Q4 Data Highlights Strength of REITs’ Operational Performance, Balance Sheets, and Post-Pandemic Recoveries

WASHINGTON, D.C. (March 8, 2023) – REITs’ operations remained solid with year-over-year increases in funds from operations (FFO) and net operating income (NOI), as they continue to navigate rising interest rates and persistently high inflation, according to new fourth quarter 2022 data from the Nareit Total REIT Industry Tracker Series (T-Tracker®) report released today.

“REITs continue to be well prepared to navigate this period of economic uncertainty and higher interest rates,” said Nareit Executive Vice President of Research and Investor Outreach John Worth. “REITs have maintained strong balance sheets, delivered solid operational performance, and notably paid out $61.9 billion in total dividends during 2022—which is a 13.8% increase over 2021,” added Worth.

Year-Over-Year Increases in FFO, NOI Underscore REITs’ Solid Fundamentals

T-Tracker® data for the fourth quarter of 2022 show that despite economic headwinds, equity REITs displayed operational strength. Specifically, the data show that:

- FFO was $18.5 billion—a 10.1% rise from one year ago.

- NOI and SS NOI experienced 6.8% and 6.5% year-over-year gains, respectively, and underscore that REITs are keeping up with inflation.

On a quarterly basis, FFO was down 6.2%, but that decrease was mainly driven by isolated issues related to non-U.S. operations and currency losses. These issues are not reflective of the U.S. real estate market. Excluding the isolated issues, quarterly FFO growth was slightly positive.

T-Tracker® data for the fourth quarter also show that the average occupancy rate stayed steady, increasing slightly to 93.6% from 93.4% in the third quarter.

Historical Analysis of Sector Specific FFO Further Highlights REITs’ Solid Operational Performance, Post-Pandemic Recoveries

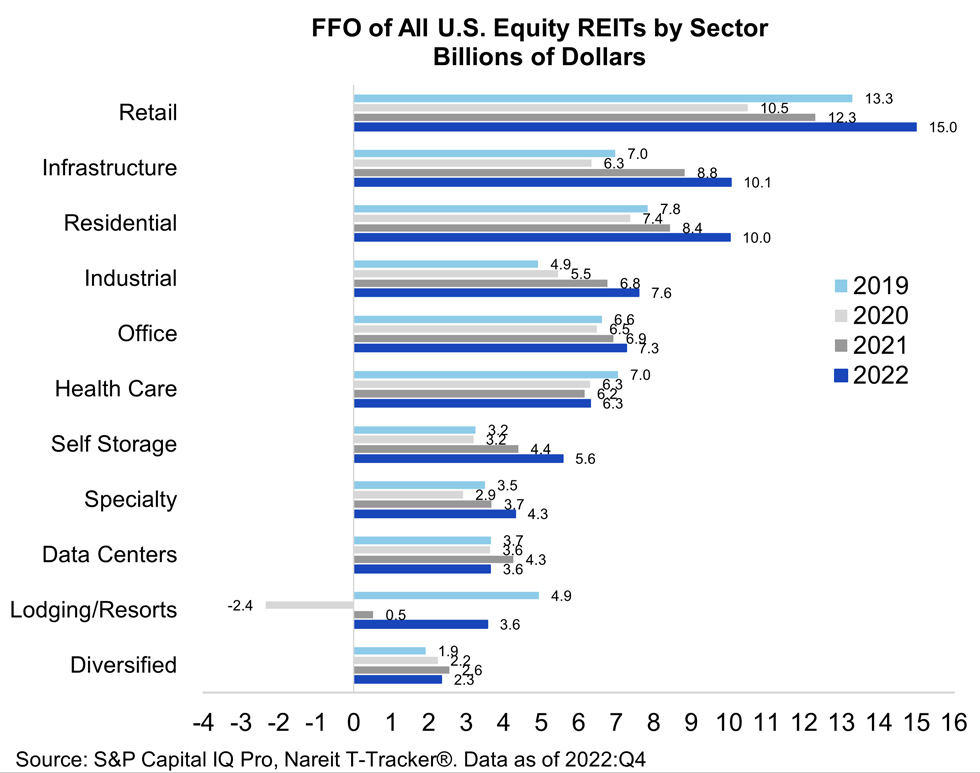

The strength of REITs operational performance is further reflected when FFO is looked at on a sector-by-sector basis over the past four years.

The chart above displays annual FFOs by property sector for all U.S. equity REITs in billions of dollars from 2019 to 2022. The COVID-19 pandemic negatively affected operational performance across all U.S. equity REIT sectors, with the exceptions of two sectors: industrial, which was driven by the rapid growth of e-commerce-based demand, and diversified.

The recoveries from pandemic operational performance levels (2020) are evident across all U.S. equity REIT property sectors as of the fourth quarter of 2022. Furthermore, eight of the 11 property types surpassed their pre-pandemic FFO levels (2019), with health care, data centers, and lodging/resorts lagging. In the current economic climate, these gains are noteworthy because they are a testament to the operational performance strength of U.S. equity REITs.

Public-Private Real Estate Market Divergence Increases REITs’ Attractiveness

Although cap rates do not move in lock step with interest rates, the public real estate market has had a meaningful reaction to the surge in the 10-year Treasury yield; the private market response has been more measured. As of the fourth quarter of 2022, T-Tracker® data show that the REIT implied cap rate was 5.9%, which is 100 basis points higher than the private market cap rate. This valuation divergence creates a potential REIT buying opportunity for investors. A review of historical market dynamics shows that REIT total returns have tended to bounce back—and even surge—after periods of significant REIT relative underperformance.

“The uncoupling of public and private real estate markets—along with REITs’ solid operational performance—has increased the attractiveness of public equity REITs,” said Nareit Senior Vice President of Research Ed Pierzak. “This dislocation is expected to close in the coming year through changes in both REIT and private market valuations. Recent data show that this valuation adjustment process may have already started,” added Pierzak.

REIT Balance Sheets Characterized by Well-Termed, Well-Structured Debt

REITs remain well-prepared for continued higher interest rates by maintaining long-term, well-structured debt along with low levels of leverage. For example, T-Tracker® data show that:

- Leverage ratios remained near historical lows with debt-to-market assets at 33.7%.

- Fixed rate debt accounted for 86.3% of total debt.

- Weighted average term to maturity of REIT debt was nearly 7 years—or 82.4 months.

- Weighted average interest rate on total debt was 3.7%

- Interest coverage was 4.5 times.

For more data, please read the complete Q4 2022 Nareit T-Tracker® report.