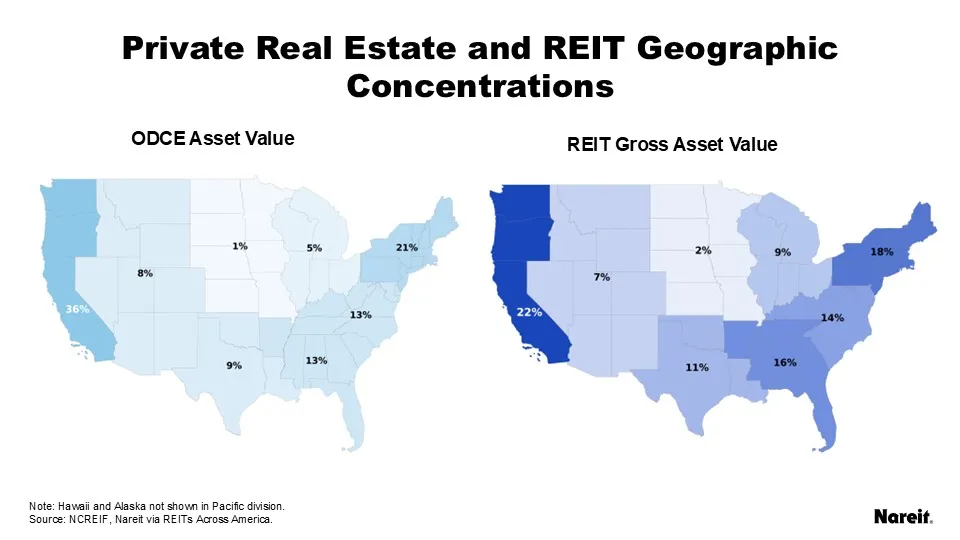

The NCREIF Open End Diversified Core Equity index (ODCE) is a commonly used benchmark for investors in private real estate. Alternatively, the FTSE Nareit All Equity REITs Index is a popular benchmark for listed real estate. Previous Nareit research has explored the differences in the two benchmarks in terms of performance and diversification. This analysis shows the geographic differences between the property holdings of the two benchmarks.

Comparing REITs and ODCE asset values geographically, REITs are more evenly distributed across eight divisions in the United States and have a greater share across the southern-most states, known as the Sunbelt region, than private real estate. ODCE asset value is predominantly in industrial and residential, while REITs are more diversified across property types. Most property type asset value is in the Northeast and Pacific regions for ODCE with the exception of residential which has a significant presence in all the divisions. For REITs, retail, self-storage, and other are the most evenly distributed property types across the U.S.

The ODCE Performance Attribution Report uses property level data to calculate the end of month value of properties in eight U.S. divisions: Northeast (which includes the mid-Atlantic states), Mideast, Southeast, East North Central, West North Central, Southwest, Mountain, and Pacific. The share of total value of the funds at year-end 2024 is shown in the light blue map on the left. Nareit publishes the geographic distribution of properties and gross asset value along with other key metrics for all public REITs on the REITs Across America website for year-end 2024. The dark blue map on the right uses this data restricted to just the REITs in the All Equity index.

Both REITs and ODCE have the highest share of value in the Northeast and Pacific divisions. Both divisions contain states with generally higher value real estate than other parts of the country. REIT property value is more evenly distributed than ODCE value. For REITs, 40% of value is in its two largest regions: 22% in the Pacific and 18% in the Northeast. For ODCE, 57% of its value is in its two largest regions: 36% in the Pacific and 21% in the Northeast. REITs also tend to favor the Sunbelt more than ODCE, with a larger share of value in the Southeast and Southwest, totaling 27%, versus 22% for ODCE. The three central divisions have very small allocations, under 10% in each for both ODCE and REITs.

As core real estate focused funds, ODCE is primarily invested in retail, office, residential, and industrial, compared to the All Equity index which is more diversified. These four property sectors are 88% of ODCE across all regions, while only 45% for REITs. For ODCE, nearly two-thirds of value is in industrial and residential, while the two property types are less than one-third of REIT value. REITs also have less value in the office sector, at only 5% compared to ODCE’s 14%.

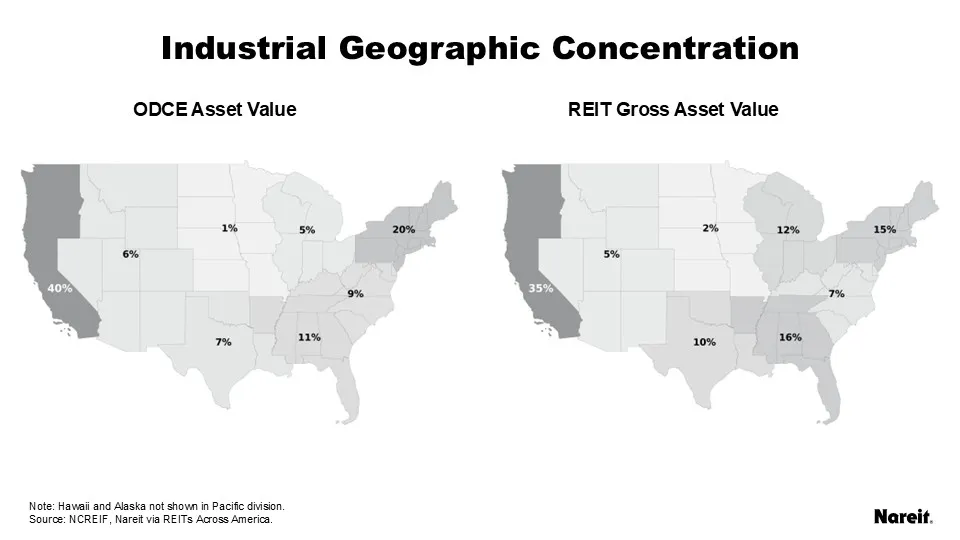

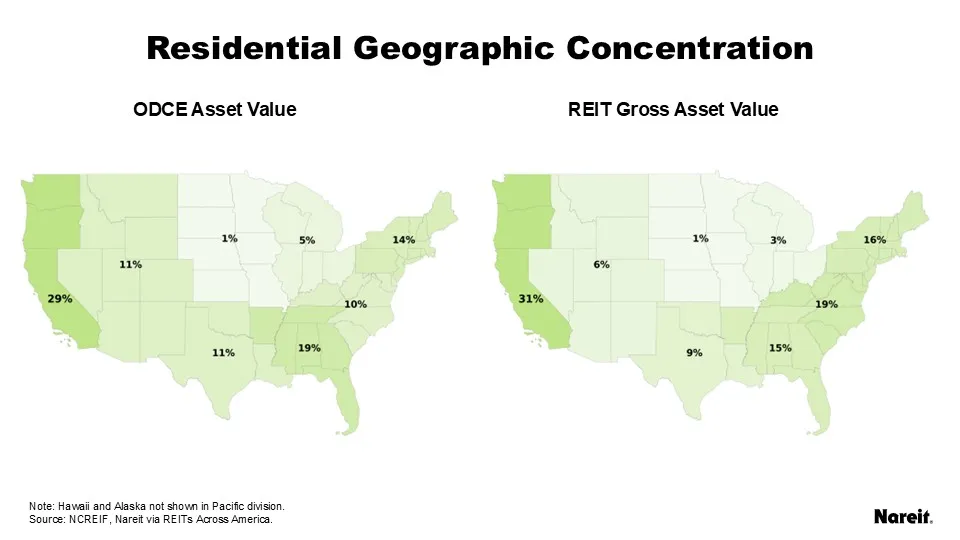

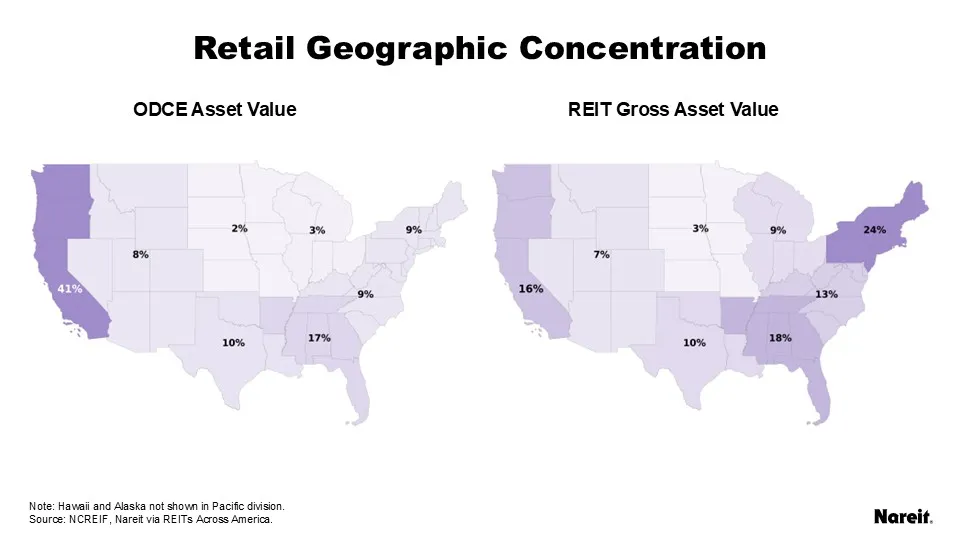

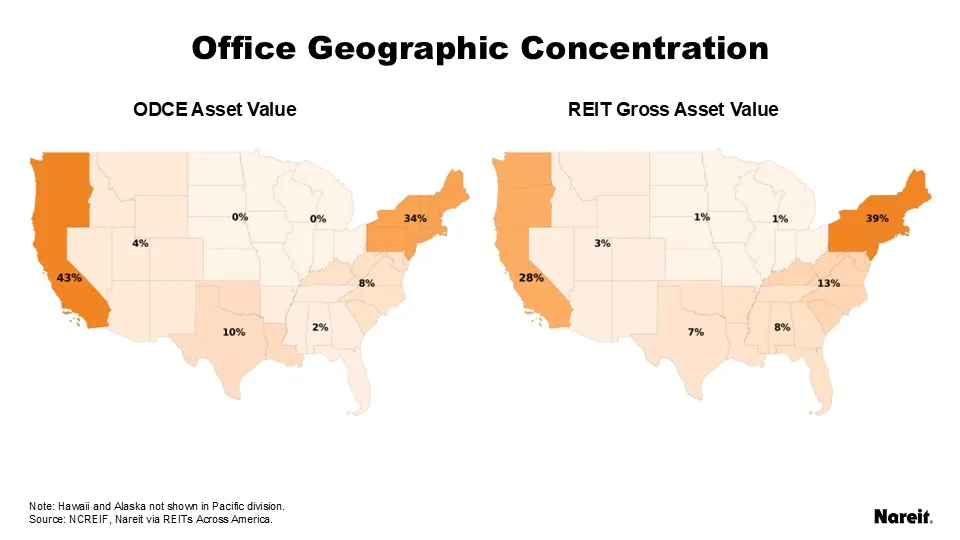

The maps above show each property type’s geographic distribution of value for ODCE and REITs.

- Industrial value for both ODCE and REITs is highest in the Pacific division, at 40% and 35% respectively. However, industrial REIT value is more evenly distributed along the coastal areas, with significantly higher allocations in the Mideast division (12% vs 5%) and in the southern divisions (26% vs 18%).

- Residential is the only property type more evenly distributed across divisions for ODCE than REITs. While REITs have 50% of value on the East Coast and more value in the Pacific than ODCE, ODCE has higher values across the middle of the country.

- Retail for ODCE is very concentrated in the Pacific, with 41% of value in the division compared to only 16% for REITs. Other than the Pacific, the Southeast division has a strong concentration, with 17% of ODCE retail value. Conversely, REIT retail has the smallest allocation to the Pacific of any property type. Instead, the majority of retail value is in the Northeast at 24% followed by the Southeast at 18%.

- Office is the most concentrated of the four property types for both ODCE and REITs. ODCE has 77% of value in the Pacific and Northeast divisions and REITs have 67%. REITs have significant asset value along the rest of the East Coast and the Southwest, but ODCE has very little in the Southeast.

ODCE’s core real estate mandate makes it less diversified in the types of property included in its funds compared to publicly listed REITs. The funds are also less diversified geographically, tending to overweight the Northeast and the Pacific compared to REITs, which are more evenly distributed and have greater property value in the Southeast and Southwest.