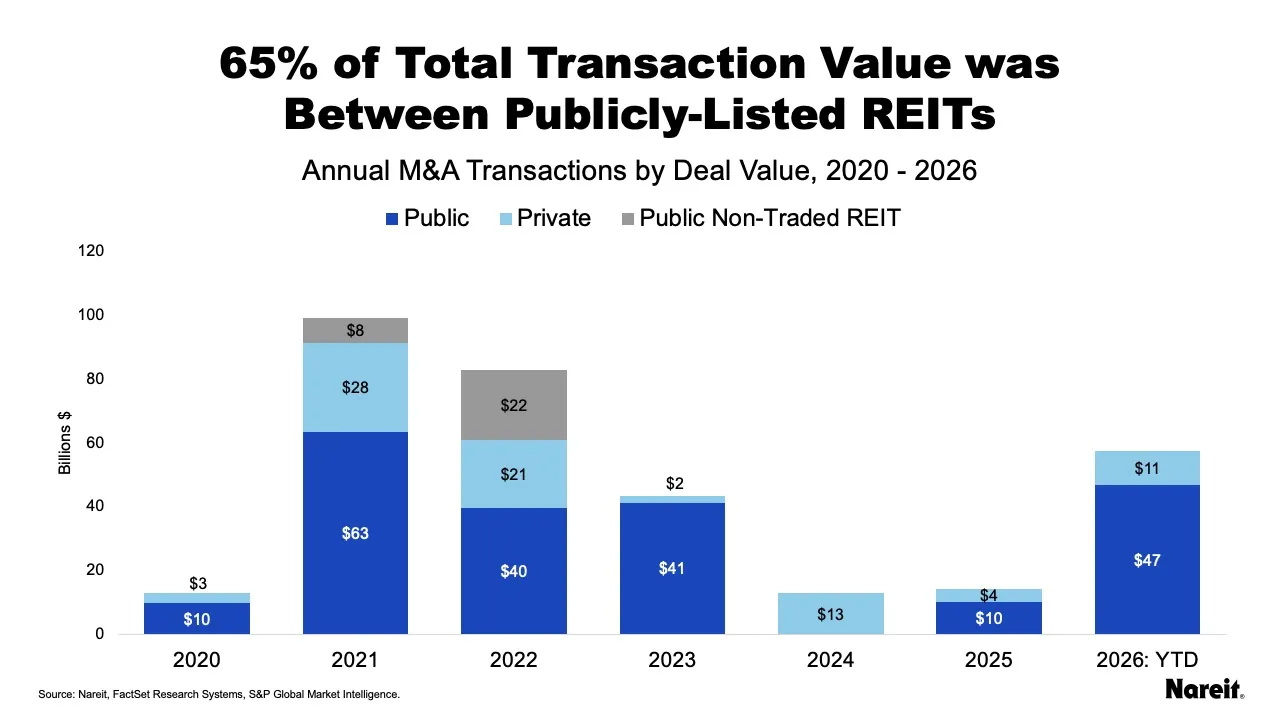

Publicly-listed to publicly-listed transactions were nearly two thirds—or 65%—of total deal value, while private entities accounted for only 25% and public non-listed REITs for 9%.

While privatizations (including non-traded REIT and private entity acquisitions) have accounted for a notable portion of transaction activity since 2020, the listed REIT market has continued to grow. Market capitalization of the REIT industry has grown from $1.2 trillion to $1.6 trillion. This occurred even as the number of listed REITs declined from 223 at the end of 2020 to 189 in 2026.

Taken together, these trends point to a market that is both growing and consolidating, with capital increasingly concentrated in larger listed REITs with the average size of publicly-listed REITs growing from $6.5 billion at the end of 2020 to $8.7 billion in 2026. In addition, over this period, 14 REIT IPOs have raised more than $10 billion.

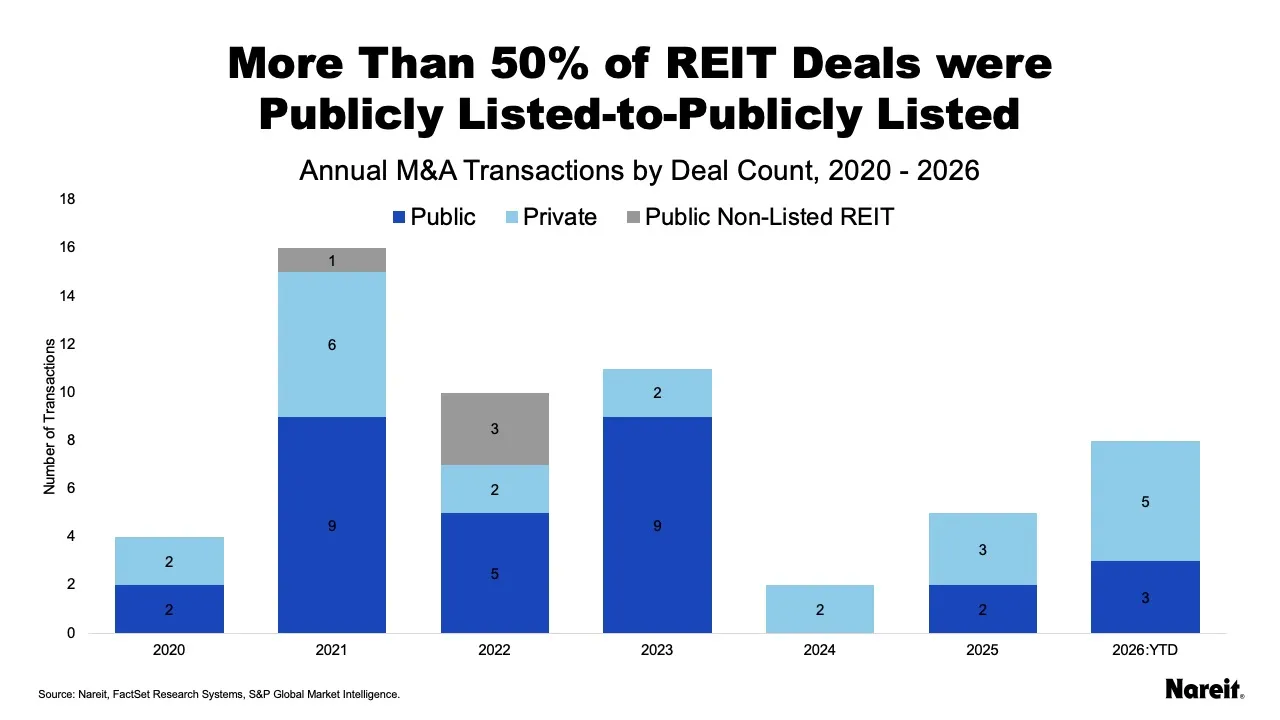

The chart above shows deal count by year over the past six years. Of the 56 deals announced, 30 (54%) were public-listed to public-listed transactions during this period.

The preceding chart reveals a more important narrative, however, as a significant majority of the transaction value has occurred between publicly-listed REITs. Strategic, public-to-public mergers accounted for 65% of the total transaction value between 2020 and 2026. While privatizations often capture headlines, the most significant capital shifts have occurred between listed REIT peers seeking scale, operational efficiencies, and the benefits of combining complimentary portfolios of high-quality properties.

Privatization Trends

Despite the dominance of public REIT mergers, the appetite for privatization is a notable trend. Twenty-two transactions (39%) were privatizations, representing 26% of total deal value.

Deal Structure and Consideration Strategy

The consideration offered in the 56 deals underscores the strategic intent of the buyers and the risk appetite of the sellers.

- All-cash consideration: This was the most popular deal structure, used in 25 transactions (45%) and accounting for 38% of total transaction value.

- All-stock consideration: Preferred by public-to-public consolidators, stock deals represented 20 transactions (36%) and 51% of total transaction value.

- Mixed consideration: Only 11 transactions (20%) used a combination of cash and stock, representing 12% of total transaction value.

The high volume of all-cash deals, particularly in terms of transaction count, aligns with the high volume of privatizations where private equity firms leverage dry powder to exit public shareholders entirely.

In contrast, the fact that stock-only deals represented a higher percentage of value (51%) than count (36%) underscores that the largest mergers in the REIT space are typically public-to-public stock swaps. This allows the combined entity to preserve cash while giving shareholders a stake in the future growth of the expanded company.

The difference in percentage of transaction count (39%) and transaction value (26%) reflects that private buyers often targeted smaller, more specialized REITs as demonstrated in the above table.

Furthermore, a small but notable 7% of transactions (representing 9% of total value) involved the acquisition of publicly traded REITs by non-traded public REITs that have opportunistically targeted high-quality portfolios in core sectors including industrial, residential, retail, as well as modern economic sectors, such as data centers and self-storage.

When combined with traditional privatizations, nearly half of the deal count involved moving assets away from the daily scrutiny of the public exchanges. However, the fact that the majority of total capital stayed within the public ecosystem highlights the enduring efficiency and liquidity that public markets offer to large-scale real estate owners.

Analyzing Transaction Characteristics: Premiums and Valuation

The above charts reveal two dynamics:

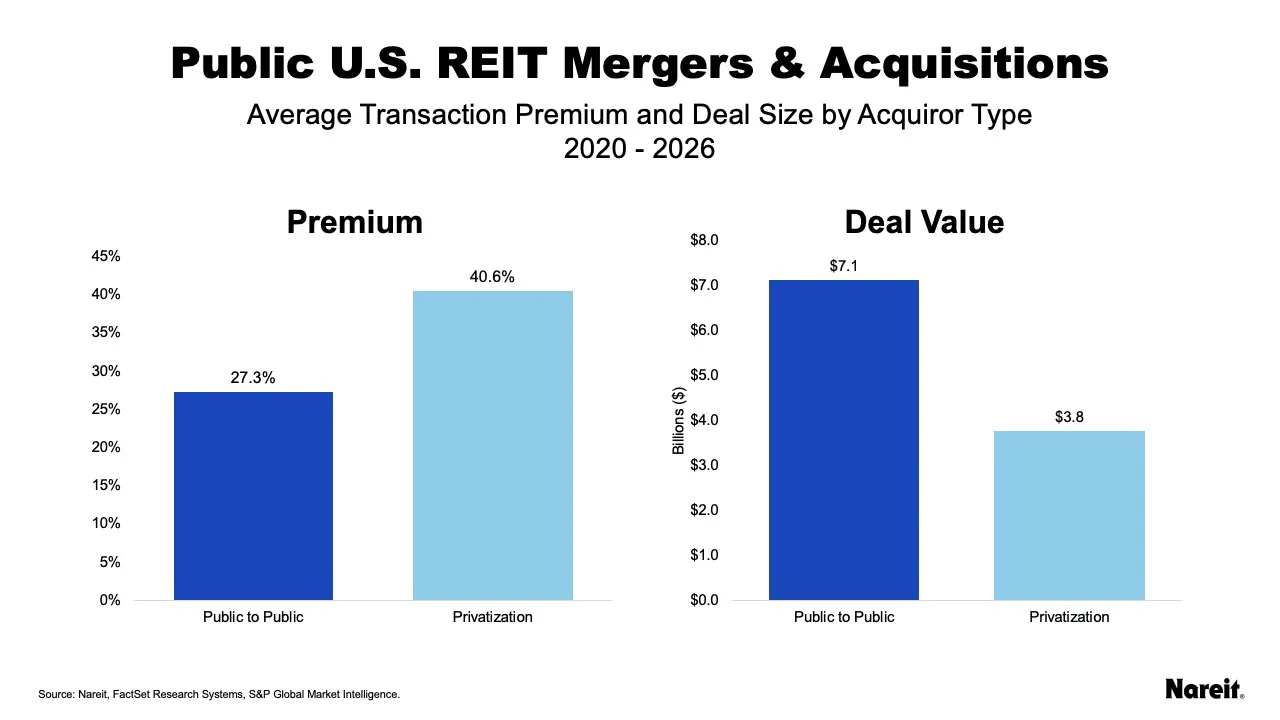

- Privatization deals have typically carried higher premiums than public listed-to public listed transactions—by more than 13 percentage points on average.

- Mergers between publicly-listed REITs have, on average, been nearly twice the size of privatizations.

In short, smaller REITs are being taken private at a premium and capital is tending to stay in the publicly-listed space.

While the rise of privatizations in the REIT landscape has attracted media attention over the past six years, the more important narrative is that M&A activity is largely strategic consolidations between publicly-listed REITs. With the majority of those deals and capital remaining within the public sphere, and premiums averaging more than 30%, current M&A trends reflect a robust mechanism for growth and affirm the high-quality properties owned by publicly-listed REITs.

Visit Nareit’s website for a complete list of listed REIT acquisitions from 2004–2026.